Exposure to Race Issues: Firm Responses and Market Reactions After George Floyd’s Murder

Reputation is paramount for a consumer-facing business, and since a firm’s reputation relies on its alignment with the public, corporations are sensitive to shifts in social values. Even when popular will does not lead to new policy, people vote with their pocketbooks, and firms that remain out of touch could end up suffering irreparable harm to their brands and bottom lines. Societal shocks can rapidly transform commonly shared beliefs, and what had been accepted practice becomes unacceptable, providing a powerful lesson to companies – or any entities – unable to incorporate and embody contemporary principles and ethical standards.

On May 25, 2020, the murder of George Floyd produced a spark that ignited international outrage, widespread protest and a collective awakening to racial injustices. The heightened awareness of race-related issues persists today, yet the shifting zeitgeist has not produced the results that many activists have called for – Black Americans are killed by police in even greater numbers now than they were in 2020, according to the nonprofit Mapping Police Violence, and they are nearly three times as likely to be killed by police than are white Americans – in an effort to eradicate racial injustice in America. Yet as the upheaval precipitated by George Floyd’s murder reverberated through every corner of society, some things did change, particularly in the corporate world.

In this insight we will discuss “Racial Diversity Exposure and Firm Responses Following the Murder of George Floyd,” a recent study by Daniela De la Parra, UNC Kenan-Flagler Business School assistant professor, and colleagues Karthik Balakrishnan and K. Ramesh of Rice University and Rafael Copat of the University of Texas at Dallas examining firm-level exposure to issues of racial diversity and corporate responses to the social demands of the moment after George Floyd’s murder.

Corporate Exposure to Issues of Racial Diversity Affects Market Valuation

To create a measure of corporate exposure to racially sensitive issues, the study’s authors analyzed transcripts from more than 180,000 conference calls held by more than 10,000 firms between 2005 and 2022. Using this text-based method, the researchers found and tabulated instances of discussion of race-related issues in corporate communications with investors, analysts and other market participants. The authors posit that the greater the incidence of race-related topics, the more important these issues are for the firm in question, and the greater that company’s exposure to matters of racial diversity.

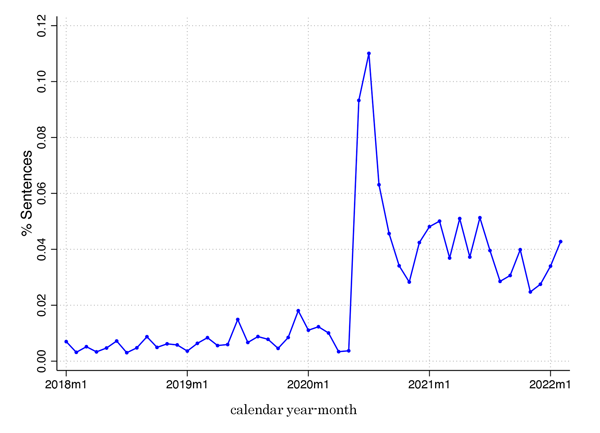

The researchers find that corporate discussion of diversity-related issues spiked in the aftermath of George Floyd’s murder (see Figure 1), with about one-quarter of the sampled firms publicly discussing diversity for the first time after the murder. In expressing concerns about racial diversity and injustice, company leaders were revealing their company’s exposure to these issues, and the market took notice. Using a subsample of conference calls held from May 26, 2020, the day after George Floyd’s murder, through the end of 2021, the authors examined market returns, finding that when company leaders discussed diversity-related topics, the market penalized the firm with 0.7% lower return, on average, in three-day windows around the communiques. Amid the national unrest spurred by George Floyd’s murder, market stakeholders were rationally troubled that a firm’s failure to address issues of diversity, equity and inclusion could impact the company’s credit risk while making it the target of customer boycotts, social activism, regulatory pressure, political backlash and employee antipathy.

Figure 1: Average Percentage of Diversity Sentences in Conference Calls

Market reactions to firm discussions of racial issues were not uniform, however, and the study’s authors repeated their analysis to uncover nuances in how shareholders responded to the ways that companies talked about and acted on issues of racial equity in the 18 months following George Floyd’s murder. Analyzing the same subset of conference calls and market data, the researchers used machine learning to identify discussions associated with action-oriented initiatives versus those considered to be passive language, finding that market reactions diverged along this active-passive dissection. Shareholders rewarded the firms that discussed their race-related risk with regards to the actions they would take with increased valuation. Meanwhile, when company heads used passive language while discussing race-related issues, markets reacted negatively, docking these firms’ value by 2.1%, triple the severity of the average penalty.

Corporate Actions Speak Louder Than Words

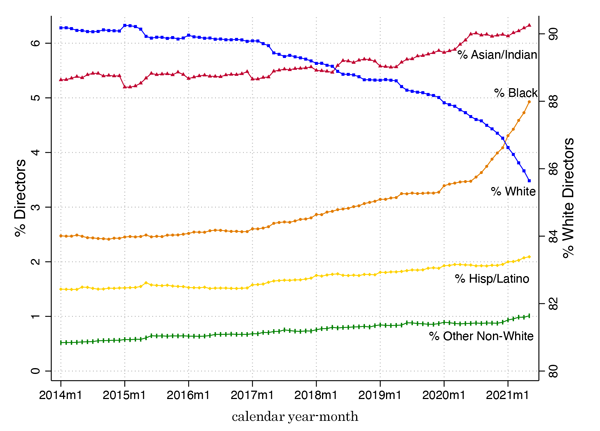

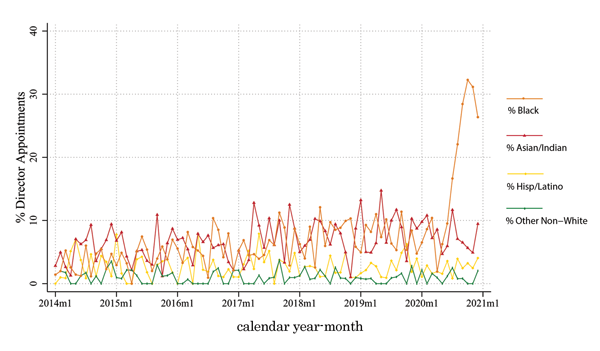

In words and in actions, corporations responded to the racial reckoning triggered by the murder of George Floyd. For companies seeking to improve internal DEI in a publicly visible way, increasing the racial diversity of corporate boards is a main avenue of change. Looking at the ethnicity of board directors of about 6,000 U.S. firms since 2013, the researchers find that companies without Black board members were many times more likely to hire at least one in 2020 or 2021 than in previous years. Meanwhile, firms that had included Black representation in their boardrooms prior to 2020 were more likely to retain them in the years following the death of George Floyd. Among the study’s most revealing findings, the authors determine that while Black members represent less than 5% of corporate boards, they account for between 20% and 30% of all new board appointments made soon after George Floyd’s murder (see Figures 2 and 3).

Figure 2: Diversity in Board Composition

Figure 3: Percentage of New Director Appointments by Ethnicity

Racial diversity of corporate boards is only one area that needs addressing, and firms acted in many other domains to mitigate their exposure to race-related issues. To study these other paths, the researchers used a novel database from As You Sow, a nonprofit shareholder advocacy group that tracks companies’ race-related actions quarterly as part of its Racial Justice Initiative. Merging this dataset with their conference call transcript database and other data sources, the authors were able to observe the discussions and actions of about 1,000 firms for a full year, from the third quarter of 2021 through the second quarter of 2022. Their analysis determines that if companies discussed race-related issues in their calls in this period, it was more likely that they would go on to act on racial diversity in a number of ways, including establishing a DEI department and appointing a DEI leader; clearly defining a diversity goal and detailing a plan to enhance diversity in their supply chain; and engaging more with their community and donating to racial justice causes.

Taking Meaningful Action Reduces Exposure and Boosts Market Value

Companies that took meaningful actions to mitigate their exposure to race-related issues following George Floyd’s murder did in fact see results. Combining As You Sow data describing corporate actions with conference call data proxying firm exposure, the researchers show that firms that made real efforts to improve racial equity reduced their exposure to race-related issues over time. The market, meanwhile, rewarded companies that appointed Black board members with valuation boosts, yet only in cases where the appointments did not enlarge the board size. The authors posit that these efforts to “overboard” – to expand board sizes by adding Black members – were viewed as symbolic rather than substantive acts, and that companies that made these token gestures did not experience the same boost in market value as the firms that meaningfully diversified their board room.

The study’s authors test the robustness of their analysis at every step, mitigating endogeneity wherever possible, and their results prove statistically significant. In many respects, their conclusions could be expected: Corporate leaders are concerned about their exposure to race-related issues, and taking concrete actions to improve diversity reduces this exposure. Yet the analysis’s most stunning findings are just how swiftly a societal shock – in this case, the murder of George Floyd – can shift social values and how clearly these values translate to market demands.

This article is part of our Grand Challenge series on business resilience.