By Courtney Edwards, Associate Director of the UNC Tax Center, and Clinical Associate Professor of Accounting at UNC Kenan-Flagler Business School

According to a recent POLITICO poll, only half of voters want Congress to force President Trump to disclose his tax returns. I’m willing to bet even fewer are interested in seeing mine. Nonetheless, in honor of tax season, I wanted to spend a few minutes sharing with you how the 2017 tax reform law affected my personal tax liability, as an example of some of the ways in which reform may have altered your returns as well.

First, you need to know a few things about me. Here are the basics: I’m unmarried and have one 16-year-old dependent son. I’m a professor at the University of North Carolina. I earn a salary, receive some dividends and interest and have a few gains and losses from selling investment securities. I pay state income and property taxes, make a few charitable contributions and pay interest on my home mortgage. In other words, a fairly common tax scenario. So how did tax reform affect me in 2018, the first year most of its provisions took effect? Are my taxes lower than they would have been without tax reform?

I’m somewhat ashamed to admit that before deciding to share this with you today, I didn’t know the answer to these questions. I understood how the law had changed. I had even completed my 2018 tax return. But I still didn’t specifically know whether I was better or worse off thanks to tax reform.

Before I get into the details, one big caveat: The answer depends on many factors, and results can and will vary depending on where you live, how much you earn, what forms of income you have, how big your mortgage is, your marital status and how many children you have, to name just a few. The answer is not one-size-fits-all. Still, because my specifics are fairly common, I think understanding how and why reform affected my tax situation could be interesting to others.

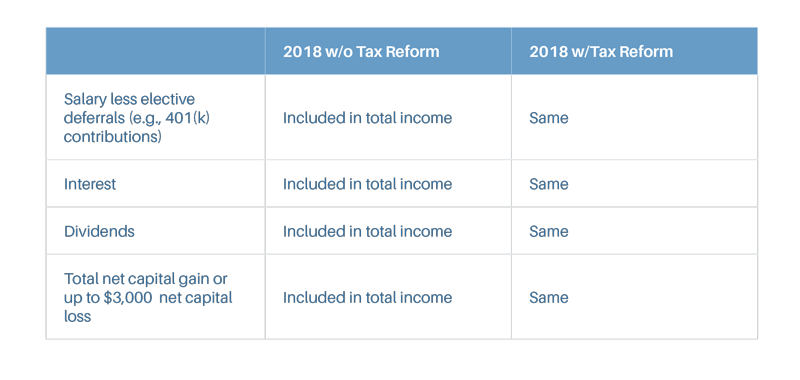

Here’s a brief summary of what the income portion of my 2018 tax return would have looked like with and without tax reform:

Bottom line: tax reform did not change the total income I reported on my 2018 tax return. This is not the case for deductions and other reductions in taxable income.

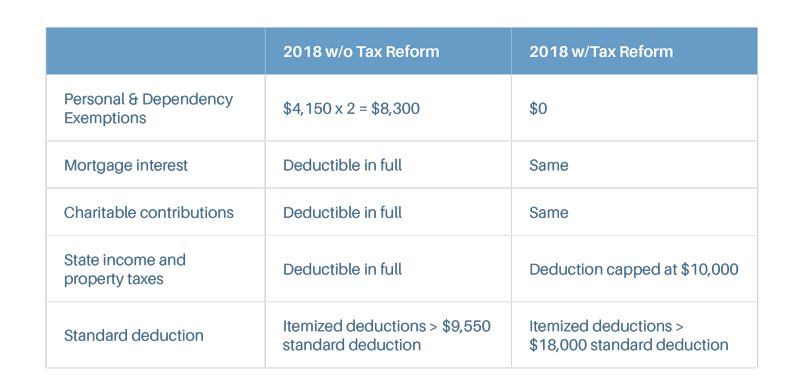

Here is a brief summary of what that portion of my 2018 tax return would have looked like with and without reform:

As you can see, my taxable income in 2018 was higher than it would have been without reform, thanks to the repeal of the personal and dependency exemptions and a cap on the amount of state and local taxes allowed as an itemized deduction.

But taxable income is not tax liability. Tax reform did more than just change the calculation of the tax base. It also changed the calculation of tax by changing the regular tax rate structure, as well as the Alternative Minimum Tax (AMT) calculation. Specifically, the regular tax brackets were broadened and the rates lowered somewhat (e.g., the maximum individual tax rate is 37% versus 39.6% prior to reform). While this lowered the tax I otherwise would have owed, the change in the AMT had the more significant effect on my tax liability.

As the name implies, AMT is an alternative tax computation that uses a broader tax base and a lower tax rate structure. Taxpayers calculate their tax liability under both the regular and this alternative tax system and pay whichever is higher. In years prior to tax reform, I consistently paid the AMT. Thanks to tax reform, however, I did not owe AMT in 2018.

To calculate AMT, taxpayers reduce their AMT base by an AMT exemption amount. This exemption is subject to phase-out once income exceeds a threshold amount.

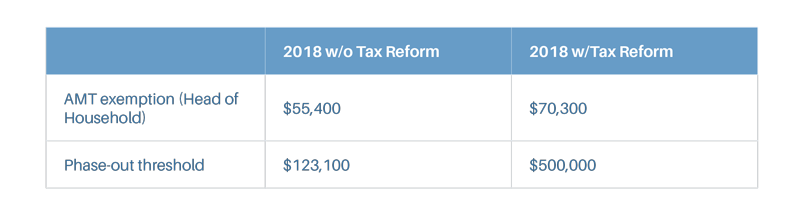

The table below summarizes the 2018 AMT exemption and phase-out threshold for my filing status with and without tax reform:

Tax reform not only increased the AMT exemption amount, but it also significantly increased the phase-out threshold. As a result, I did not owe AMT in 2018, although I would have without tax reform.

Taking all of these changes into account, my overall tax liability was actually about 10 percent lower in 2018 than it would have been without tax reform. A Tax Foundation analysis concluded that taxes would be lower for 80% of all individual filers. Despite this, many individuals are finding that the tax refunds they’re receiving from their 2018 filings are lower than they were in 2017. I, in fact, owed tax with my 2018 return, and this amount is higher than what I owed in 2017.

This outcome is creating a lot of confusion for many. If tax reform should be decreasing taxes for most taxpayers, why are tax refunds lower (or, as in my case, taxes owed higher)? It’s important to remember that tax liability is not the same as the taxes owed or tax refund due amount that appears on the bottom line of your tax return each year. Taxes owed or refund due represents the difference between your tax liability for the year and the amount that you’ve paid in during the year through withholding and/or estimated tax payments. In early 2018, the withholding tables employers use to calculate withholding amounts were changed to reflect the lower expected tax liabilities associated with reform. So individuals should have enjoyed somewhat higher paychecks throughout the year. In theory, that’s a good thing. After all, why wait until April 2019 to feel the effects of tax reform? But many taxpayers are disappointed, perhaps because they’re used to getting a bigger check at tax return time. Despite their dissatisfaction, however, it’s a fact that for most individuals, myself included, tax reform has actually lowered the total federal taxes they paid for 2018.