Q&A with Kala Gibson: Banking on Impact

Fifth Third Bank executive Kala Gibson says his organization believes it has an obligation to use its capital in ways that expand access and remove long-standing barriers to opportunity.

Fifth Third Bank executive Kala Gibson says his organization believes it has an obligation to use its capital in ways that expand access and remove long-standing barriers to opportunity.

UNC Kenan-Flagler's Camelia Kuhnen discusses the possibilities of open banking with Duke Fuqua's Manju Puri.

During the institute's monthly press briefing Feb. 2, Senior Faculty Fellow Christian Lundblad discussed a "Wow!" employment report for January in which job growth beat all expectations.

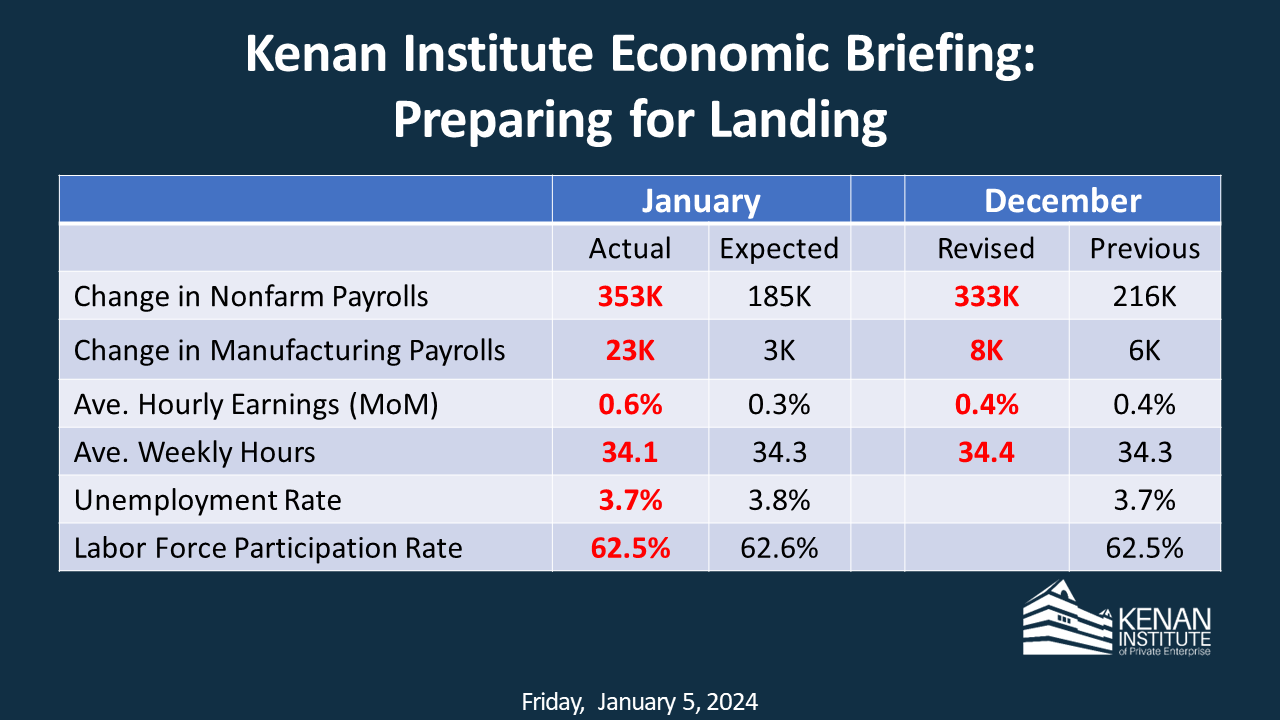

During the institute's monthly press briefing Jan. 5, institute Chief Economist Gerald Cohen analyzed another healthy job growth number and discussed his five economic trends to watch for this year.

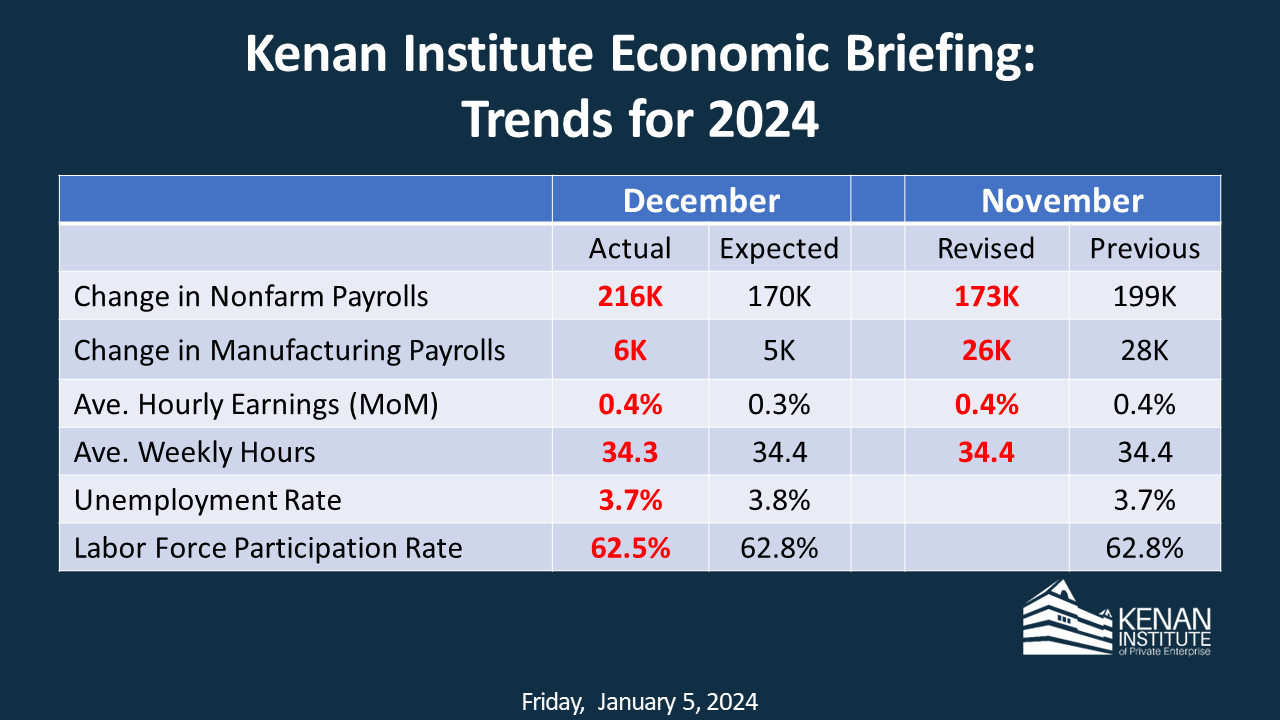

During the institute's monthly press briefing Dec. 8, former institute Executive Director Greg Brown analyzed the “slower slowing” in employment growth and signs that the Federal Reserve should keep its guard up against inflation.

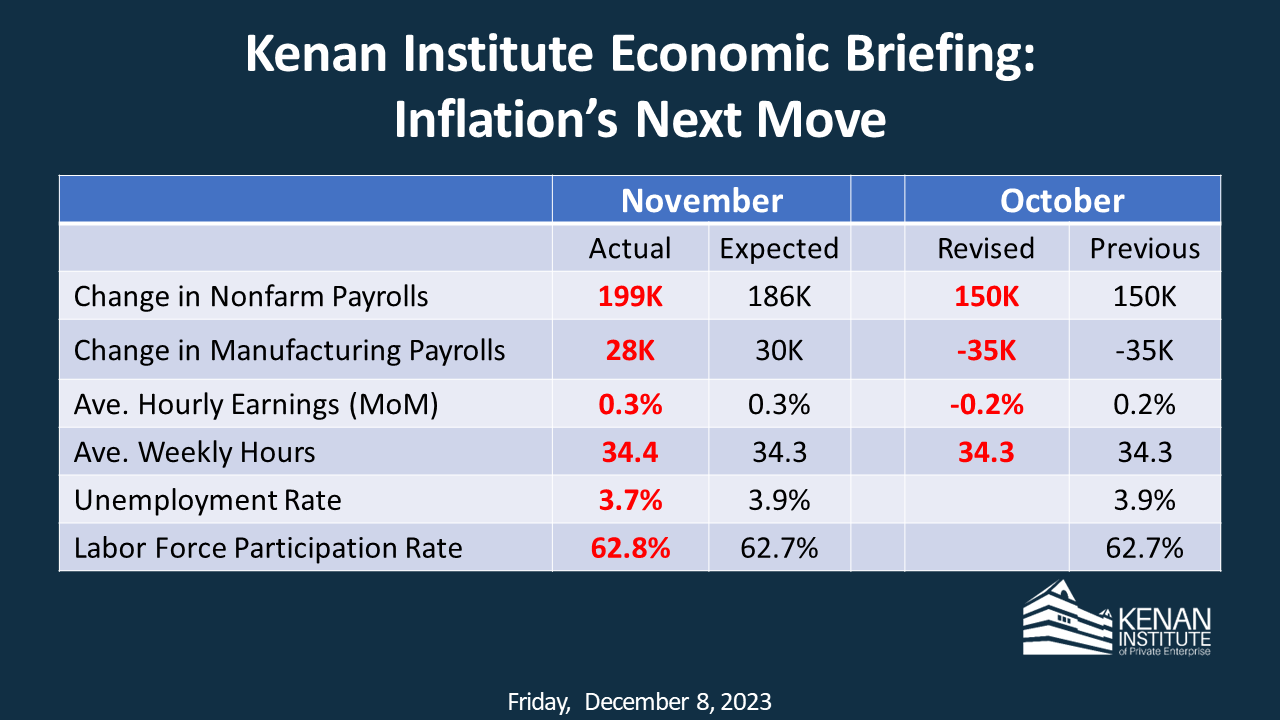

During the institute’s monthly press briefing Nov. 3, Research Director Camelia Kuhnen analyzed the subdued job growth in October’s employment report and why economic growth isn't being distributed evenly among all households.

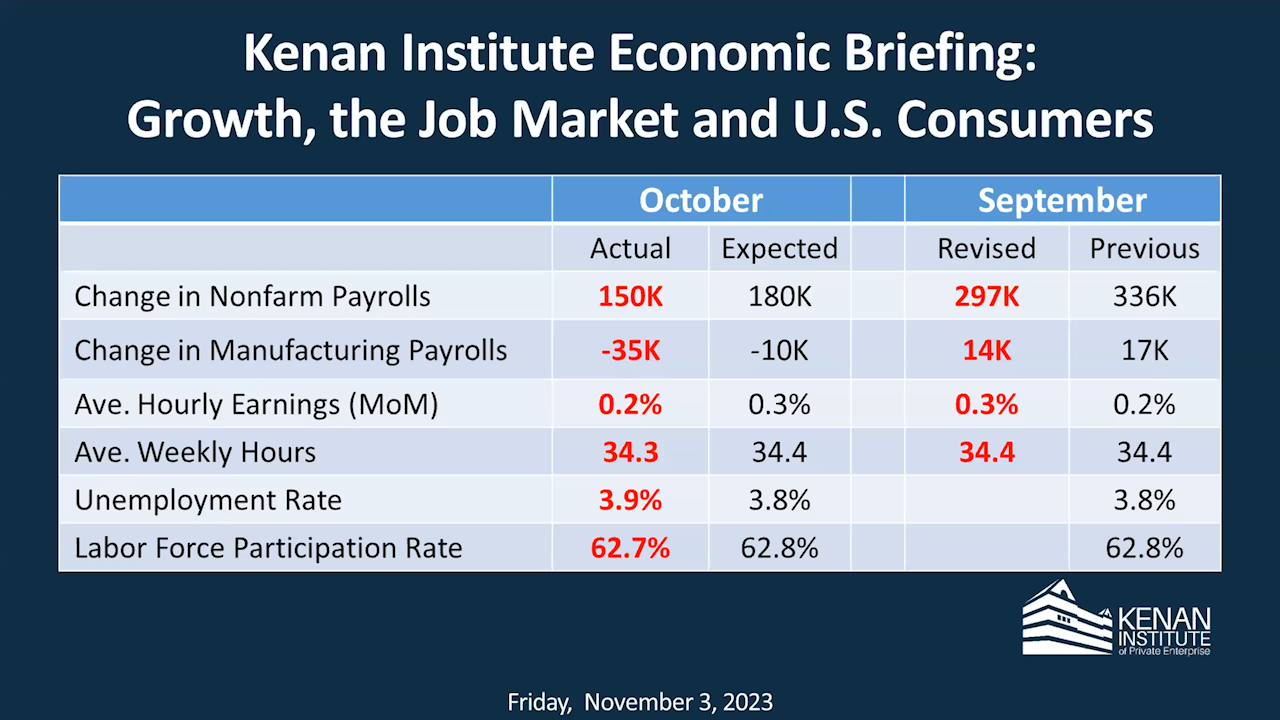

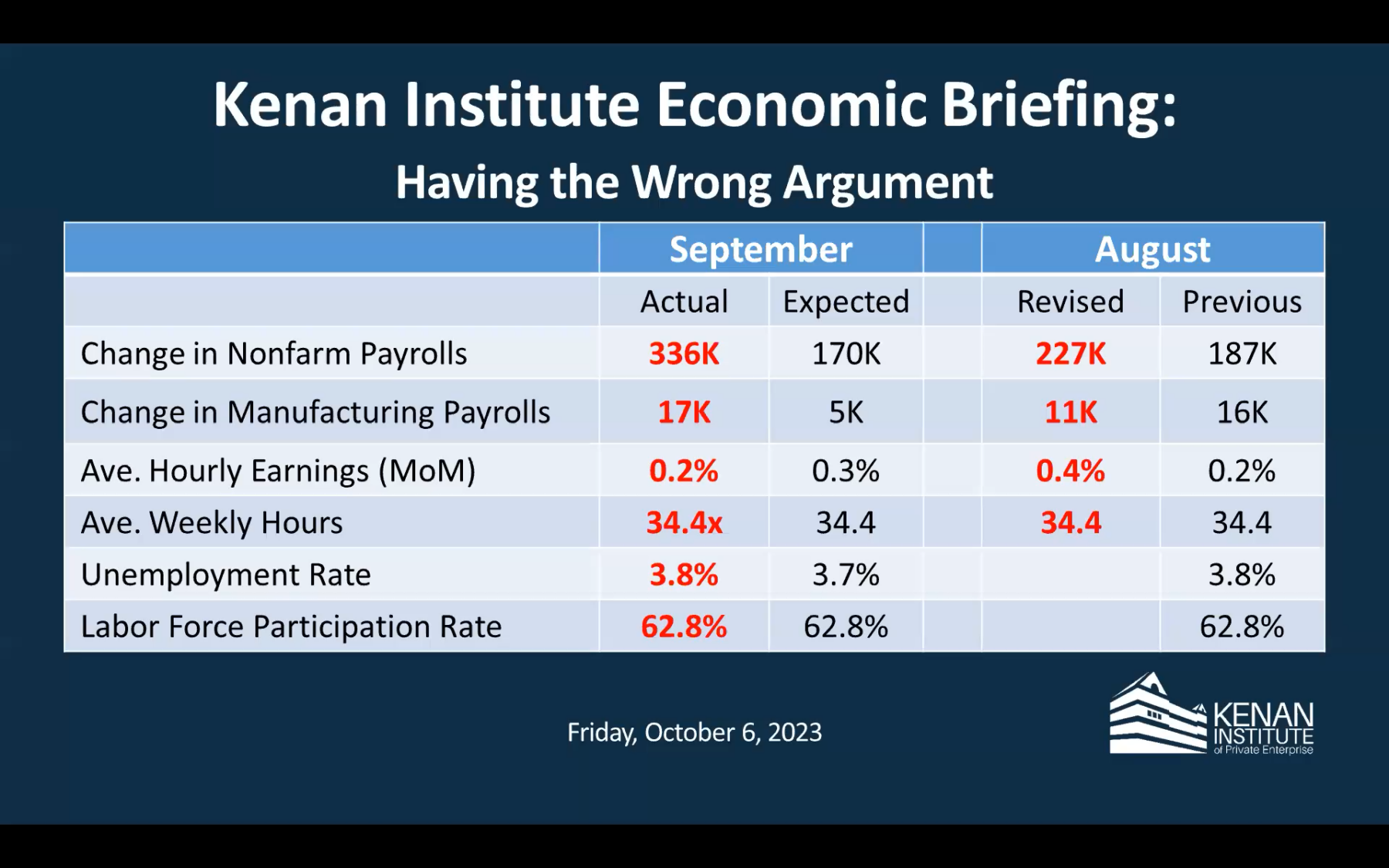

Chief Economist Gerald Cohen analyzed the strong job growth in September’s employment report during the institute’s monthly economic briefing Oct. 6 and looked at why Congress should focus on mandatory spending and tax revenue, not discretionary spending.

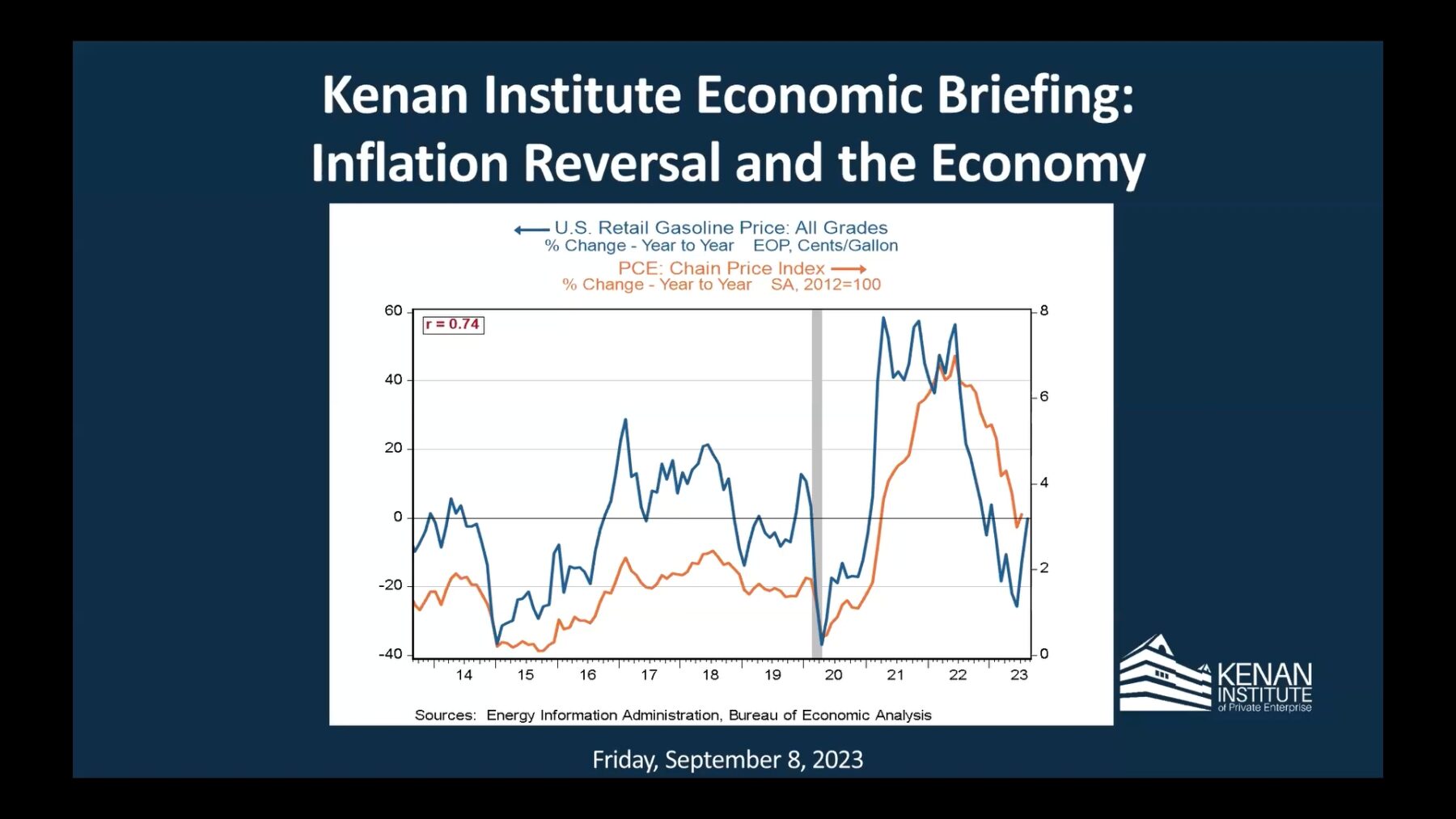

Institute Chief Economist Gerald Cohen examined the effect of rising gasoline prices on overall inflation figures and the Federal Reserve’s probable response during the institute’s monthly economic briefing Sept. 8.

UNC Tax Center Research Director Jeff Hoopes discusses how the tax system figures into the debt ceiling standoff and why we probably won’t see any dramatic increases in taxes anytime soon.

Chief Economist Gerald Cohen discusses why the uncertainty caused by the debt ceiling crisis is bad for the economy - regardless of how the situation ends.

Recent bank failures have revived the old debate "Are banks too big to fail?" Chief Economist Gerald Cohen spoke with "Marketplace" to discuss comparisons to the 2008 bank crisis and whether we should be worried about what comes next.

Kenan Institute Research Director Christian Lundblad navigated the cognitive dissonance provided by another strong jobs report when considered alongside more negative indicators during the institute’s latest economic briefing July 8. The virtual event took place at 9 a.m. after the release of the latest monthly employment numbers. Lundblad also answered questions from the audience, including limitations on the Federal Reserve in addressing core consumer price issues, the differences among regional labor markets, and the probability of an actual recession vs. a technical recession occurring this year.

Join us to hear from Seth Lloyd, Professor of Mechanical Engineering and Physics at MIT, as he shares his findings on quantum algorithms for analyzing financial data and predicting time series

Participants include Jim Goldman, Assistant Professor of Financial Economics, University of Toronto; Eva Steiner, Associate Professor of Real Estate, Penn State University; Jay R. Ritter, Joseph B. Cordell Eminent Scholar, Warrington College of Business, University of Florida; Allyson Tucker, Chief Investment Officer, Washington State Investment Board; Michael Elio, Partner, StepStone; Christian Lundblad, Richard Levin Distinguished Professor of Finance, Director of Research, Kenan Institute of Private Enterprise; Matt Harvey, Managing Director, Head of Direct Lending, PGIM Private Capital; and David Sambur, Apollo Global Management, Inc.