- Both academics and practitioners are hampered by the measurement problem in social entrepreneurship. Without a consistent aggregated measure, academics are unable to measure how efficiently social entrepreneurship can create impact or assess risk-return relationships. Practitioners are limited in evaluating how well their portfolios are creating impact without this measure. The industry risks inefficient allocation of capital, potentially overinvesting in segments that are most easily interpretable in the present framework and underinvesting in high-impact segments.

- Challenges to scaling social entrepreneurship also include expanding access to capital. This challenge is tied to one of the mechanisms for investors to create impact through their investments, i.e., targeting companies that are constrained by external financing conditions is one of the ways in which providing a lower cost of capital can be an effective means to create impact. Tackling this issue will involve not just creating entrepreneurial networks, but also breaking down existing structural patterns of discrimination in investment.

- Finally, the data on this sector is slim. Impact investors and academics need to collaborate in order to effectively measure the frontier between financial return and impact, and appropriately measure risk in both dimensions. Academics can also be helpful in ensuring that the burgeoning industry is not replicating entrenched patterns of investment through careful cross-sectional analysis.

Major strides have been taken in recent years to push toward more sustainable investing practices, including a corporate call to develop a core set of universal environmental, social and governance (ESG) disclosures. Yet it remains to be seen if these initiatives will bear fruit, especially for those most in need. In the United Nation’s 2030 Agenda for Sustainable Development, Secretary-General António Guterres cited a funding gap of $2.5-3 trillion per year to support its 17 goals, suggesting that not all sustainable investments are necessarily producing substantial impact.

Researchers have described three mechanisms by which investors can achieve impact: shareholder engagement, capital allocation to companies constrained by external financing conditions and indirect impact via stigmatization, endorsement and benchmarking. During the 2020 Kenan Institute Frontiers of Entrepreneurship conference, UNC Kenan-Flagler Business School Professor Olga Hawn provided context for these mechanisms. She explained that the most effective way for investors to achieve impact is by growing businesses that provide solutions to the world’s problems. Promoting best practices via engagement or screening is a second-best mechanism, and there is little evidence that indirect mechanisms such as signaling (in which investors influence public discourse by targeting beneficial sectors and excluding harmful ones, e.g. fossil fuels) can achieve measurable impact. Unfortunately, most sustainable capital is invested in signaling, while the smallest amount is invested in growing new businesses.

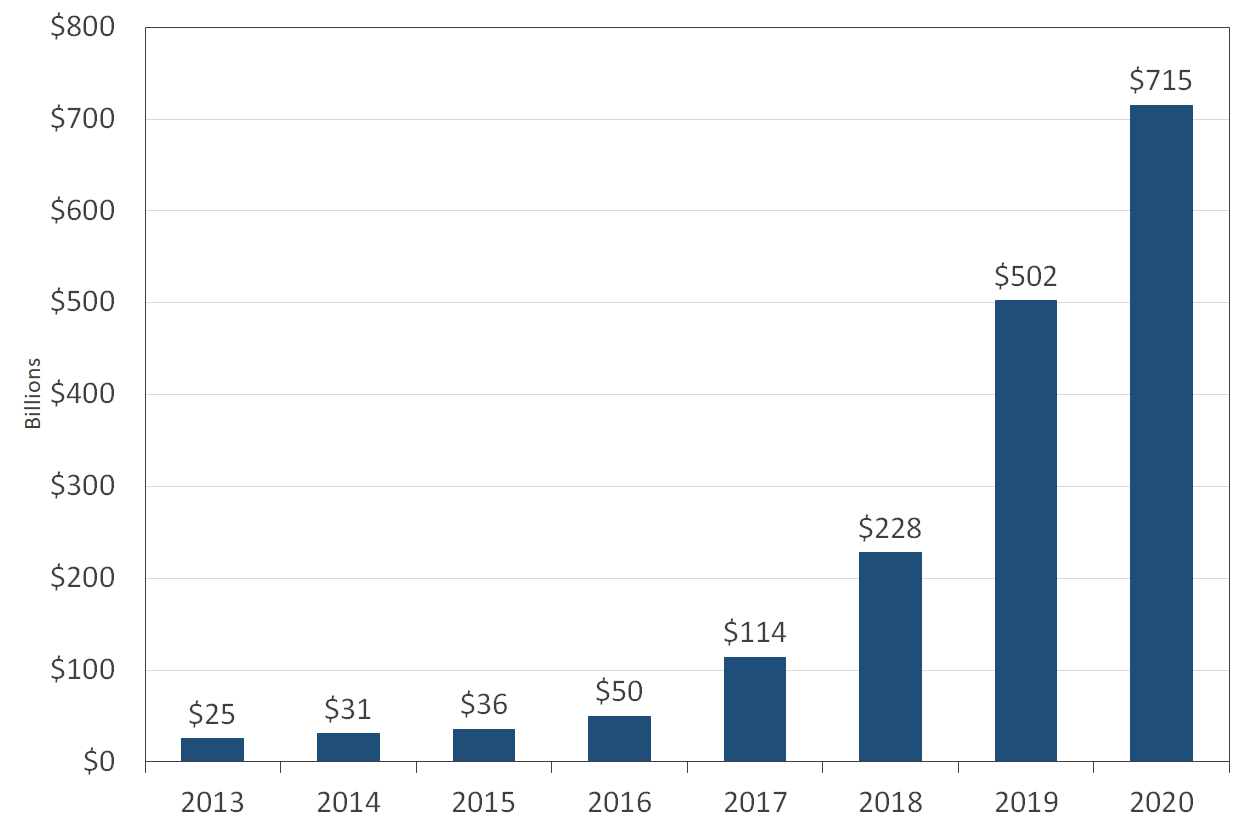

This suggests a rising role for impact investing and social entrepreneurship. These investors use the modalities of business in order to target an increase in social benefits and financial returns. According to the Global Impact Investing Network, the total impact investing market is about $715 billion in 2020. Advocates in this space argue that investors can deliver social and environmental impact in a cost-effective way, redeploy capital that would be lost in a grant-making philanthropic context and prevent negative externalities that may occur by conducting business using only a profit-seeking strategy.

Source: GIIN, Annual Impact Investor Survey

Concessionary Capital and the Risk-Return Trade-off

A purely return-seeking fund has the benefit of a single investment goal for a disparate group of investors; this is not the case for impact investing. More work outlining the risk-return trade-off is a necessary step in order to determine modal impact goals and provide more investment options for a variety of investors. Cleanly articulating the relationship between risk and return within and across impact and financial dimensions is thus a foundational requirement for developing the industry.

The impact investing finance literature has started to address this task by asking whether investors sacrifice financial returns in order to create impact through their investments. The extant literature on impact investing has not reached a clear conclusion on this question. Barber et al. (2019) found that after benchmarking to similar venture capital (VC) funds, impact funds earn 4.7% lower internal rates of return (IRRs). Kovner and Lerner (2015) analyzed the performance of community development VC funds and found that these funds’ investments are less likely to succeed than investments by traditional VC funds. However, the Wharton Social Impact Initiative found evidence that market-rate-seeking impact investing funds are competitive with the market on a gross basis.

Panelists at the Frontiers of Entrepreneurship conference said they believe this trade-off is less stark in practice. Elizabeth Chou, an investor at Leeds Equity Partners, emphasized that targeting impact is a profitable strategy. Investing in a great service in a sector where consumers are demanding more efficacious products will inevitably lead to a company’s financial success.

An obvious issue with this literature is that it assumes that investors create impact and analyze variation in financial returns across funds. This obscures the true relationship between the amount of generated impact and financial returns. Without consistent industry-wide metrics for measuring impact, assessing this trade-off between financial return and impact has not yet been undertaken in a robust way in academic circles.

Can Social Entrepreneurship Scale?

Even without a clear risk-return relationship, investor demand for socially responsible investment products has been increasing over time. Hartzmark and Sussman (2019) found causal evidence that mutual fund investors value sustainability. Conference presenter Mike Elio, a partner at StepStone Group, described the process of generational change that leads to shifts in limited partner (LP) demands and tastes in the private markets, which tend to lag developments in other markets. Responsible investing has become the norm as more responsibility-focused investors and millennials with large amounts of capital enter the space. Elio emphasized that once LP support shifts, then general partner (GP) practices will change.

There are still challenges to scaling. Consistent measurement of impact has important ramifications for productive deployment of capital, in addition to effectively communicating risk-return trade-offs. Berg et al. (2019) analyze ESG ratings across six rating agencies and find considerable disagreement. This disagreement primarily originates from differences in measurement practices and categories used for assessment. Hawn argued that ESG ratings should be geared toward promoting investments that have the most effective mechanisms for generating impact. Chou also discussed this difficulty from the practitioner perspective. As metrics are rolled up across different companies that target different goals, it is difficult to accurately summarize impact without losing the true depth of outcomes. This also complicates assessment of whether funds and companies are practicing what they preach about ESG, according to Elio.

Overcoming Barriers to Access

The matching of capital with social entrepreneurs is still a hurdle to generating impact, according to conference presenter Philip Gaskin, vice president of entrepreneurship for the Kauffman Foundation. Without a connected entrepreneurial community, the same capital gaps that exist in the rest of the VC space may be embedded in the impact space. Furthermore, Kölbel et al. (2019) found that only when socially responsible capital targets companies constrained by external financing conditions can capital allocation be an effective mechanism for delivering impact. The Kauffman Foundation has responded to this problem by testing the use of alternative funding structures to reach underrepresented communities. Fortunately, the genesis of social entrepreneurship activity in a region may be a viable way to overcome some of these gaps. Kovner and Lerner (2015) found that even though the community development VCs in their sample were less likely to have successful exits of investments, they tended to bring traditional VCs to previously underserved regions. By remaining cognizant of systemic barriers that prevent access to capital and taking appropriate corrective actions, social entrepreneurs and impact investors can begin to correct these potentially inefficient investment patterns.

Kelly Posenau is currently studying finance as a Ph.D. candidate at the University of Chicago Booth School of Business.

1 Cann, O. (2020, January 22). Measuring Stakeholder Capitalism: World’s Largest Companies Support Developing Core Set of Universal ESG Disclosures. World Economic Forum. www.weforum.org/press/2020/01/measuring-stakeholder-capitalism-world-s-largest-companies-support-developing-core-set-of-universal-esg-disclosures/

2 UN Secretary-General’s Strategy for Financing the 2030 Agenda – United Nations Sustainable Development. (n.d.). Retrieved August 14, 2020, from www.un.org/sustainabledevelopment/sg-finance-strategy

3 Kölbel, J. F., Heeb, F., Paetzold, F., & Busch, T. (2019). Can Sustainable Investing Save the World? Reviewing the Mechanisms of Investor Impact. Working paper.

4 Mudaliar, A., & Dithrich, H. (2019, April 1). Sizing the Impact Investing Market. The GIIN. https://thegiin.org/research/publication/impinv-market-size

5 Trelstad, B. (2016) Impact Investing: A Brief History. Capitalism and Society, 11, 4, 1-14.

6 Ibid.

7 Barber, B.M., Morse, A., Yasuda, A. (2019) Impact Investing. Journal of Financial Economics, forthcoming.

8 Kovner, A. & Lerner, J. (2015). Doing Well by Doing Good? Community Development Venture Capital. Journal of Economics and Management Strategy, 24, 3, 643-663.

9 Gray, J., Ashburn, N., Douglas, H., Jeffers, J., Musto, D., Geczy, C. (2015) Great Expectations: Mission Preservation and Financial Performance in Impact Investing. Wharton Social Impact Initiative Report.

10 Hartzmark, S.M. & Sussman, A.B. (2019). Do Investors Value Sustainability? A Natural Experiment Examining Ranking and Fund Flows. Journal of Finance, 74, 6, 2789-2837.

11 Berg, F., Kölbel, J.F., & Rigobon, R.(2020). Aggregate Confusion: The Divergence of ESG Ratings. Working Paper. Retrieved from: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3438533

12 Kölbel, J. F., Heeb, F., Paetzold, F., & Busch, T. (2020). Can sustainable investing save the world? Reviewing the mechanisms of investor impact. Organization & Environment. doi:10.1177/1086026620919202