Can I Ever Retire?: The Effects of COVID-19 on Financial Security

The rise of personal retirement responsibility

The global COVID-19 pandemic is a health crisis unlike any other in recent times and will have a devastating effect on many of those directly affected by the illness. It is becoming clear that the wider economic and financial ramifications will affect many more, though perhaps less critically. Job losses and economic insecurity will likely disturb millions, and the financial losses suffered by substantial market declines will be felt by the tens of millions of Americans who are increasingly responsible for financing their own retirements.

Job losses and economic insecurity will likely disturb millions, and the financial losses suffered by substantial market declines will be felt by the tens of millions of Americans who are increasingly responsible for financing their own retirements.

One of the biggest shifts in household finance during the last 30 years has been the move toward defined contribution, or DC, retirement vehicles such as 401(k) plans. As most of us know, these plans are typically sponsored by employers, who often provide some matching funds, but are ultimately individual accounts owned by employees. While there are many benefits to DC plans, such as immediate vesting of individual contributions and continued ownership when changing jobs, they are not a retirement panacea. In fact, DC plans inherently put additional responsibility and risks in the hands of employees. DC plan participants bear the full risk of investments they make, as well as the responsibility for funding accounts at a level sufficient to maintain their desired lifestyle in retirement (supplemented by any other assets they may have, of course).

As a consequence, large market declines like those experienced during the 2001-2002 tech bubble burst, the 2008 global financial crisis and, most recently, the 2020 COVID-19 pandemic can significantly affect the retirement prospects of DC plan participants. In this analysis, we consider a hypothetical saver in our current economic situation as an example for understanding the risks posed by such market declines.

What’s at risk?

Managing one’s own retirement savings is a big responsibility and most individuals do not have the time or investment expertise to closely oversee their own DC plan assets. Furthermore, most have very limited access to such expertise through their employer or professional financial planners. The sudden decline in markets is a big risk for at least a couple of reasons. First, a large market decline results in an immediate loss of value in retirement savings for those allocated to risky assets like stocks. Second, and just as dangerous (as shown below), there is the risk that a saver panics and sells when markets suddenly drop. For example, by panicking right now, savers run the risk of selling at the bottom of a big market decline. Many households did this during both the 2001-2002 and 2008-2009 market dips and effectively locked in large losses.

Perhaps even worse, many of these panicked investors subsequently returned to stock investing after markets had recovered a few years later and set themselves up for the next downturn. The lesson here is that the fear and instincts of individual investors can substantially disturb their retirement prospects.

So, really, when can I retire?

What should those saving for retirement do? First, savers should have a good feel for their level of risk tolerance. It may be too late to deal with that in the current situation, but hopefully people have some notion for the amount of risk they should be taking. A commonly used rule of thumb is that investors should allocate about 100 percent minus their age to stocks. Using this rule, for example, a 40-year-old worker should be allocating 60 percent (100 minus 40) of their portfolio to risky assets like stocks. We then assume that the other 40 percent of savings is allocated to safer assets like bonds.

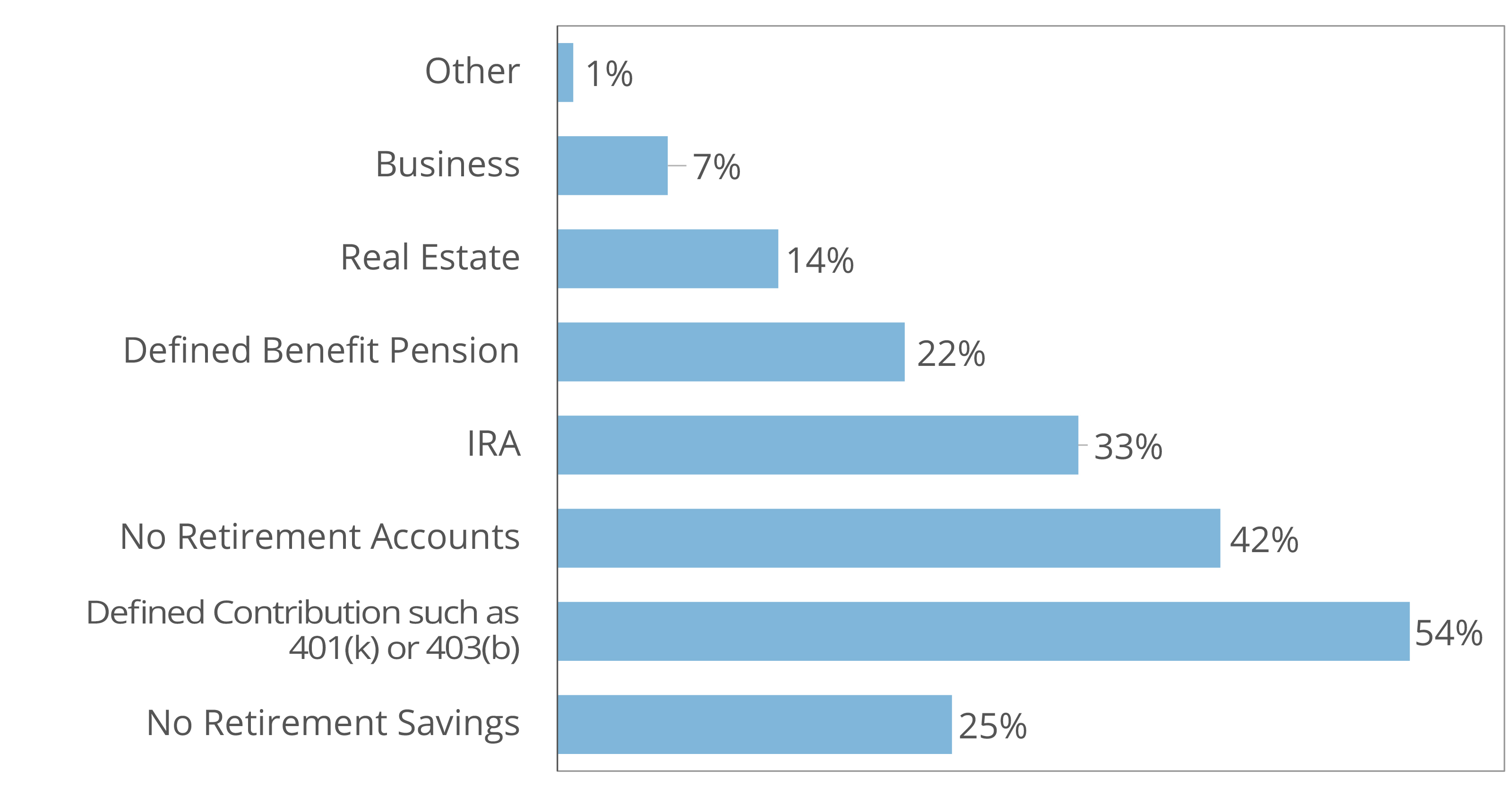

*Respondents can provide multiple answers. Source: Federal Reserve Board of Governors

We can calculate what might happen under a few different scenarios to the retirement prospects for this saver based on current conditions and different behaviors. By making a few reasonable assumptions, it’s possible to calculate some specific, albeit hypothetical, numbers. First, let’s assume that the saver started the year with $500,000 in their 401(k) and plans to work until they have enough savings to guarantee a $70,000 distribution each year from their account until age 85. Let’s also assume reasonable numbers for average annual returns going forward on stocks (seven percent) and bonds (two percent).2

| Scenario | Retirement Age |

|---|---|

| No current crisis (benchmark case) | 62 |

| Hold steady (keep 100%-minus-age stock allocation) | 66 |

| Short panic (move to all bonds for 5 years) | 68 |

| Permanent panic (move to all bonds forever) | 74 |

As a benchmark case, we begin by assuming that the current downturn never happened and our saver follows the allocation rule of investing 100 percent minus their age in stocks until retirement. In this idyllic scenario, our saver would be able to meet their goal and retire at age 62—not bad. Of course, the current downturn has had a big impact on portfolio values, so for the next scenario, let’s assume that the value of the retirement plan assets declines by 20 percent in 2020, but our saver stays true to the 100 percent-minus-age stock allocation rule. In this case, retirement will have to be postponed until age 66—a fairly significant extension in expected working age based on conditions largely outside the control of our worker. So, we see that a portfolio shock like what we have seen so far in 2020 (and much less than that experienced in 2001-2002 and 2008-2009) can potentially have a significant impact on retirement age.

Some might argue that market fluctuations are short term and not related to long-term value created through investing in stocks. This is a possibility and would certainly shorten the extension in working years noted above. But what is more certain is the negative impact if our saver panics in the face of market declines and moves to an all-bond or all-cash position. Next, we can consider the case where the market decline causes our 40-year-old saver to panic and convert to all bonds for five years before returning to the 100 percent-minus-age stock allocation rule. In this case, the short-run change in allocation pushes back the hypothetical retirement age another two years to age 68. But the biggest risk occurs if our saver permanently moves to an all-bond position. In this case, the expected retirement age is moved back yet another six years to age 74. Alternatively, our saver could retire earlier, but with potentially much less income to sustain them in their golden years.

This is a very simple and stylized example, but it makes it clear that retirement savers relying primarily on DC plans face two important sources of risk. First, the variation in market returns, even for a reasonably allocated portfolio, can have a meaningful impact on retirement ages and incomes. Second, plan participants’ own actions can greatly affect their retirement prospects.

Target-date funds to the rescue?

One of the best developments in the last decade for DC plans has been the trend toward default allocation into target-date funds. Target-date funds allocate to risky assets like stocks, as well as safer assets like bonds, and slowly change the mix of assets over time, with the goal of matching the risk profile of savers (like the 100 percent-minus-age rule of thumb). These so-called “glide paths” are written into the objectives of the funds and rebalancing is done automatically by the fund manager. All investors have to do is pick the right vintage of target date (e.g., 2045 for our hypothetical 40-year-old saver) and relax. Empirically, it seems that DC plan participants both do better and feel better letting a professional manager handle the asset allocation and the underlying investments.

1 Federal Reserve (2019). Report on the Economic Well-Being of U.S. Households in 2018. https://www.federalreserve.gov/publications/files/2018-report-economic-well-being-us-households-201905.pdf

2 Of course, actual returns will fluctuate, and ultimately differ from these, but these values are reasonable averages given current market conditions and allow for first-order approximation of the effects we seek to illustrate.