- The U.S. economy is expected to weaken this year, yet the extent of the deceleration is uncertain. Our base case is a mild recession in the middle of the year.

- In this scenario, slower activity is forecast for almost all of our 150 Extended Metropolitan Areas, with 26 experiencing outright decline, a higher concentration of those among our midsize cities.

- In a soft-landing scenario, most of our microeconomies would experience slower growth this year than last.

- High interest rates are expected to weigh on housing in 2024, with large variation across microeconomies, affecting growth trajectories.

The U.S. economy grew 1.9% in 2022, the most recent year for which the government has released local area GDP numbers, yet in the same year, 26 of the 150 Extended Metropolitan Areas that we analyzed contracted. The American Growth Project seeks to measure these microeconomies in near-real time and understand the drivers of this variation. We anticipate a mild recession in the middle of this year, a forecast given with a significant dose of humility as we acknowledge that the mild recession that we expected in the second half of 2023 or early 2024 has not materialized. Our models indicate that all 150 EMAs will experience slower growth in 2024 than they did in 2023, and 26 EMA economies will contract.

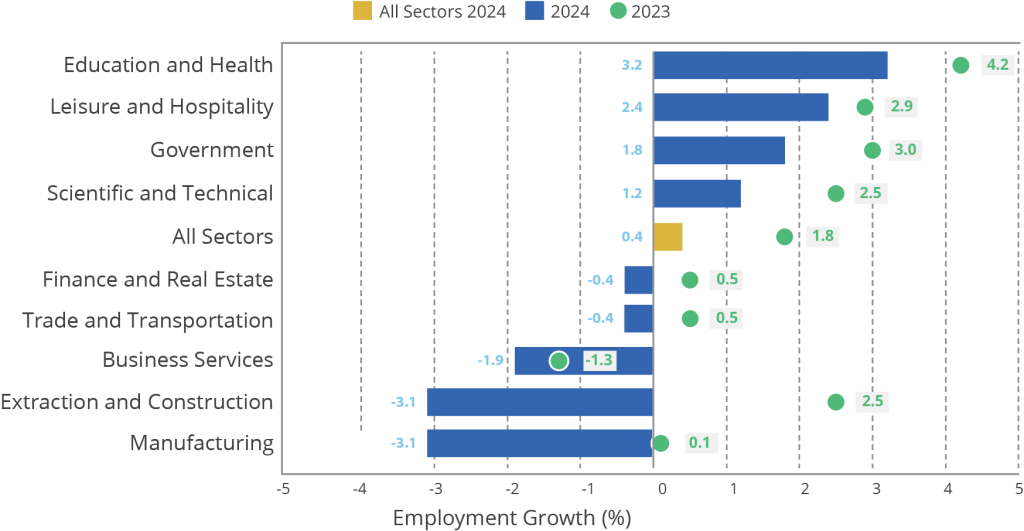

Austin’s growth prospects remain the strongest among our 50 largest microeconomies, with healthy local growth characteristics offsetting softening demand. Meanwhile, Oklahoma City is a notable climber, moving up five slots from last year to No. 9 in our top 50 ranking, bolstered by the strength of its labor market. Oklahoma City’s move is a nice illustration of how an area’s industrial makeup affects growth. The city has a larger-than-average share of its labor force in construction – a characteristic discussed below as an economic drag – yet it is underweight in Manufacturing, meaning limited exposure to an expected sectoral slowdown, and overweight in Government, a sector likely to be resilient to economic headwinds. These factors combine to support OKC’s growth prospects relative to other cities. We expect job creation to be less favorable in this year than in last in every sector of the economy – with industries such as Extraction and Construction anticipated to experience outright declines and the biggest shift in growth trajectory. The weakening labor market is a key reason why we forecast all our EMAs to experience slower growth in 2024 than in 2023.

U.S. Employment Growth by Sector

2024 vs. 2023

Housing Challenges

Federal Reserve rate hikes have so far only moderately impacted the national economy, yet their effects will increasingly weigh on housing activity this year. Building permits, which are an important leading indicator of housing activity, declined nationally by 11.7% in 2023. As the map below illustrates, there is significant variance in outcomes among microeconomies. Many of our 150 EMAs saw declines in new housing permits – some exhibiting double-digit drops (shown in deep red in the map below) – and one-quarter of the EMAs showed gains, which we expect will translate into an increase in housing activity in those areas in 2024.

The gains in housing, however, are unlikely to offset weakness in other sectors driving the growth slowdown. Louisville, for example, which has the strongest gains in permits among our 50 largest cities, is still expected to experience minimal job gains this year, largely resulting from its less than favorable industry mix. The EMA is overexposed to the Manufacturing and the Trade and Transportation sectors, which include retail and warehousing and which are forecast to lose jobs. Meanwhile, Louisville has a smaller-than-average employment share in Government, which is forecast to grow, albeit more slowly than last year. Despite these anticipated economic frictions, the Derby City’s economy is still expected to grow in 2024 and move up the large-city rankings fifteen places, into the middle of the pack.

Soft Landing, Still Slowing

The economic environment we anticipate is not particularly favorable to the many communities that continue to experience housing shortages. A slowdown may bring lower interest rates, yet weak economic growth is not an environment in which businesses and households would normally undertake large investments in housing or other expensive, long-lived assets. The backdrop of weak housing permit numbers is itself a headwind, at least this year. How local communities deal with housing shortages is centrally important to their long-term growth prospects.

As we discuss in our Five Economic Trends to Watch in 2024 forecast, uncertainty abounds, from how much the Fed will cut rates (or if it may even raise them further) to how rising geopolitical uncertainty stemming from the U.S. election and foreign wars will affect consumer and business behavior. Embodying some of this uncertainty, we modeled a soft-landing scenario estimating how a paradigm of consistent moderate growth would impact our EMAs. Under this alternative model, we found that over two-thirds of the microeconomies would still experience a slowdown. So even under a rosier scenario of continued economic expansion, growth will still slow from an unexpectedly strong 2023. And given the diversity of America’s microeconomies, even in a solid growth environment, some areas gain while others lag behind.

This post was updated Jan. 30, 2024, to reflect latest data.