It’s no surprise that investors want access to the best performing assets for their portfolios. Many providers of defined-contribution (DC) investment plans, such as 401(k)s, have advocated for broader access to private investments in those plans. But can access to private funds really happen, given operating, regulatory and legal constraints? Perhaps more important, should it? Or more specifically, what is the evidence suggesting that gains from investing in private funds are likely to accrue to retail investors?

What’s the fuss about?

Last June, the prospects for investments in private funds by retail investors through DC plans were boosted by an Information Letter written by the U.S. Department of Labor (DOL) that effectively provided a clear path for DC plans to invest in such funds.1 The letter did not simply answer the question of inclusion of private equity (PE), but provided a detailed outline of how to create such an investment. Most important, plans must offer the PE investment as part of a multi-asset class vehicle with the structure of a custom target date, target risk or balanced fund. In addition, these multi-asset class vehicles would be required to have sufficient exposure to other assets and the proportion allocated to PE must remain below a specified threshold.

With more and more of the capital of our economy being allocated to private markets, it’s important to understand the impact of allowing private funds in defined-contribution plans. As some critics have pointed out, the merits of including PE investments in DC plans are not easily understood and are open to much speculation and interpretation.2 In this analysis, we contrast the desire to allow equal access to investment opportunities with the need to protect unsophisticated investors with regulated “seatbelts and airbags” to keep them from harm. We also consider the need to educate investors of the possibility of lower-than-expected returns.

Potential Benefits

A necessary condition for including private funds in DC plans is that participants should reasonably expect to obtain overall portfolios with better returns, lower risk or both.

Access to better-returning investments

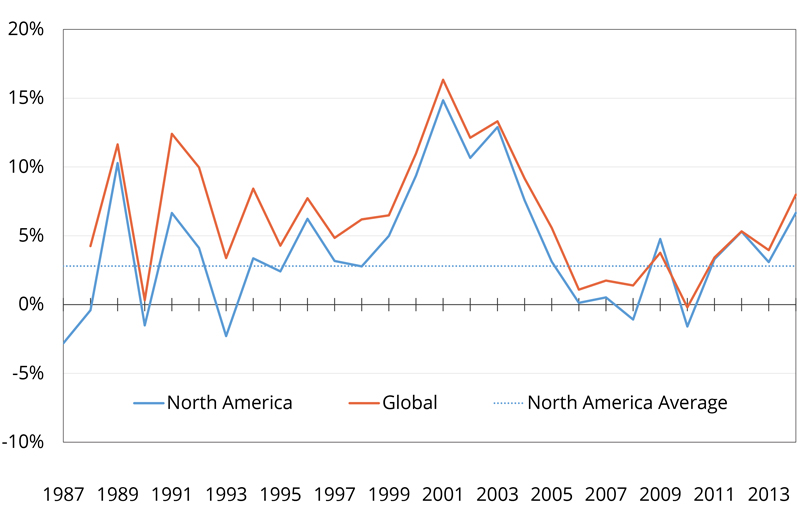

Of all the potential benefits of the inclusion of PE investments in a DC plan, the most fundamental is access to higher-returning assets. Using data from Burgiss, Brown and Kaplan (2019) document that U.S. buyouts have outperformed the S&P 500 by roughly 3.5% and find only a modest decrease in this outperformance when considering only vintage years 2009-2014.3

Here we update performance statistics through December 2019 and provide the results in Table 1. Values reported are annual direct alphas (see Gredil, Griffiths, and Stucke, 2014) based on all buyout funds with a North American focus (first row) and all global buyout funds including North American funds (second row). These alphas measure net-of-fee performance over and above public market benchmarks.4 Figure 1 plots performance by vintage year through December 2019.5 The results show that while there is variation in performance based on geographic focus, time horizon and vintage year, buyout funds have outperformed broad public benchmarks by about 3% or more on average.

| Table 1. Private Equity Performance vs. a Public Market Benchmark (Direct Alphas Through December 2019) |

|||||

|---|---|---|---|---|---|

| 5-year | 10-year | 15-year | 20-year | Since Inception | |

| North America (vs. Russell 3000) | 3.1% | 1.2% | 3.7% | 3.9% | 2.8% |

| Global (vs. MSCI-ACWI) | 3.9% | 3.2% | 4.7% | 5.7% | 6.5% |

Source: Burgiss. |

|||||

Source: Burgiss, data through December 2019.

Better portfolio diversification

Although the last 20 years have witnessed a decline of publicly traded (especially small-cap value) companies, retail investors in PE would likely gain access to a wide range of small companies.6 Thus, even if the PE investments offer only a fair return per unit of total risk (ex ante), there are potential diversification benefits to a portfolio. A recent analysis by Goetzmann, Gourier and Phalippou (2019) decomposes private fund returns into a set of risk factors and finds substantial diversification benefits from private funds.7 The authors note, “Perhaps some assets perform better, or more true to their underlying factor exposures, when held by private capital. … private markets provide exposures that public markets do not, thereby offering an additional source of factor risk premia.”

Other potential benefits

In addition to an increase in risk-adjusted returns, there are other potential benefits. Expanding the set of investors with the ability to invest in private capital will likely expand the pool of capital available for private fund investments. Given that many of the fastest-growing and innovative companies are increasingly preferring to stay private longer, the increase in capital supply should expand access to capital for these companies. Finally, there is a fundamental question of equity: Is it fair to restrict access to the highest returning investments? This is an especially poignant question given trends toward higher wealth and income inequality in the U.S. If proper fiduciary conduct is enforced, it seems unethical to categorically exclude investors from substantial and still growing opportunities in private investment funds that are afforded to all types of institutional investors and wealthy individuals.

Potential Drawbacks

Although clearly there are potential benefits to providing access to private funds in DC plans, there are also potential disadvantages. For one, the exact structure for the implementation of such a plan is still to be determined and there is uncertainty around which method will prove to be best.

Fees will be higher than in public equity

By the nature of the investment, fees are likely to be higher for plans that include private equity sleeves. Private investments require additional due diligence as well as more complex monitoring and internal accounting. While these costs may be effectively outsourced to a specialized manager or fund of funds (FoF), they ultimately must still be borne by investors. It is not guaranteed that excess returns in PE would cover additional costs. Harris, Jenkinson, Kaplan and Stucke (2018) find that private equity FoFs outperform public markets historically, but also underperform direct fund investments.8

Future returns may be lower

One current concern surrounding PE is the growing amount of committed but unused capital or “dry powder” across the industry. Although having deployable assets may not be a problem, Braun and Stoff (2016) find that the cost of PE investing has increased in recent years, and this increase is driven by factors related to higher levels of dry powder as capital has moved into the PE industry.9

Risk-adjusted returns may be below public markets

When considering PE fund returns, we need to evaluate the risks underlying those returns. In general, the academic literature indicates that PE funds are riskier than public market indices, so estimates of risk-adjusted returns to PE are less favorable to the asset class than unadjusted return comparisons. Korteweg (2019) conducts a broad survey of risk estimates in the PE literature.10 He concludes that the risk of PE funds tends to be higher than that of the market index, with an estimated beta (risk multiplier) in the range of 1.3.

Liquidity risk is inherent in the asset class and may not be properly addressed

Research suggests that a portion of the historical return premium earned by PE investors is compensation for bearing illiquidity risk. These studies raise the question of what would happen to an illiquidity premium for DC plan investors. In order to gain access to the trillions of dollars in the 401(k) market, GPs may need to devise costly mechanisms that provide additional avenues for liquidity to plan participants. As such, the cost of these new facilities may inherently absorb a private markets illiquidity premium so as to provide no net (or even a negative) benefit.

Lack of transparency and access

Beyond the aspect of the complicated structure and additional fees, there are reasons for restrictions on private funds. The issue of disclosure, or lack thereof, in PE is potentially worrisome. Not only are investors subject to dealing with a lower quantity of disclosure by private funds, but studies have found that the quality of reporting for private firms (e.g., portfolio companies) is lower than for public firms in a variety of dimensions.11

With now thousands of PE funds, how will plan providers choose specific investments for their portfolios. The historical data suggest much wider variation in PE fund performance than is observed for public asset portfolio performance (e.g., for mutual funds). Because it is not practical to invest in all PE funds (in contrast to a public market index that invests in all stocks), there is then potential for substantial fund selection risk.

So where does this leave us?

Overall, a number of potential benefits may come from allowing DC plans to invest in private funds. As PE becomes an increasingly greater component of the overall economy, retail investors may need access to this market to be fully diversified. Even if the higher returns are only fair compensation for the higher risk borne by the investor (rather than an excess risk-adjusted return), this inclusion of PE funds would still provide greater diversification and higher overall portfolio returns. Access to PE through well-structured DC plans also give retail investors relatively safe access to investments previously only available to institutions and the very wealthy.

These enticing benefits need to be weighed against potential challenges and costs that may arise from creating broader access to private funds. The complicated structure and uncertainty around the mechanism to provide required liquidity backstops may bring increased fees. If liquidity is provided and fees are incurred, this may remove both the diversification and return benefits and therefore remove the incentive for including PE funds in DC plans to begin with.

Whether access to private investments provides a net benefit for DC plan participants will depend both on how private fund investments perform in the future as well as on how institutional features around plan participation evolve.

This insight was abstracted from “Should Defined Contribution Plans Include Private Equity Investments?” Read the full report. Contributing Authors: Greg Brown, Keith Crouch, Andra Ghent, Bob Harris, Yael Hochberg, Tim Jenkinson, Steven Kaplan, Richard Maxwell, and David Robinson. The corresponding author is Greg Brown, UNC Kenan-Flagler Business School, CB-3440 Kenan Center Room 301, Chapel Hill, NC, 27516 USA, [email protected]. The authors thank TJ Carlson, Tim Riddiough and Andrea Carnelli Dompé for valuable comments. The authors also thank Burgiss for providing data for the analysis.