As the dust continues to settle from the 2020 U.S. election, Congress is slated to restart negotiations for additional stimulus relief for workers and companies. Although the jobs report for October saw the unemployment rate decrease by a percentage point to 6.9 percent, job growth has continued to slow, and the overall number of jobs in the U.S. is 10.1 million below the February (i.e., pre-pandemic) rate.1 With COVID-19 cases on the rise, much uncertainty remains about the country’s economic future and what additional havoc the pandemic could inflict on its economy. Corporations in certain industries and small businesses will likely continue to struggle, requiring infusions of capital to stay afloat. Although the government currently plays an outsized role in providing capital to these businesses in need, the long-term business recovery will require private sector capital providers to be part of the solution.

Fundamental Changes to Risk Assessment by Capital Providers

It will be a long time before any sort of “business as usual” returns to the U.S. private sector. Achieving pre-pandemic output levels will require substantial financial investment. Since March, a large fraction of new capital entering the economy has come from government sources. More than $3 trillion in federal fiscal stimulus has already been provided directly to households and businesses primarily through the CARES Act, with additional funding currently being discussed in Congress. In addition, the Federal Reserve has instituted unprecedented support programs for credit markets (and indirectly, public equity markets).2 However, private sector providers of capital will necessarily drive long-run business investment, and the pandemic has caused a massive change in the risk profile of many businesses. A risk reassessment by capital providers will fundamentally change the amount, type and mix of capital allocated to private sector businesses.

(Percent, Option-Adjusted)

Source: Bank of America Merrill Lynch 3

To date, public companies have benefited from the Fed’s massive liquidity injection, and fortunately public equity and debt markets are now functioning normally. Capital access for private companies is more of a mixed bag. There is substantial liquidity at the large end of the institutional private equity market, supported by record levels of committed but undeployed capital at the start of 2020. Deal volume in the first half of the year was slow, but is accelerating in the second half and likely will reach record levels in 2021. Increasingly, this capital will also be available to middle-market companies as conditions further stabilize. However, the lower-middle market and many small companies are in very bad financial shape.4 Many businesses will not be viable until the recovery fully takes hold, and the increasingly uncertain timeline is holding back capital.

Shifting Risks in a Time of Great Uncertainty

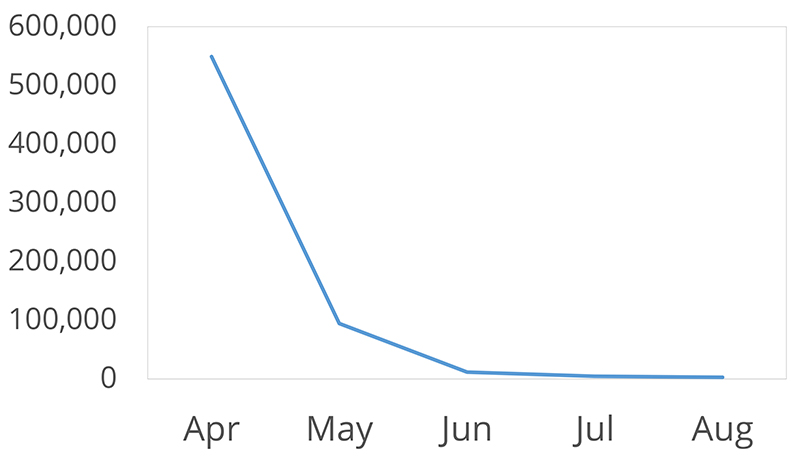

The fundamental issue faced by capital providers is the shifting risks in the economy brought about by the pandemic. Companies that were once assumed to have very predictable cash flows, even through a recession, have instead experienced previously unimaginable shocks to revenues.5 Furthermore, the radical uncertainty around the pandemic’s future course generates more financial risk than many investors can tolerate. For example, banks’ commercial and industrial (C&I) loan books have been battered, and the six largest U.S. banks have set aside $36 billion in reserves to date for future loan losses.6 Banks were very efficient in doling out PPP loans to small businesses, but with these funds drying up, there will be a careful reassessment and scaling back of C&I lending activity. The banking sector overall is unlikely to be a source of new capital for most small businesses desperately in need of it. This decline in capital supply is exacerbated by low levels of private-fund institutional capital (both debt and equity) in the lower-middle market.

(April-August 2020)

Source: U.S. Small Business Administration7

Opportunities for Savvy Investors

Given this severe dislocation, the lack of current funding sources delivers a great opportunity for new capital providers who can solve two problems. First, investors must be able to ascertain forward-looking business risks and, in many cases, provide operational expertise in navigating these risks. There is no existing playbook for the type of evaluation needed in many industries, but savvy investors will be able to devise new methods and management practices. Second, investors will need to identify what structures and platforms can quickly obtain capital from investors not currently active in the lower-middle market and small business segments. These may take the form of new traditional private credit and private equity funds, new small business investment companies (SBICs) and even entirely new structures currently under consideration in federal legislation to support small businesses.8

1 U.S. Bureau of Labor Statistics. (2020, November 6). Employment Situation Summary — October 2020. Retrieved from https://www.bls.gov/news.release/empsit.nr0.htm

2 Martin, F. (2020, July 16). The Impact of the Fed’s Response to COVID-19. St. Louis Fed. Retrieved from https://www.stlouisfed.org/on-the-economy/2020/june/impact-feds-response-covid19

3 Retrieved from Federal Reserve Bank of St. Louis (2020).

4 Caniato, F., Moretto, A., & James B. Rice, J. (2020, August 6). A Financial Crisis Is Looming for Smaller Suppliers. Harvard Business Review. https://hbr.org/2020/08/a-financial-crisis-is-looming-for-smaller-suppliers

5 Akers, J., & Nicum, P. (2020, May 13). The Secondary Market under COVID-19. Adams Street Partners. https://www.adamsstreetpartners.com/news/the-secondary-market-under-covid-19-learning-from-the-great-financial-crisis/

6 Forsyth, Randall (2020). Banks’ Loan-Loss Reserves Send Sharp Warning on Economy. Barrons. https://www.barrons.com/articles/banks-loan-loss-reserves-send-sharp-warning-on-economy-51595032237

7 Small Business Administration (2020). Paycheck Protection Program. Data retrieved August 26, 2020. https://sba.app.box.com/s/ox4mwmvli4ndbp14401xr411m8sefx3i

8 See for example, section 321 of the HEALS Act: Coronavirus Response Additional Supplemental Appropriations Act. S. 4320 116th Cong. (2020).