- After a blockbuster employment report, we expect to see some moderation in job gains for February when the data is released on Friday. We will be closely watching for any major downward revisions.

- These job numbers have caused some economists to move away from their hard landing (recession) forecasts, with some even penciling in a “no landing” scenario.

- Our research suggests those moving away from a recession call are being shortsighted.

- Thus, we are hardening our late 2023/early 2024 recession stance, as it means that the Fed is going to have to be more aggressive, as Federal Reserve Chair Powell indicated yesterday.

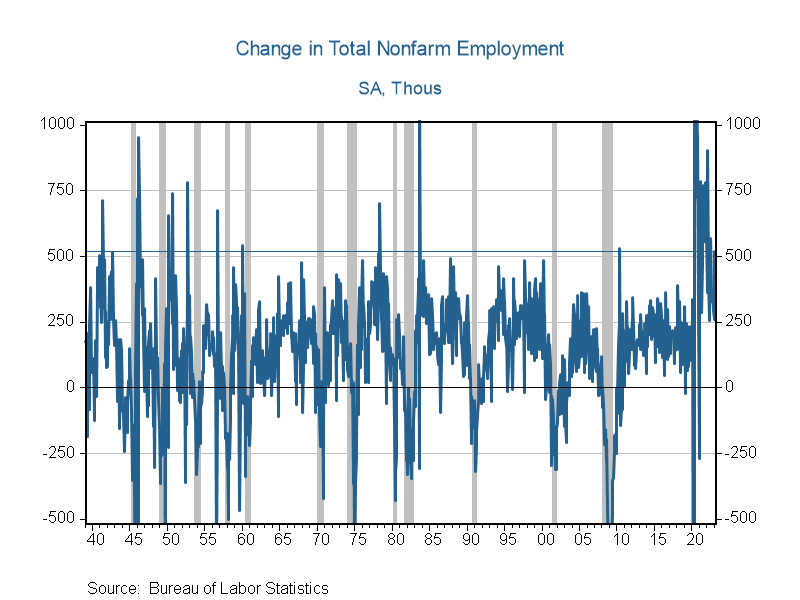

An astounding 517,000 jobs were created in January 2023. To put that into perspective, in the 84 years of data on record, only 30 months – 3% of all months – have reported job gains this strong (see the Change in Total Nonfarm Employment graph below). Moreover, 18 of those 30 months have taken place since the beginning of the COVID-19 pandemic, with many of the others occurring at the end of labor strikes or in the early parts of an economic recovery.

However, unlike mid-2020 or even 2021, we have an extremely tight labor market. The unemployment rate currently sits at 3.4%, which marks a 54-year low. Adjusting for the size of the labor force, 22% of months had job creation on par with January – with the vast majority of those occurring when the labor force was growing a lot faster than it is today. Thus, when we account for the tightness of the labor market, job creation on par with January occurred only 6% of the time, with the last time taking place in March 2000; prior to that, the most recent month was in late 1973.

The general strength of the labor market to date raises an important question for businesspeople and policymakers – particularly the Federal Reserve. What is the likelihood of a meaningful slowdown or recession given this employment backdrop? Over the last 84 years, the probability of a recession occurring in the next three, six, and 12 months after this level of job gains is extremely low: only 2%, 4%, and 12%, respectively. As such, historical data might lead one to be optimistic that a recession is highly unlikely. But the jobs numbers are only half the story.

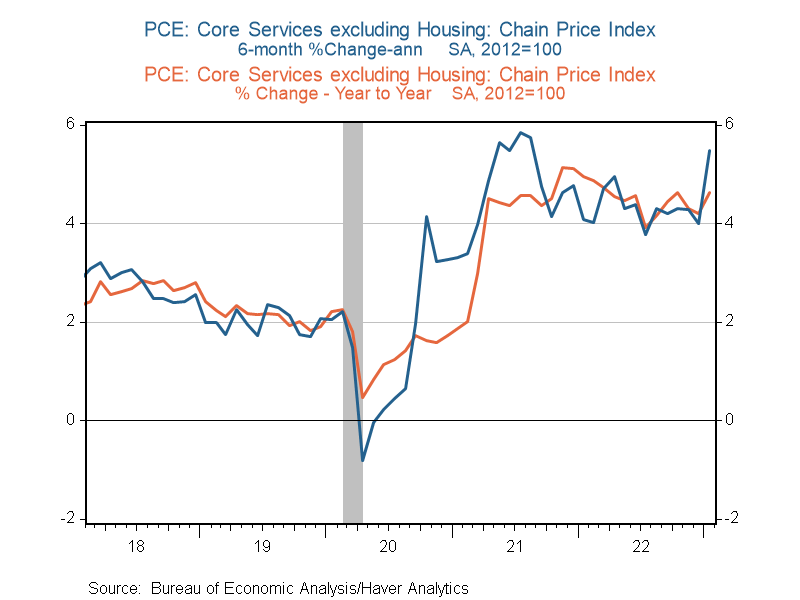

These statistics exacerbate an already sticky inflation problem for the Fed. Inflation remains stubbornly high, and after some slowing in the second half of last year, things seem to be moving in the opposite direction. The Fed’s preferred measure of inflation, the Personal Consumption Expenditure (PCE) price index, was up 5.4% in the year ending in January (recall that their target rate is 2%). Core services excluding housing – Chair Jerome Powell’s new preferred inflation measure – has shown even less of a downtrend. And it now looks like it’s reaccelerating, especially over the last six months (see the blue line in the chart below). The Fed lost some of its inflation-fighting credibility by not tightening more aggressively last year – and these readings aren’t helping matters. Thus, it is stuck having to be reactive to current inflation levels rather than in its preferred forward-looking position.

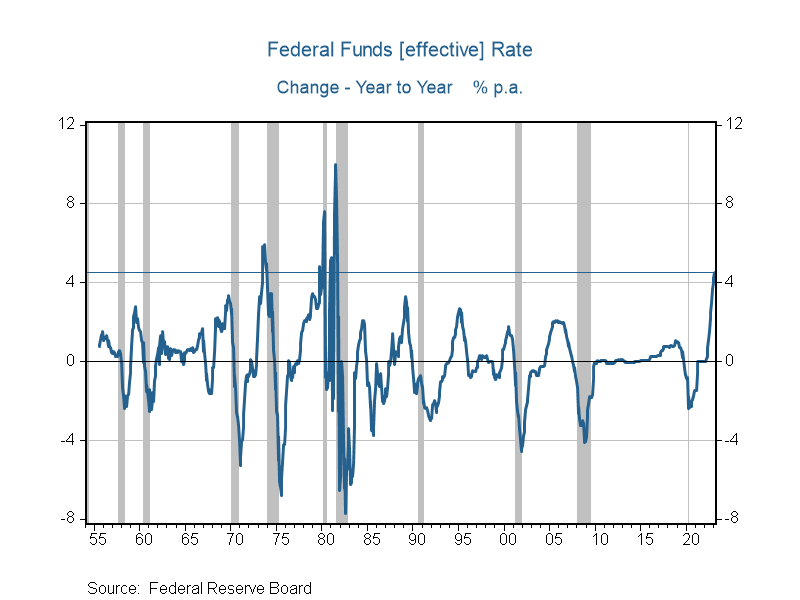

If it had been more aggressive a year ago, the Fed would argue that it’s already raised interest rates by 4½ percentage points and meaningfully contracted their balance sheet. This is likely to cause a soft landing at best and a recession at worst, which will push inflation lower. But it’s hard to make this case when your credibility is on already the line and the data is indicating that a near-term slowdown in both the economy and inflation is unlikely. This means that more rate hikes are coming down the pike. The markets have now priced in another three-quarters of a percentage point of rate increases and have essentially removed the rate cuts they anticipated later this year. That is a key reason why 10-year Treasury rates have increased roughly half a percentage point over the last few weeks and are now hovering near 4%.

This brings us back to our recession probabilities. Milton Friedman famously said that monetary policy works with “long and variable lags” and former Dallas Fed President Robert McTeer likened monetary tightening to drinking vodka; that is, “it sneaks up on you.” The Fed has never raised rates by 4½ percentage points – no less 5¼ percentage points on top of continued balance sheet contraction – without a recession ensuing. The current data suggests we are in the “not-really-feeling-it stage” – and our research suggests it will continue to take some time – but history suggests that is likely to be temporary. Recall the last two times when we had super strong job growth and a super tight labor market: March 2000 and late 1973. In both cases, the Fed was in the midst of a rate hiking cycle and a recession ensued within a year. Given these signs, unless something changes meaningfully on Friday, we are doubling down on our recession forecast.