Five Economic Trends to Watch in 2026

Want to know which issues are top of mind for business leaders as we enter 2026? Chief Economist Gerald Cohen gives you the big questions for the new year in his annual Five Trends.

Want to know which issues are top of mind for business leaders as we enter 2026? Chief Economist Gerald Cohen gives you the big questions for the new year in his annual Five Trends.

Join us Friday, December 5, at 9 AM EST as Research Fellow Greg Brown examines how federal agencies are tackling a historic data backlog and what it means for policy and business amid ongoing uncertainty.

Kenan Institute Chief Economist Gerald Cohen kicks off 2025 with a rundown of five issues that will be top of mind for business leaders and policymakers, accompanied by his analysis.

Chief Economist Gerald Cohen compared wage growth with inflation to answer some questions from USA Today.

Despite strong economic indicators—2.5% GDP growth, unemployment under 4%, and easing inflation—American consumer sentiment remains low. Kenan Institute experts explore why the public's mood doesn’t match the upbeat data, highlighting deeper sources of economic unease.

How can the economy be running above its potential output level and still experience declining inflation? Join Kenan Institute Research Fellow Greg Brown in the institute’s monthly virtual briefing at 9 a.m. EDT this Friday, April 5 to learn why.

Join Chief Economist Gerald Cohen for the institute’s monthly virtual briefing at 9 a.m. EST this Friday, March 8, to discuss the morning's employment report and the latest economic data.

By all accounts, there is steady good news coming the Federal Reserve’s way. And yet, the Fed seems to be in no rush to start cutting rates. Dive deeper into what the Fed will do to make sure inflation remains at that 2% goal.

Kenan Institute Senior Faculty Fellow Christian Lundblad will discuss Friday’s employment report and other economic issues during the institute’s monthly virtual briefing at 9 a.m. EST this Friday, Feb. 2.

The year ahead is full of economic uncertainty, but institute Chief Economist Gerald Cohen knows that some topics will be in the thoughts of many business leaders and policymakers. Find out five trends he has in mind.

Dive into the Kenan Institute’s monthly virtual press briefing from Friday, Jan. 5, as institute Chief Economist Gerald Cohen offered some economic trends to watch for 2024.

Inflation has come down but may still have some fight left in it. One concern is what happens going forward as the relief from pandemic price pressures disappears, but deflationary tailwinds are no longer there.

Join us for the Kenan Institute’s monthly virtual press briefing at 9 a.m. EDT this Friday, Dec. 8, as professor and former executive director Greg Brown shares his thoughts on where inflation may be headed from here.

Since March 2022, the Federal Reserve has battled the highest inflation in decades with interest rate increases whose effects are only now starting to be seen. So does this mean the era of rate hikes is coming to an end?

Join the Center for the Business of Health for sessions including the rising price of drugs, the influence of consolidation on healthcare prices and costs, and the AI boom and reducing healthcare prices. Meals are included for in-person attendees.

With gas prices on the rise, inflation numbers will look less favorable. How should the Federal Reserve handle this, and what does it mean for the economy? Join us for a discussion Friday.

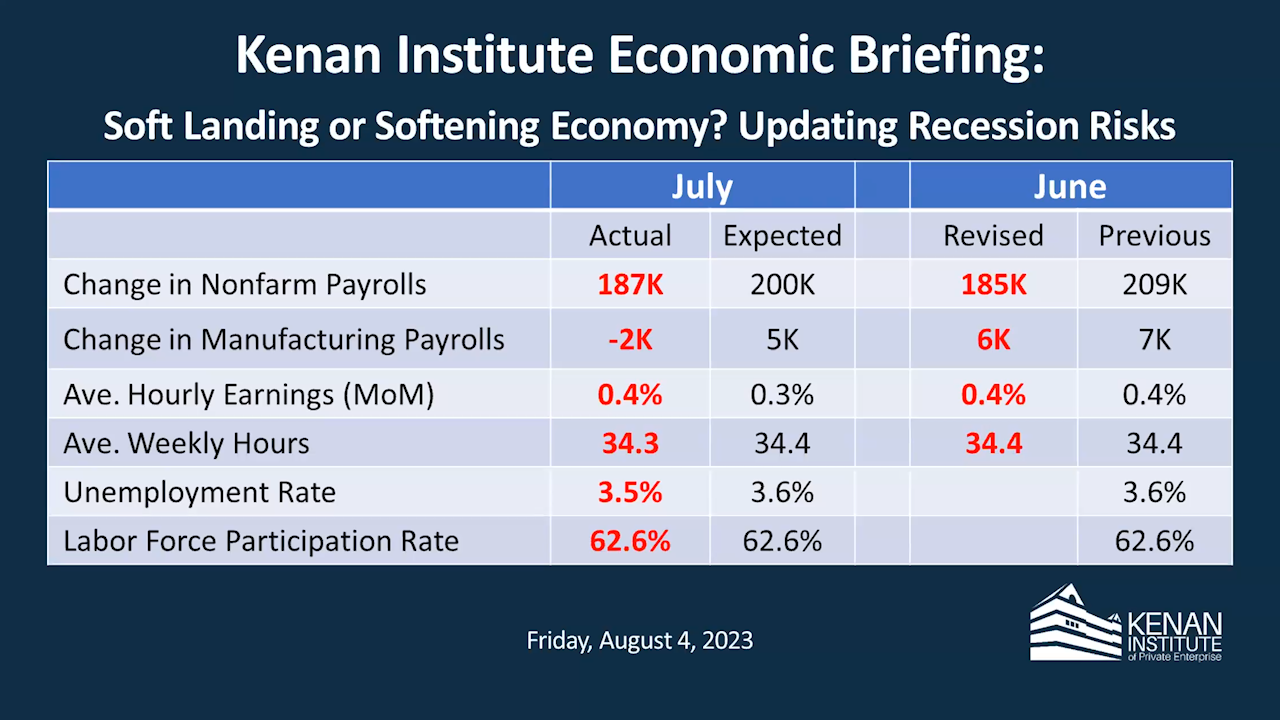

Have the chances of a recession arriving in the next year decreased? Institute Executive Director Greg Brown laid out the conflicting economic indicators around this question and offered his analysis of the Aug. 4 employment report, which showed 187,000 jobs added in July. He also answered questions on the yield curve’s performance and the potential effects of Fitch’s downgrade of the U.S. credit rating.

Join us for the Kenan Institute’s monthly virtual press briefing at 9 a.m. EDT this Friday, Aug. 4, as Executive Director Greg Brown discusses whether declining inflation has put an economic soft landing back on the table.

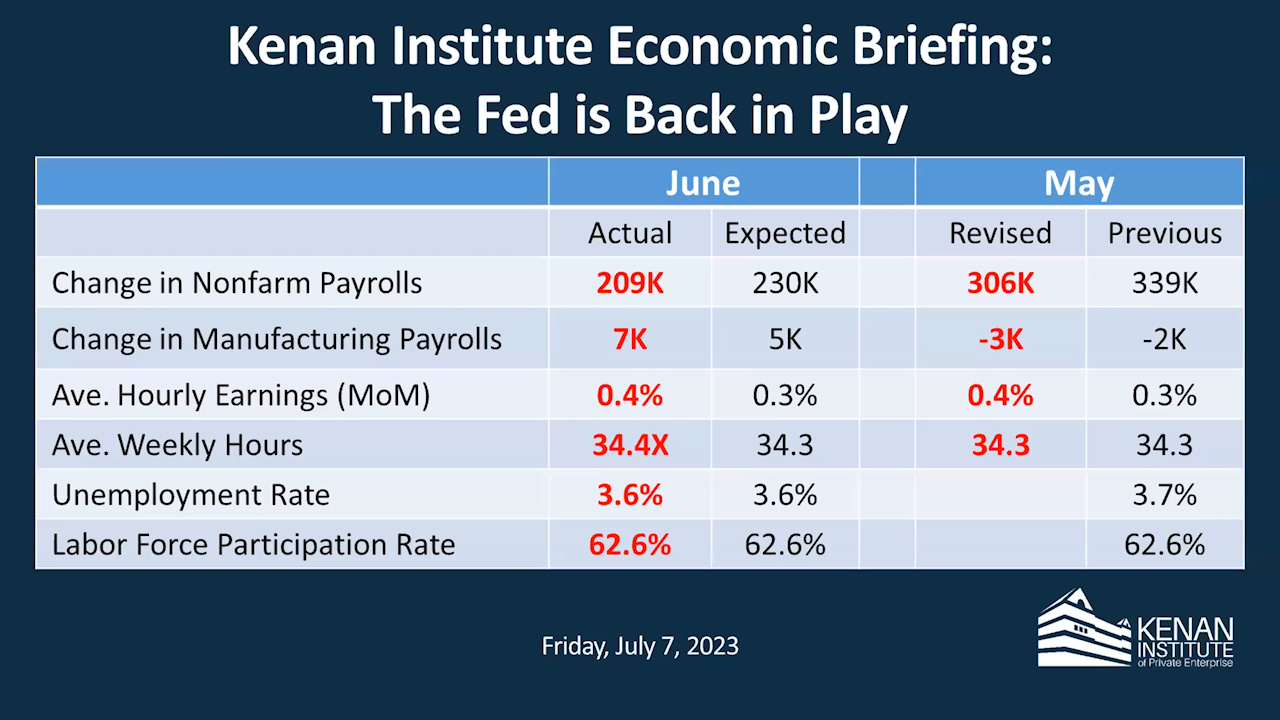

Institute Chief Economist Gerald Cohen offered his analysis of the July 7 jobs report, which showed an additional 209,000 jobs in June, and discussed why the Fed may be looking at interest rates increases in the near future but not beyond that.

Institute Executive Director Greg Brown offered his analysis of the June 2 employment report and talked about why now may be a good time to tackle the country’s spending and revenue issues.

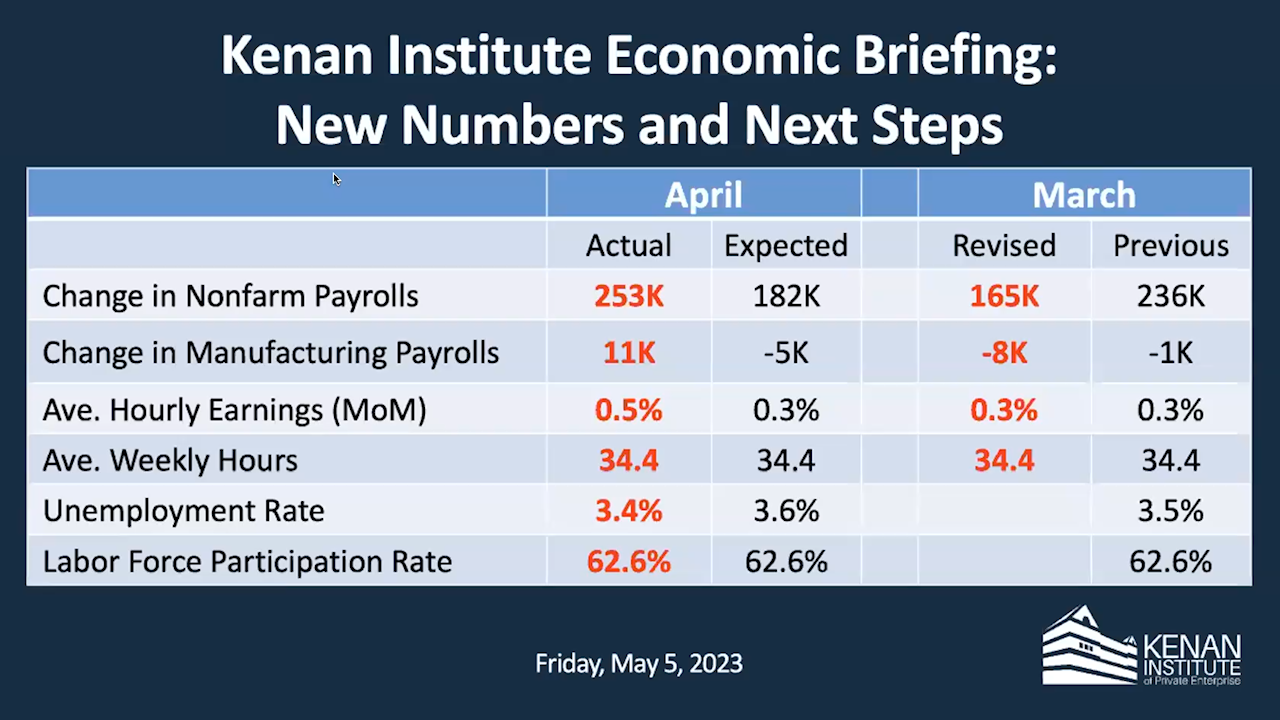

UNC Kenan-Flagler Business School’s Christian Lundblad offered his analysis of the May 5 employment report, which showed employers adding 253,000 jobs in April, far above forecasts. He also answered questions about the Fed’s next move and what a sharp revision in March’s numbers might mean.

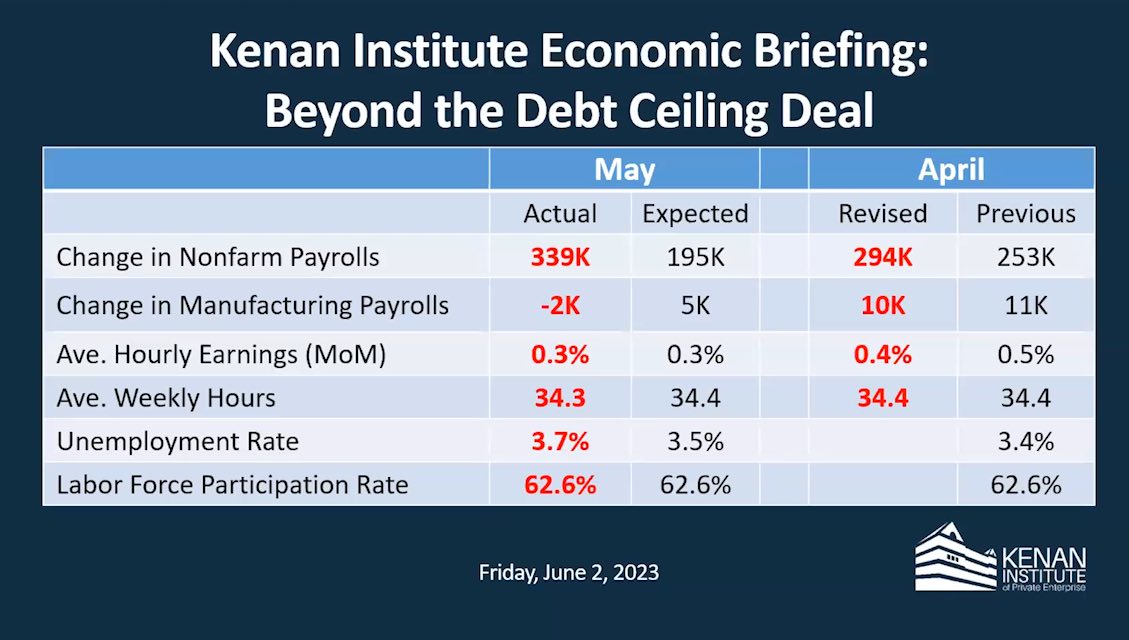

The economy continued to add jobs in March, but Chief Economist Gerald Cohen pointed out some underlying indicators that point to a slowdown. Also: effects from March’s bank collapses.

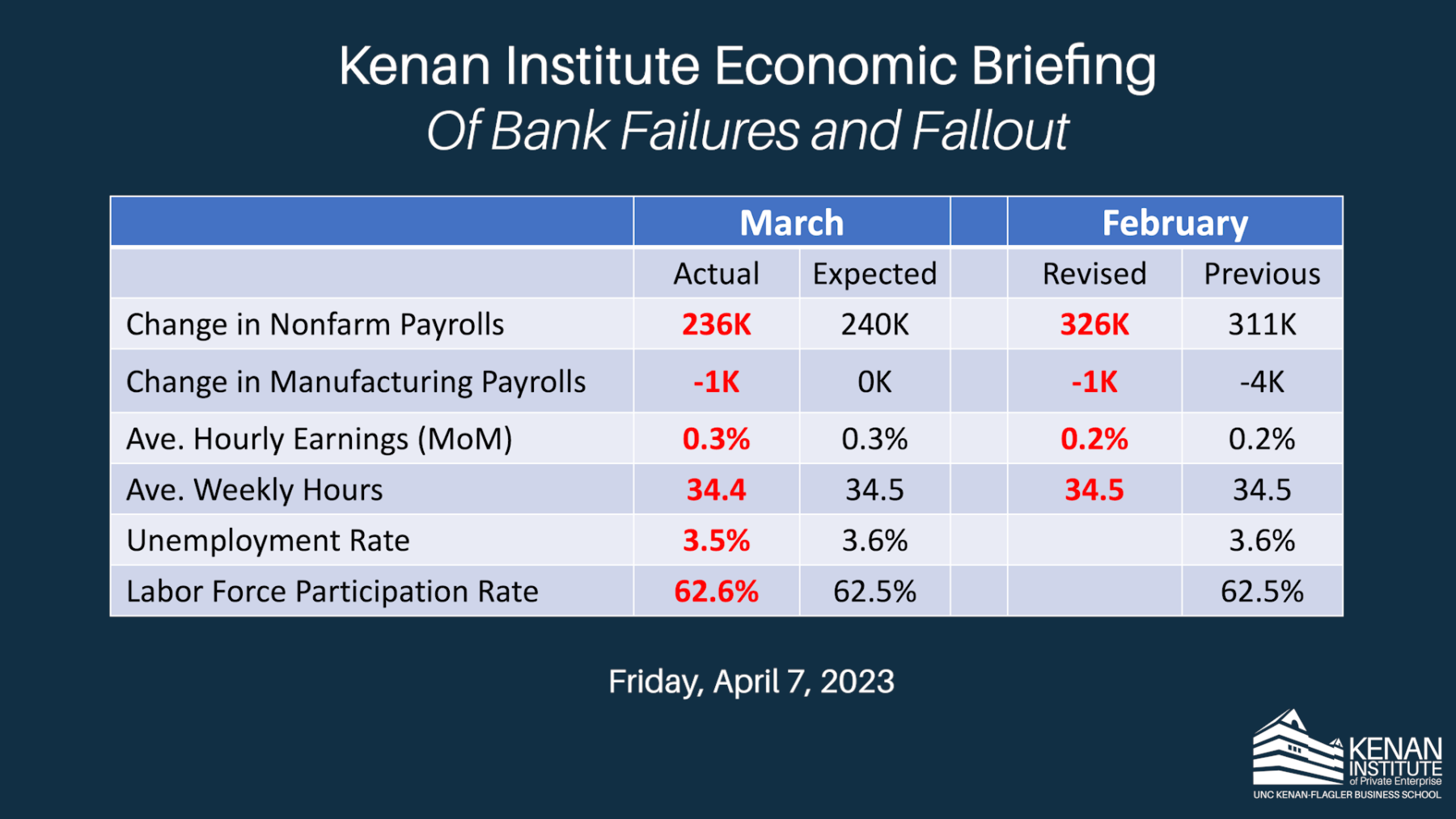

Kenan Institute Executive Director Greg Brown discussed the 311,000 jobs that the economy added in February during the institute’s monthly briefing March 10 and answered questions about labor participation rates and news of trouble at Silicon Valley Bank.

Kenan Institute Chief Economist Gerald Cohen explains why we're doubling down on our recessionary forecasts.

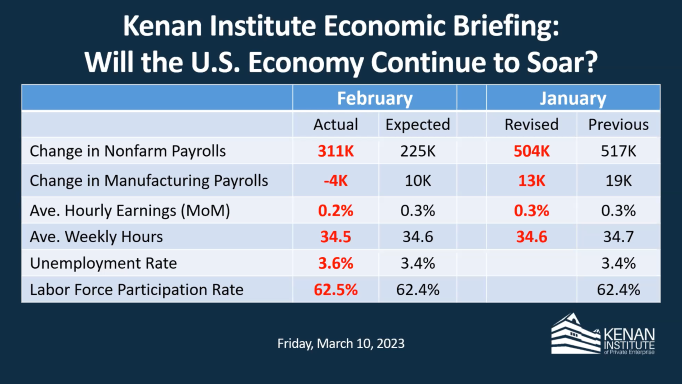

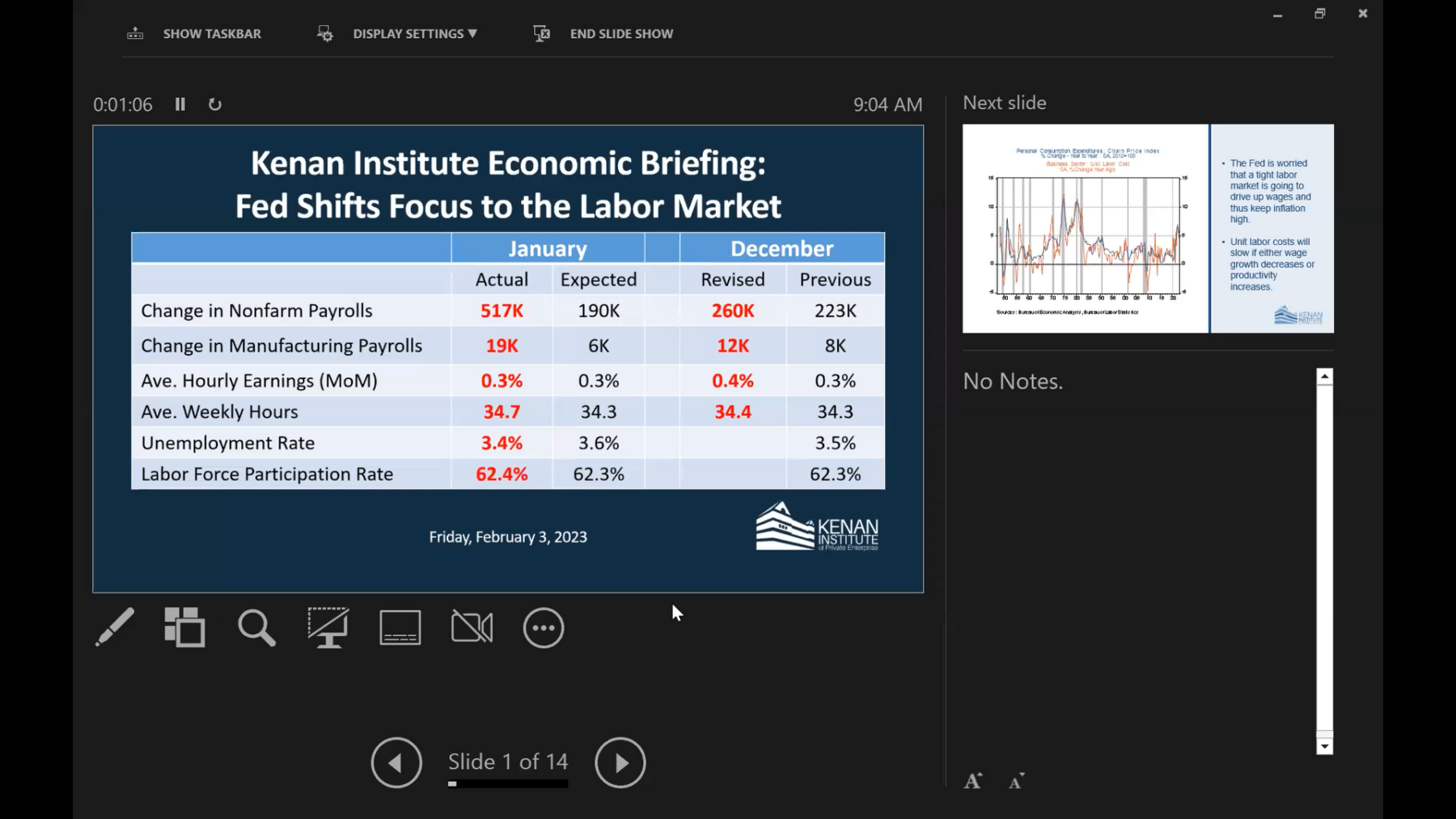

Kenan Institute Chief Economist Gerald Cohen discussed the 517,000 jobs that employers added in January during the institute’s monthly economic briefing Feb. 3 and answered questions from the press on where workers to fill those jobs are coming from.

2022 was a tumultuous year: NASDAQ, a tech-heavy stock index, closed the year down more than 30%; inflation proved more stubborn than policymakers initially thought and reached 40-year highs; Russia invaded Ukraine, sending commodity prices even higher; and central banks cranked up rates in response, the Federal Reserve raising interest rates at an unprecedented pace in recent history from around zero to over 4%. As we entered 2023, the global economy stood “on a razor’s edge,” the World Bank warned in its latest projections. Add to that a divided Congress with razor-thin majorities, political wrangling over the debt ceiling, and increasingly frequent catastrophic weather events, and it leaves one wondering where we are all headed.

Join us for the Kenan Institute’s virtual press briefing at 9 a.m. EST this Friday, Feb. 3, as we provide instant analysis following the latest employment report from the Bureau of Labor Statistics. Institute Chief Economist Gerald Cohen will offer his insights and answer questions from the audience.

In kicking off the new year, we at the Kenan Institute want to highlight five topics we anticipate will be top of mind for business leaders and policymakers during the 12 months ahead.

2022 has not been kind to many investment portfolios; as Kenan Institute Executive Director Greg Brown argues, this is all attributable to the change in real interest and inflation rates.

Chief Economist Gerald Cohen discussed the Bureau of Labor Statistics’ fresh employment report and what it means for the U.S. economy during the Kenan Institute’s monthly economic briefing Dec. 2. Cohen also discussed the inversion of the yield curve.

High levels of inflation have dominated global headlines for a good part of the last year, but what’s the connection between high global inflation and a strong dollar?

How the U.S. is experiencing inflation shows considerable variation from place to place.

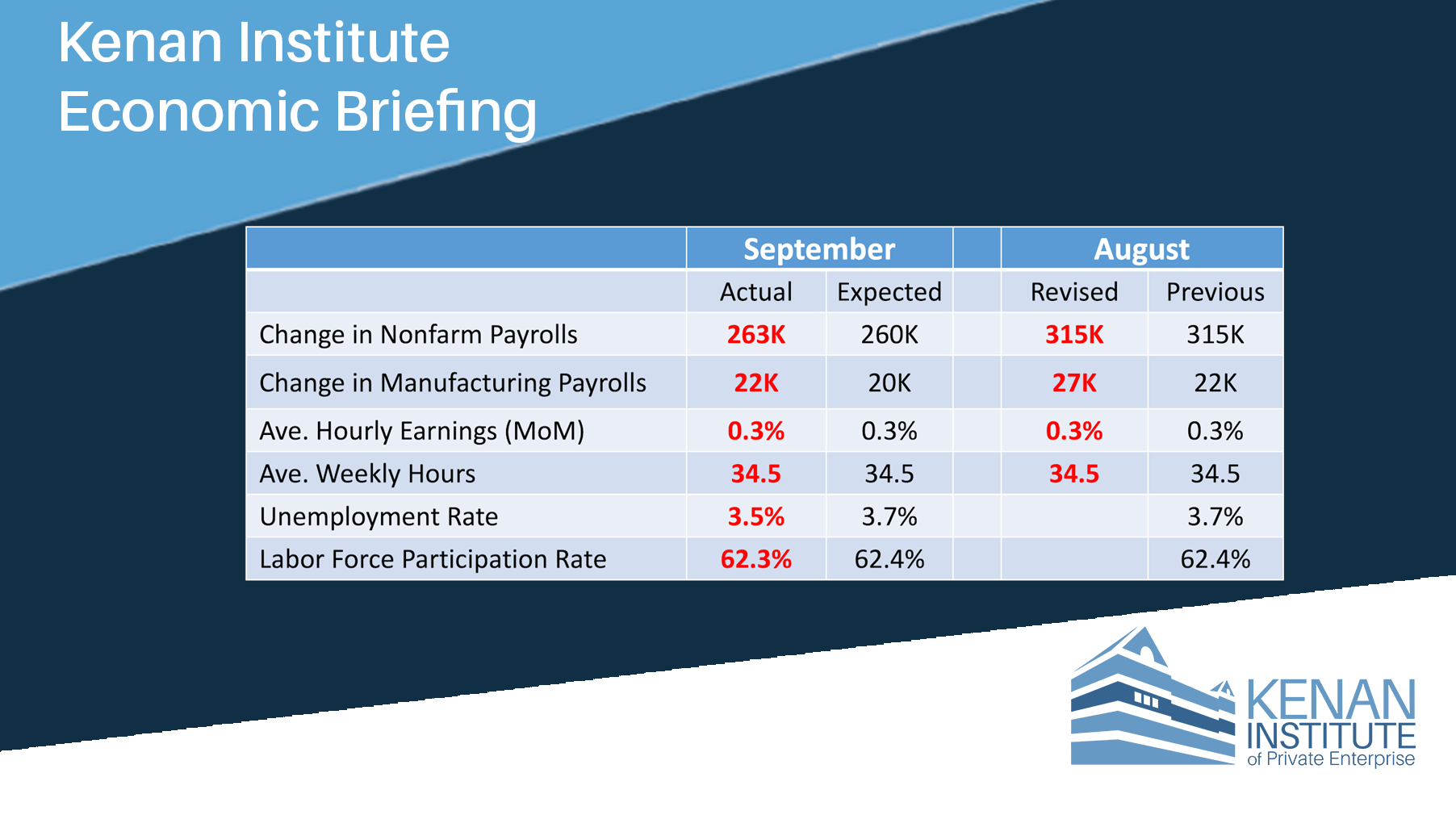

Kenan Institute Chief Economist Gerald Cohen discussed the latest employment report Oct. 7, seeing a few signs of cracks in the economy despite a still respectable number of jobs added during September.

Employment growth has remained exceptionally strong this year, and September is expected to be another healthy month. Join us for the Kenan Institute’s virtual press briefing at 9 a.m. EDT this Friday, Oct. 7, as we discuss the Bureau of Labor Statistics’ fresh employment report and how it may affect the Federal Reserve’s aggressive reaction to inflation.

Economists and investors traditionally see uncertainty as a bad thing that suppresses growth and valuations, but new research shows that downstream uncertainty from customers in the U.S. supply chain can foretell expansion for firms and the economy.

It is probably not a mystery to even the most casual observer of political affairs why the historic climate, health care and tax bill signed earlier this month was dubbed the Inflation Reduction Act. Inflation is high and causing real problems for many households, and so if only Congress could legislate it away by enacting … This is not to say that the package does not deserve any enthusiasm; it is an impressive legislative feat, making significant, though imperfect, advances on health care and climate change. On the other hand, the effect it will have on inflation, its raison d’être in name, will be modest at best and occur only over time.

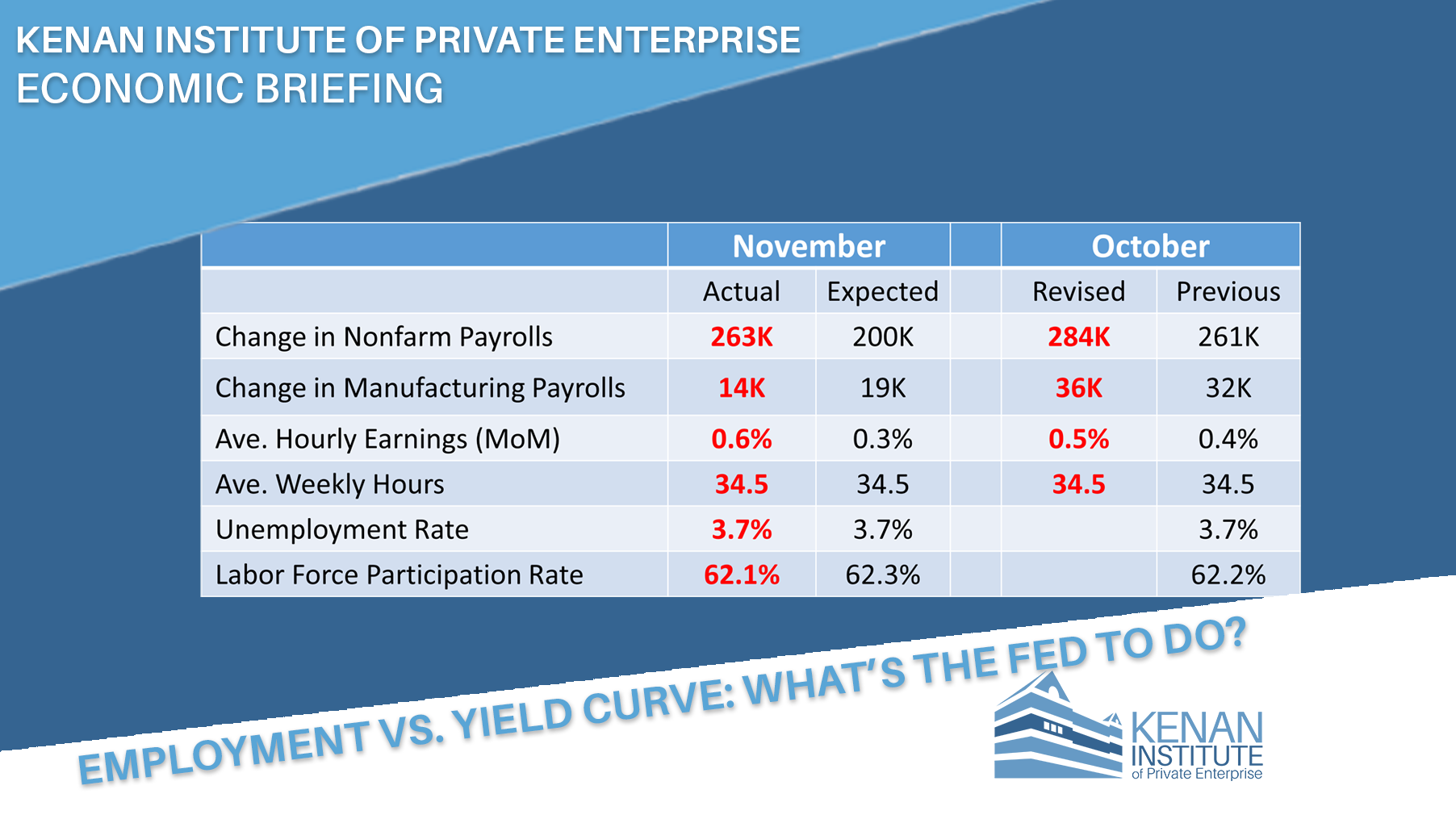

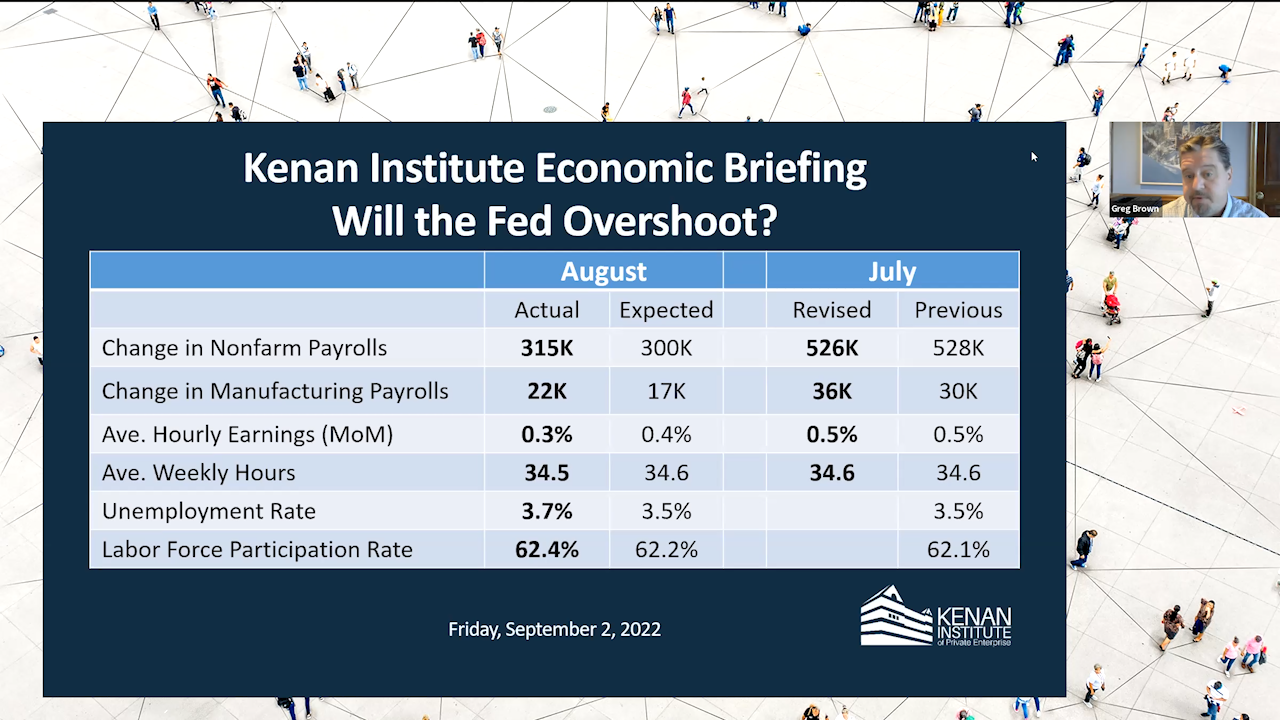

Kenan Institute Executive Director Greg Brown discussed the Federal Reserve’s next move after the Sept. 2 employment report showed slowing but still strong job growth. Brown predicted that the Fed, to protect its reputation as an inflation fighter, would more likely overshoot than come up short in using higher interest rates to tamp down rising prices. He also answered questions from the media on how the global nature of inflation limits the Fed’s effectiveness as well as what can be expected for local and North Carolina labor markets.

Blouin, a member of the Kenan Institute Board of Advisors, told Knowledge at Wharton that proposals to levy a 1% excise tax on corporate share buybacks and a 15% minimum tax on corporations that report more than $1 billion in book profits or in their financial statements were ill-conceived and based on misconceptions of corporate behavior.

The cost to rent a one-bedroom apartment in Raleigh and Durham jumped 6% in a month as the area continues to attract new residents, according to a WRAL TechWire report. Rising prices are an indication of an undersupply in homes for rent or sale, said institute Chief Economist Gerald Cohen, adding that this “suggests that the risks of a significant drop in housing is quite low.”

The Fed is threading a shrinking needle in its attempts to engineer a soft landing for the U.S. economy. Join Professor Greg Brown for a briefing built on the latest employment data and financial market signals, followed by his answers to questions from the audience.

The U.S. economy added 528,000 jobs in July, an unexpectedly strong number that Kenan Institute Chief Economist Gerald Cohen discussed during the Kenan Institute’s economic briefing Aug. 5. Cohen also answered questions from the media about the shifting balance of power between employers and employees, the labor force shortage and what the news means for North Carolina businesses.

GDP, the broadest measure of economic output, contracted for the second straight quarter, stoking fears that the economy is already in a recession — and has been since the beginning of the year. But the guts of the GDP report coupled with continued strong job growth and decent consumer spending suggest that the expansion remains on track. While the official arbiters of recessions are likely to agree with me — they don’t look at GDP but rather measures like job creation — what really matters to households and businesses is whether their spending power or foot traffic is drying up.

Too much or too little? Asked by German network Deutsche Welle about the Federal Reserve’s 0.75 percentage point interest rate increase July 27, Chief Economist Gerald Cohen called it just right, given that a hot job market is now accompanied by high inflation.

Institute Director of Research Paige Ouimet spoke to Ned Barnett for The News & Observer’s Opinion section on how the pandemic has changed workers’ lives. The wages of lower-skilled workers have increased by a higher percentage than those of high-skilled workers, but inflation has effectively wiped out those gains.

A new Raleigh pizzeria is among the area restaurants paying employees higher wages, and the owner told WTVD-TV that bigger paychecks are helping him hire and retain workers. Institute Chief Economist Gerald Cohen said he thinks bar and restaurant workers have long been underpaid and called putting more money in their pockets beneficial to society. “As long as you don't have the inflationary spiral, this could be a really positive outcome. It just means it might cost people more to go to a restaurant,” Cohen said.

Friday morning’s employment report beat expectations, showing that the U.S. economy added 372,000 jobs in June. That runs counter to other economic indicators at a time when high inflation is hurting consumers’ wallets and some see a recession on the horizon.

UNC Kenan-Flagler Business School Professor Camelia Kuhnen is an expert in corporate finance, behavioral finance and neuroeconomics, the application of neuroscience tools and methods to economic research. As many question whether a recession is on the way, she answers some questions about how the most notable consumer confidence surveys differ and whether Americans are prone to economic gloominess.

Institute Chief Economist Gerald Cohen spoke to both WRAL-TV and WTVD-TV on July 5, saying the potential downside of a recent decrease in gasoline prices is that it may reflect concerns in the markets that the economy is going into recession. “Economic activity slows, gasoline demand slows,” Cohen said. “If [prices are] coming down because people think we’re in a recession, then that’s bad.”

Kenan Institute Chief Economist Gerald Cohen was part of a panel on WRAL’s in-depth news program July 2 discussing the whys and how longs of inflation, particularly rising prices for gas, housing and food.

Chief Economist Gerald Cohen will appear on a panel on WRAL-TV’s “On the Record,” on Saturday, July 2. They’ll discuss how a sharp increase in the inflation rate over the last few months is affecting Americans and when they may begin to feel some relief. The program is scheduled to air at 7 p.m.

The Fed tried to show its inflation-fighting mettle by raising the federal funds rate, the short-term interest rate it directly controls, by 0.75 of a percentage point. This is the largest increase since 1994, though the funds rate remains at a quite low 1.625%, especially relative to the 8.6% inflation reading last week. The Fed seemed to be spooked by the inflation print — which, rather than declining as many forecasters (including myself) expected, rose to its highest level since 1981. More important, in my opinion, longer-term measures of consumer inflation expectations and uncertainty increased.

Higher prices for gas, groceries and nearly everything else are on consumers’ minds after a government report Friday showing that inflation is up 8.6% on a year-over-year basis, the largest jump since late 1981. Chief Economist Gerald Cohen tells WTVD-TV, “When people start saying, ‘I think inflation is going to continue to occur, that means that the Fed has to work harder and that it could end badly.”

After government statistics showed another big annualized jump in inflation Friday, talk turned to how aggressively the Federal Reserve will act in raising interest rates this week. “Many people are expecting a half a percentage point increase,” Chief Economist Gerald Cohen told WRAL-TV. “Perhaps this would raise the discussion of doing a three-quarters of a percent increase.”

First, the good news. Given what we know about current economic conditions, it is likely that the consumer inflation rate has peaked in the U.S. for the current cycle. Recent inflation reports on the Consumer Price Index (CPI) and Personal Consumption Expenditures (PCE) Implicit Price Deflator, which is the Federal Reserve’s preferred measure, show a jump to new 40-year highs in March but signs of moderation in coming months. For example, consumer goods with very large 12-month cost runups such as used cars and food away from home are starting to see prices moderate. Likewise, prices of important household goods like apparel, furnishings, prescription drugs and recreation commodities (think TVs and Pelotons) are flattening. Furthermore, some important energy prices such as crude oil and gasoline have stabilized in April after jumps in the first quarter. So, while inflation will surely remain elevated for some time, it is unlikely to get much worse.

Concerns about further supply-chain troubles are on the rise. Just a few months ago the “temporary disruptions” stemming from covid were predicted to work themselves out in 2022. However, businesses are now faced with the possibility of disruptions much more severe than those experienced to date. These stem from two sources: interrupted supplies in essential raw materials and agricultural commodities resulting from Russia’s invasion of Ukraine and the potential for a rapid (and massive) spread of COVIC-19 in China resulting in suspensions to manufacturing operations there.

Inflation hit a 40-year high of 7.8% in February. We estimate energy prices will raise inflation by another percentage point in March. If sustained, the runup in gas prices will take a $100 billion-sized bite out of households’ wallets, weighing on consumer spending – and ultimately, inflation.

Together with many business and economic leaders around the globe, we at the Kenan Institute of Private Enterprise support the harshest feasible sanctions against Vladimir Putin in the immediate interest of Ukraine and its people. More broadly, we view such measures as vital to the long-term survival of democratic values. But as the Russian invasion continues, seemingly unabated by unprecedented economic and financial sanctions, we must ask: what more is feasible? And for how long can such restrictions be sustained?

The jumps in the inflation rate over the last few months have been larger and longer-lasting than expected. For much of 2022 economic forecasters, including those at the Federal Reserve, assumed that higher inflation rates would be short-lived—or “transitory” using the preferred jargon of the day. Inflation was expected to start shifting back towards the Fed’s 2% target as supply-chain bottlenecks were resolved and a pandemic-induced shift in demand for consumer goods swung back toward consumer services. Instead, recent inflation prints have set 40-year records and we are seeing more discussion about the possibility of a “wage-price” spiral.

Following last week’s debate about the overheating economy, Kenan Institute experts return this week for round two – this time focusing on policy. In this week's insight, Kenan Institute’s Executive Director Greg Brown and Chief Economist Gerald Cohen debate the pandemic’s influence on U.S. fiscal policies.

Inflation hit its highest level in almost forty-years, with overall prices up 7% in 2021. Is this a transitory increase as a result of COVID-driven demand and supply shortages, with inflation likely to decelerate to around 2% over the next year? Or, is inflation the result of a meaningfully overheated economy and likely to remain meaningfully higher than the Fed’s 2% target precipitating changes in business behavior and an aggressive policy response?

As the U.S. continues to face COVID-19 and supply chain disruptions, experts debate just how worked up the economy is in its current state. This week’s Insight serves as the first in a two-part point-counterpoint series, in which Kenan Institute Executive Director Greg Brown and Chief Economist Gerald Cohen hash out the arguments both for and against an overheating economy.