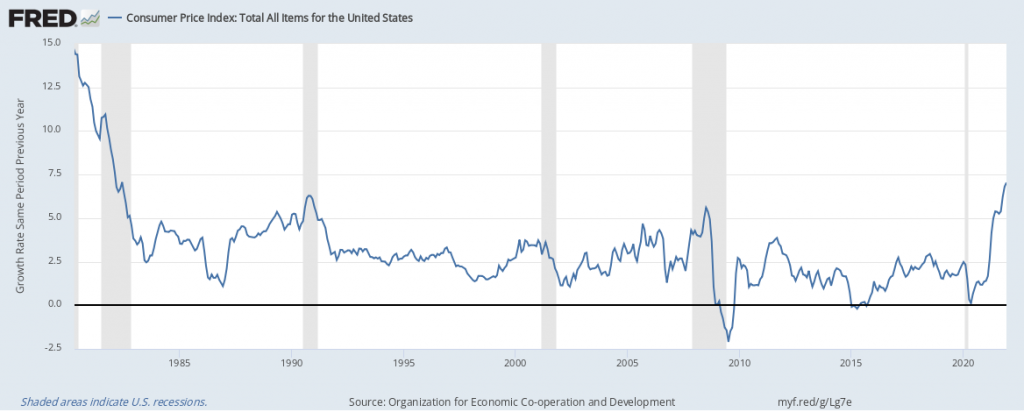

Inflation hit its highest level in almost forty-years, with overall prices up 7% in 2021. Is this a transitory increase as a result of COVID-driven demand and supply shortages, with inflation likely to decelerate to around 2% over the next year? Or, is inflation the result of a meaningfully overheated economy and likely to remain meaningfully higher than the Fed’s 2% target precipitating changes in business behavior and an aggressive policy response?

Figure 1: Highest Inflation in 40 Years

Greg Brown, Kenan Institute’s Executive Director: I believe the U.S. economy is boiling over! I estimate that the GDP-gap, the difference between the actual level of GDP and its potential is +5.9%, which means that the economy has never been more overheated. As a result high levels of inflation will remain with us until the economy slows down meaningfully.

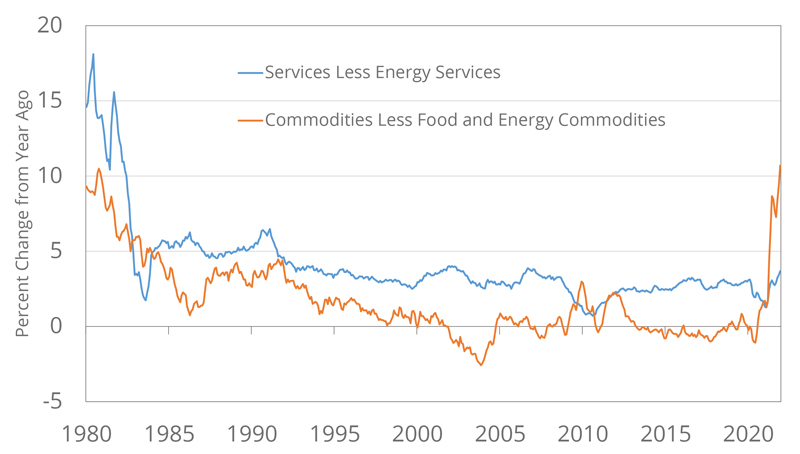

Gerald Cohen, Kenan Institute’s Chief Economist: I believe that most of the inflation reflects a combination of a COVID-driven shift in demand toward goods and housing and supply shortages. Families stopped going to restaurants and started remodeling their kitchens. Meanwhile, appliance makers had their factories shut down and then when they restarted, they ran at a lower capacity because of pandemic precautions. As a result, inflation for goods like dishwashers and cars was up 10.7% in 2021, the fastest pace in decades (Figure 2). However, manufacturers are responding to these price signals – though Omicron has thrown some sand in those gears – but as supply shortages abate, goods inflation should follow suit.

Figure 2: Goods vs. Services Inflation

Source: FRED

Some of these supply-demand imbalances have bled into the services sector. For example, rental car prices came from a combination of rental car companies selling off their fleets to remain afloat during the spring 2020, then facing an inability to rebuild fleets because of the chip shortages. But overall, service price inflation has remained relatively muted, with recent acceleration more about a return to trend after below trend growth.

I also believe that when COVID-19 subsides, there will be a shift in demand back to services. As more people dine out and take more extensive vacations they may regret some of their goods purchases. I wouldn’t be surprised to see cancelled backlogged orders of furniture and appliances, and lightly used boats or exurbs homes on the market at cut rate prices. This would lead to a return to the goods deflation we experienced for much of the last 20 years.

Greg: I don’t feel as complacent about services inflation given the most recent data. Inflation in the service sector experienced a dramatic spike toward the end of 2021. The inflation in services is widespread as well: housing, healthcare and personal services (i.e haircuts) inflation all clocked in at an annual rate of more than 4% in the fourth quarter. Thus it seems very clear to me that we are in a position of too many dollars chasing too few goods – another way of defining overheating.

As a result, we are starting to see signs of a wage-price spiral, where workers who are already in short supply are demanding wage increases to keep up with inflation. This would inflation even higher, creating a vicious cycle. Without an immediate an immediate increase in the Federal Funds rate to at least 5%, inflation will not abate!

To learn more, see Is the U.S. Economy at a Boiling Point, or Just Simmering?

- Keyword(s):

- covid-19 192

- inflation 62

- monetary policy 17

Is Inflation Transitory or Long-Lived?