UNC Kenan-Flagler Business School Professor Camelia Kuhnen is an expert in corporate finance, behavioral finance and neuroeconomics, the application of neuroscience tools and methods to economic research. As many question whether a recession is on the way, she answers some questions about how the most notable consumer confidence surveys differ and whether Americans are prone to economic gloominess.

Can you tell us about your field of study in neuroeconomics and behavioral finance? From your research, how does consumer sentiment impact the economy?

Camelia Kuhnen: Consumer sentiment has a significant impact on future economic growth. Consumer spending represents about 70% of gross domestic product in the U.S., and therefore if people are pessimistic in their expectations about availability of jobs in the future or their wages or inflation, this will change their spending. This is why the Fed is working very hard now to make sure households’ expectations about inflation do not become too high — if that were to happen, we’d be dealing with a self-fulfilling prophecy: If consumers expect very high inflation in the future, they’d want to buy things today and will ask for higher wages, which will then cause inflation to be high.

But is consumer sentiment warranted to be as pessimistic as it is sometimes? Research in neuroeconomics and behavioral finance has shown that this is not the case.1 We have found that people become unduly pessimistic about future economic conditions when they have been in an environment where there has been some bad economic news. In this type of environment, even the slightest bit more bad news leads people to overreact in their assessment of just how bad the economy will do in the future.

In the current context, my assessment is that households are overreacting to news about inflation — and are too pessimistic about how the economy will look in the future.

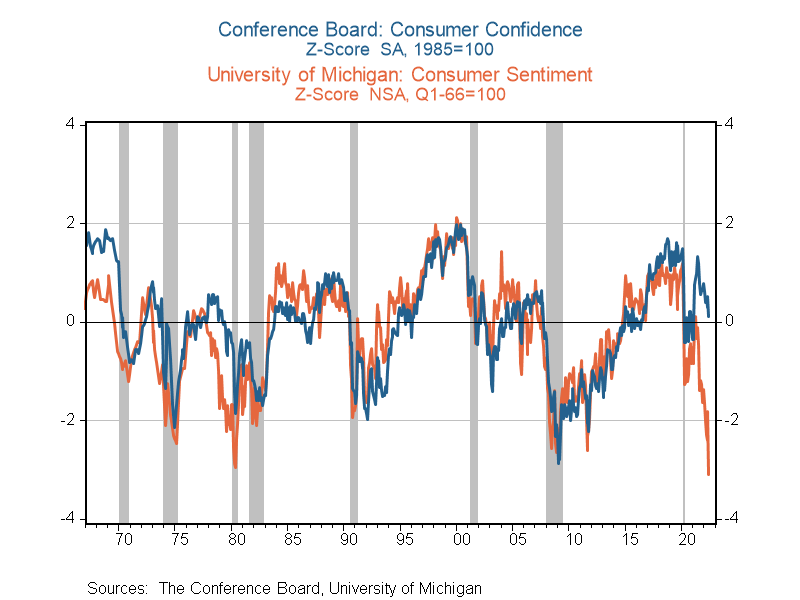

The two main measures of consumer sentiment seem to be giving mixed signals, with the University of Michigan measure at record low levels while The Conference Board is down but still slightly above historical averages. What is your take on these differing measures, and what will you be watching for in the coming months?

Camelia Kuhnen: Both of these consumer sentiment indexes are based on two types of questions: about people’s present situation and about people’s expectations about the future.

The expectations piece is different across the two surveys: Michigan asks people to think about economic conditions 12 months ahead, whereas The Conference Board asks people to think about economic conditions six months ahead. The Conference Board’s expectations part of the index appears to be more optimistic than Michigan’s expectations part of the index, and this can reflect the different horizon that people in the two surveys think about when answering questions about future economic conditions. A simple explanation that makes the surveys agree with each other is that people assess the economy to be in pretty good shape in six months but not in such good shape in 12 months. Why? Maybe because they think that stimulus money will run out in 12 months or that inflation will be even more out of control in 12 months but not in six months.

Now, if you look at the piece of the two indexes that captures people’s assessment of “present conditions,” this is where we see a discrepancy between Michigan and Conference Board that seems very large. Conference Board respondents assess present conditions to be much better than Michigan respondents. But this also could have a simple explanation: The questions about present conditions in the two surveys are different. Michigan survey respondents are asked “Is this a good or bad time to buy major household items?” and “Would you say your family is better or worse off financially than you were a year ago?” whereas Conference Board respondents are asked “How would you rate general business conditions in your area?” and “What would you say about available jobs in your area right now?”

It is then perfectly understandable why the Michigan folks have answers that seem more negative about “present conditions” than those of the Conference Board folks: The people in the Michigan survey have to answer a question that brings to mind high prices or inflation, whereas the Conference Board respondents have to answer a question that brings to mind how low unemployment is. So both types of respondents can be accurately assessing the present situation: Those asked to think about “Is this a good time to buy stuff?” will tell you no, because they have seen prices go up tremendously for certain things (e.g., cars, houses) in the recent past. And those asked to think about “Are there jobs available in your area?” will say yes, because they see businesses working really hard to hire people in this environment with very low unemployment.

To summarize: The two consumer sentiment indexes do not have to be in conflict with each other. This is because they differ in terms of which aspects of the economy they have respondents think about, and they differ in the time horizon that the respondents are asked to consider when reporting what they expect economic conditions to look like in the future.

Both measures, as well as the sentiment in the press, seem to have shifted quickly despite very low unemployment rates. What is driving this change in sentiment, and do you think it’s an accurate reflection of where the economy might be headed?

Camelia Kuhnen: I think that people are responding to the intense news coverage of inflation numbers and to global developments, including the war in Ukraine. It makes sense to become a bit worried about the future. That being said, as I mentioned earlier, people tend to overreact to bad news in an economic environment where they have heard some bad news already. We see that consumer spending is slowing down, and this should help reduce inflationary pressure. The real estate market seems to also be moving from a frenzied seller’s market to one where more than 40% of listing prices are being reduced, and more homes are available for sale than what we typically saw over the prior two years. That will also help cool off prices. The Fed has also indicated that it will raise rates as much as needed to bring down inflation to a rate that is sustainable. Overall, I am optimistic that we won’t see a recession in the next year and that inflation will go to around 3% in the next 12-18 months.

Is there anything you can say about business sentiment, which is also giving mixed signals?

Camelia Kuhnen: Different sectors of the economy will experience different growth rates over the next year or so. Services (e.g., travel) are experiencing a really busy summer, whereas construction has slowed down. So, the news about business sentiment can be mixed because different business sectors are exposed differently to inflationary pressures, or to consumer spending changes, or have different exposure to macroeconomic conditions. Some businesses are procyclical, others are countercyclical and others do fine no matter what.

1 Kuhnen, C. M. (2015). Asymmetric learning from financial information. The Journal of Finance, 70(5), 2029–2062. https://doi.org/10.1111/jofi.12223