How tech monopolies and the finance sector are exacerbating income inequality across America

The geographic distribution of wealth in the U.S. today is much different than it was just a few decades ago. In 1980, many of the most well-paid workers lived in places dominated by manufacturing. Now, wealth in many of those places has fallen while incomes have skyrocketed in places that are home to major technology firms. In a Kenan Institute of Private Enterprise research paper, Maryann P. Feldman from the University of North Carolina, Chapel Hill; Frederick Guy from the University of London; and Simona Iammarino from the London School of Economics and Political Science examine how the rising economic power of technology and finance firms has contributed to regional income disparities across America.

The researchers detail three trends driving income disparities. The first is that many top technology companies exhibit a winner-take-all dynamic that creates monopoly power, which in turn makes certain locations invincible by amplifying the benefits companies gain by clustering together geographically. Second, these monopolies inhibit local economic development in other places by imposing what can be considered a “tax” on economic activity while also restricting dissemination and customization of technology. Third, the authors argue that the financial sector feeds this dynamic by favoring geographically concentrated big-tech monopolies at the expense of other places and industries.

The trends outlined in the paper reveal that many of today’s economic policies aren’t helping places that lack the headquarters of big-tech monopolies. The authors posit that breaking up the concentrated economic power of the technology and finance sectors would be the best way to encourage more evenly distributed economic activity and prosperity.

The rise of monopolies

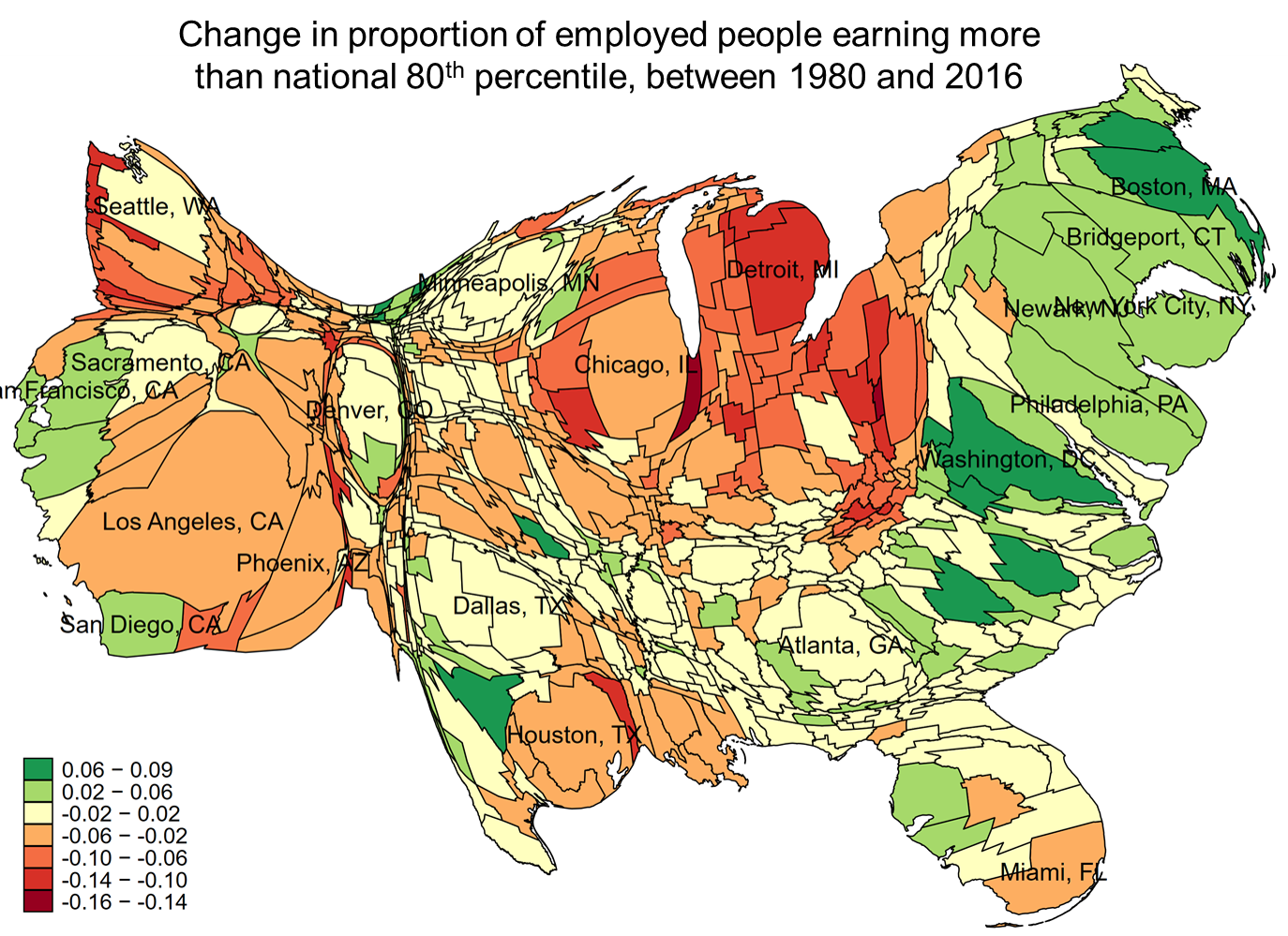

In 1980, the highest concentration of well-paid workers was in Gary, Indiana, followed by Detroit, and Washington, D.C. In 2016, Washington, D.C., held the top spot followed by San Francisco-San Jose, New York, and Boston. From 1980 to 2016, those three metropolitan areas, along with secondary hubs in banking and technology, saw the largest increases in the share of workers earning incomes exceeding the 80th percentile nationally. At the same time, income in most of the industrial heartland declined, including yesterday’s technological leaders like Detroit, home of the automobile industry and Rochester, N.Y., home of Kodak and Xerox.

In some places, better paying jobs might have arisen from industry expansion or the shift toward skill-based labor. However, an outsized proportion of high-paying jobs are concentrated in places where firms have achieved monopoly status, defined as increased market power and the ability to command prices that far exceed the cost of providing a service or good. Consider, for example, Apple, Google, and Facebook in Silicon Valley; Microsoft and Amazon in Seattle; and Qualcomm in San Diego.

The authors attribute the increasing prevalence of monopolies to three factors: the platform nature of digital technology, extended intellectual property (IP) rights, and a loss of regulatory oversight.

- The platform nature of digital technology: Digital technologies benefit from network economies – situations in which a growing number of users increases the product’s value to the consumer and/or decreases the costs to the producer (Evans 2003; Gawer 2010; Rochet and Tirole 2006). Digital platforms, in particular, exemplify a type of network economy that leads to monopolies when platforms lock down and monetize a segment of a previously open digital network. One example is messaging protocols that keep messages within a specific social media platform rather than using universal e-mail or texting protocols.

- Extended IP rights: Like digital platforms, firms based on IP rights such as patented software, algorithms, genetic codes, and business models have grown both in terms of their market power, and in terms of their geographic concentration. For these firms, clustering near other IP-based firms helps lower marginal costs and facilitate the global reach of the monopoly.

- Loss of regulatory oversight: The growth of monopoly power occurred under the reinterpretation of anti-trust law pioneered by Robert Bork in 1967. Previously, monopoly power was assessed based on trade restraint; Bork’s interpretation required evidence of harm to consumers. As the Bork interpretation gained popularity in the 1990s, the number of antitrust cases pursued by the Federal Trade Commission dried up, allowing more monopolies to grow unchecked.

Although today’s monopolies come with some of the same issues as those previously encountered with monopolies over electric power distribution and telecommunications, they typically project market power over a much wider, often global, territory. In addition, because they are valuable industries to their home bases, government has limited motivation to regulate them (Iammarino 2018).

Concentrated benefits, widespread costs

Companies tend to cluster near other companies that are in related industries. By doing so, they benefit from proximity to a pool of skilled labor, knowledge spillovers, and access to specialized suppliers and customers. In many cases these clusters also benefit from the presence of local institutions and universities, government R&D spending, formal mechanisms for inter-firm cooperation, and social networks that facilitate trust and knowledge-sharing while reducing transaction costs.

While this clustering tendency has been observed for more than a century, monopolies can amplify the effect. In the winner-takes-all world of digital platform monopolies, the value of technical staff who are even slightly better, or technical and market intelligence that is even slightly more complete or up to date, might make the difference between market dominance and irrelevance (Rosen 1981; Sattinger 1979). As a result, such firms derive a great deal of value from proximity to skilled labor and knowledge spillovers.

The geographic concentration of tech monopolies has not necessarily been positive, even for the areas that are home to these clusters, which have experienced rocketing real estate costs, rising homelessness, and transportation problems. The effects on other places have been not only passively negative, but actively so, in that places lacking tech monopolies have been not just left behind but held back. Today’s technology monopolies collect revenues that are effectively a tax on almost all business activities in most parts of the world. For example, Microsoft produces software in the Seattle area but harvests license fees globally. Amazon controls a chokepoint through which it can tax the revenues of thousands of vendors and gather vast amounts of data on consumer purchases. Intermediaries like Airbnb, Trip Advisor, Booking.com, Expedia (Microsoft), and Uber all take significant slices of revenue from many thousands of globally dispersed small businesses. This situation redistributes wealth from around the world to the shareholders and employees of the platform companies found in a few privileged places.

Digital platform monopolies make their money by controlling access to previously open networks. This affects not only consumers of digital services, but also potential producers of such services. As companies such as Microsoft, Adobe, Apple, and Oracle have worked to prevent the spread of open source software, they have limited organizations’ ability to adapt software to meet their own needs. This has curtailed locally based skilled work as well as software products and capabilities that could be sold to others.

Finance further feeds monopolies

The financial sector plays an important role in the geography of wealth because it facilitates the movement of capital away from firms with lower returns, which tend to operate in more competitive markets, to firms with monopoly power or monopoly prospects. In effect, this means finance flows to places with monopolies at the expense of those without.

This situation has resulted from a shift in which companies have become significantly more dependent on financing. From the 1970s until the year 2000, the typical medium or large American firm was largely self-financing, paying some of its cash flow out to shareholders and using a greater portion for capital expenditure. Since 2000, many firms have paid substantially more of their cash to shareholders or to acquire other firms, with average payouts approximately equaling capital expenditure and companies relying more heavily on financing as a result.

In a competitive market, increased dependence on financing can indicate increased efficiency of financial markets because capital is moved from less productive to more productive uses (Rajan and Zingales 1998). However, the same does not hold true in a market with monopoly power. If higher returns are gained by investing in monopolies, commercial banks are incentivized to strip assets from perfectly viable firms to finance monopolies. When monopolies are found in clusters, this dynamic increases the inflow of capital to monopoly firms and the places in which they invest (Myrdal 1957), inhibiting opportunities for growth or economic revival elsewhere. This dynamic is further intensified by the growing industrial and geographical concentration of commercial banking.

Breaking up economic power

The stark divide in economic realities between places that are doing well and those that are not reflects the rise of monopolies and the power of the financial sector. Local economic development policies have not been successful for most of the population because these policies tend to focus on generating increasing returns to a place, finding the right industrial niche or smart specialization, and attracting established companies or enabling entrepreneurs. These strategies don’t work because monopoly conditions limit the ability for new businesses to emerge, and the few firms that do succeed are pressured to relocate to the centers of monopoly power. This creates star cities with which other localities can’t compete.

If the U.S. is to address its worsening regional income disparities, reversing the rise of monopoly power will be critical. Local economic development initiatives in held-back regions are bound to be ineffective against the unrestricted power of regions that are home to tech monopoly clusters. From both national and international perspectives, reducing monopoly power is tricky because these tech monopolies have become a key element of the U.S. international competitiveness. Also, the monopolies themselves are politically powerful and their symbiotic relationship with the financial sector gives Wall Street and the monopolies a common interest in the status quo. However, with further research and informed policy steps, regulation of monopoly power and the financial system may offer the best path to economic revival in America’s held-back cities and regions.

References:

Evans, D. 2003. “Some Empirical Aspects of Multi-Sided Platform Industries.” Review of Network Economics 2: 3. https://doi.org/10.2202/1446-9022.1026.

Gawer, A. 2010. “The Organization of Technological Platforms.” Research in the Sociology of Organizations 29: 287–96.

Fama, Eugene F. 1980. “Agency Problems and the Theory of the Firm.” Journal of Political Economy 88 (2): 288–307.

Iammarino, Simona, Philip McCann, and Raquel Ortega Argilés. 2018. “International Business, Cities and Competiveness: Recent Trends and Future Challenges.” Competitiveness Review 28 (3): 236–51. https://doi.org/10.1108/CR-10-2017-0070.

Jensen, Michael C., and William H. Meckling. 1976. “Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure.” Journal of Financial Economics 3 (October): 305–60.

Manne, Henry. 1965. “Mergers and the Market for Corporate Control.” Journal of Political Economy 73: 110–20.

Rajan, Raghuran G., and Luigi Zingales. 1998. “Financial Dependence and Growth.” American Economic Review 88 (3): 559–86.

Rochet, J., and J. Tirole. 2006. “Two-Sided Markets: A Progress Report.” The RAND Journal of Economics 37: 645–67. https://doi.org/10.1111/j.1756-2171.2006.tb00036.x.

Rosen, Sherwin. 1981. “The Economics of Superstars.” American Economic Review 71: 845–58.

Sattinger, Michael. 1979. “Differential Rents and the Distribution of Earnings.” Oxford Economic Papers 31 (1): 60–71.