- Inflation hit a 40-year high of 7.8% in February.

- We estimate energy prices will raise inflation by another percentage point in March.

- If sustained, the runup in gas prices will take a $100 billion-sized bite out of households’ wallets, weighing on consumer spending – and ultimately, inflation.

I have been fairly sanguine on the medium-term outlook for inflation – believing that most of the spike in inflation reflects the combination of an unprecedented shift in goods demand running into supply constraints exacerbated by COVID-19 related labor shortages. As the pandemic abates, I anticipated we would see a deceleration in inflation as demand shifts toward services and supply constraints loosens. Even though inflation hit a 40-year high of 7.8% in February, there were some promising signs as used vehicle prices were down and new car prices showed more modest gains for the second consecutive month. Unfortunately, in the near term, inflation is going to move meaningfully higher on the back of energy prices.

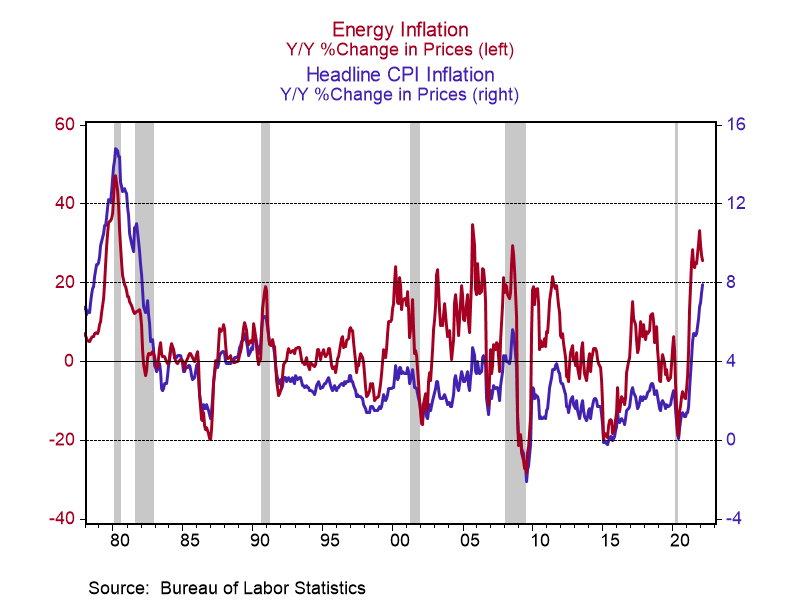

While energy represents only 7.5% of an average household’s spending, as the chart below illustrates, the large swings of energy prices make for a key driver of inflation. AAA reports that national gasoline prices are currently $4.33, up from $3.48 from a month ago. This is likely to raise inflation by about one percentage point in March, with the potential for even larger gains given the impact of oil prices on airfares and shipping costs. The surge in other commodity prices, such as food and industrial metals, will also weigh on inflation but to a much lesser extent, as they represent a much smaller share of the final cost of consumer goods. (Recall the adage that what’s inside a box of cereal costs less than its packaging and advertising.)

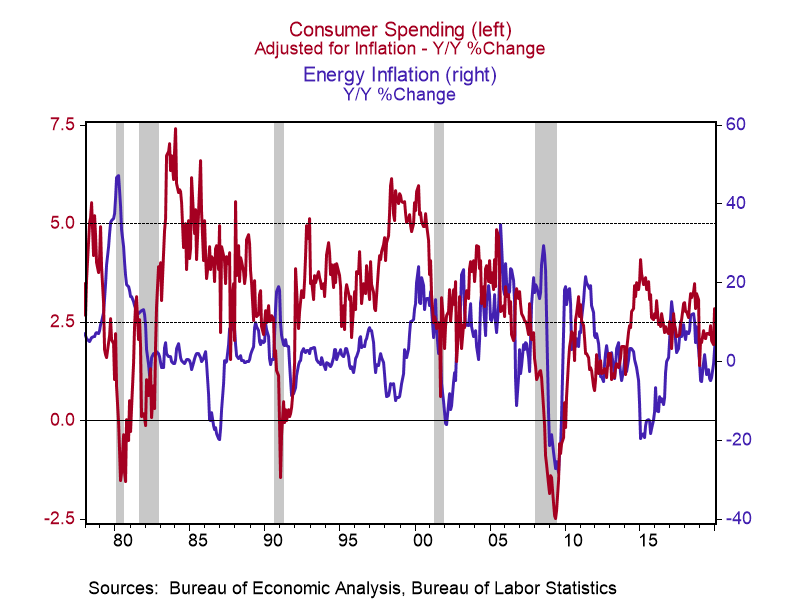

Unfortunately, a runup in energy prices often precedes recessions – the gray bars in the chart below – though the relationship is much more complicated than can be illustrated in a simple picture.1 What we can say is that higher gasoline prices clearly weigh on consumer spending. We estimate that if gasoline prices stay where they are, they will take a $100 billion-sized bite out of households’ wallets over the course of a year, which could cut consumer spending by about one-half percentage point. While we don’t think this is enough to put the U.S. economy into recession, especially since the U.S. has a large energy sector that benefits from higher energy prices, the slowdown in demand is likely to soften overall inflation pressures in the future.

That is why the Fed is unlikely to tighten more aggressively than expected a month ago – in fact, most observers anticipate the Fed will begin raising rates next week followed by a modest path of rate increases over the next year. However, it does make the Fed’s communication challenges even harder. The Fed keeps saying that inflation is expected to slow over the coming months – but that forecast keeps getting pushed out. Another challenge for policymakers is that higher energy prices hit lower income households hardest as gasoline represents a larger share of their spending basket. These households are also more likely to have jobs that require commuting. While proposals to soften the blow by cutting gas taxes may seem like a good idea, they aren’t targeted enough to the households that need the most support (and they work against long-term climate goals). Instead, expanding the Earned Income Tax Credit, which is targeted to lower income working households, would produce the greatest benefit at the lowest cost.2

This commentary was written by Kenan Institute Chief Economist Gerald Cohen.

1 https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2745171

2 For a more in depth discussion of the tradeoff see https://archive.massbudget.org/report_window.php?loc=The%20Pros%20and%20Cons%20of%20Higher%20Gas%20Taxes,%20and%20How%20They%20Could%20be%20Offset%20for%20Lower-Income%20Families%20-%20MassBudget.html