Event • Aug 25, 2022

Although innovation is the engine of a growing economy, it is highly concentrated in a relatively small number of high-growth companies. As policymakers and investors have more closely examined the role of these companies in the economy, one sore spot has been the shortcomings related to social impact, or what is often referred to as the “S” in ESG. One issue that has received particular attention is workforce diversity.

While high-growth startups are especially important because of their large impact on the overall economy, it is also important to consider them through a diversity lens. For example, startups create substantial wealth for founders and investors. In fact, seven of the 10 richest people on the Forbes World’s Billionaires List are associated with high-growth technology companies.1 None of these top high-growth tech billionaires are women or underrepresented minorities. Lack of diversity in a wealth-building space like private equity has implications for broader societal outcomes such as the racial wealth gap. Research has estimated that white families have six times more wealth compared with Black families, on average, a dramatic gap that is at least partly fueled by differences in capital gains.2

The success and composition of innovative startups often depend on the venture capital firms, which select the startups that receive funding early on and monitor the startups after their funding. However, as we show in recent research by Cassel, Lerner and Yimfor (2022) and Cook, Marx and Yimfor (2022), less than 3 percent of venture capital firms or portfolio companies receiving venture funding are owned by minorities.

This lack of diversity can have important consequences regarding how capital is allocated, the quality of products that are created, the diversity of employees who are hired and, ultimately, startup performance. Diverse teams might not only create success by allocating capital to traditionally overlooked entrepreneurs (our research shows that diverse venture firms fund three to four times more diverse entrepreneurs), but diverse teams of entrepreneurs may also create better products for their customers and provide better services to their customers. A diverse workforce will likely create solutions that are inclusive and mirror the demographics of the population they serve. Thus, a lack of diversity can leave everyone worse off and contribute to some of the inequality we observe.

In this Kenan Insight, we unpack statistics on diversity in high-growth startups and the private capital groups that fund them, sources of funding disparities, and implications of the lack of diversity, as well as provide some suggestions to help facilitate change over time.

The first step in understanding the lack of diversity among high-growth companies and venture firms is having clear statistics on ownership of private capital groups and portfolio companies by race. This is difficult, however, because databases that track private markets activity do not systematically classify founders or partners at venture funds by race. We take on these tasks in two recent papers, classifying about 60,000 founders receiving venture funding and 36,000 managing partners and founders of venture firms active between 2000 to 2020 by race using their images we collected from various internet sources. Our research shows that about 2.6% of private capital groups have owners who are Black or Hispanic and less than 2 percent of founders receiving venture funding are Black.3 This composition of founding teams at high-growth startups and private capital groups stands in stark contrast to the working age population in the United States, which is 62% white, 6% Asian, 18% Hispanic and 12% Black, according to the U.S. Bureau of Labor Statistics.4

Using this data, we show that Black and Hispanic entrepreneurs encounter difficulties in raising first-time funds, that they are less likely to raise follow-on funds after periods of low returns, and that, in the five years following company formation, Black founders raise close to $6 million less in venture funding than non-Black founders of companies formed in the same year, located in the same state and operating in the same industry. This funding deficit exists even though Black high-growth startups are just as likely to exit (go public or be acquired), just as likely to fail and just as likely to obtain patent approval conditional on applying as non-Black startups. Our results on the performance of diverse-owned startups are consistent with other studies showing that companies with diverse executive teams had 19% more revenue and were 43% more likely to experience higher profits relative to their nondiverse peers.5

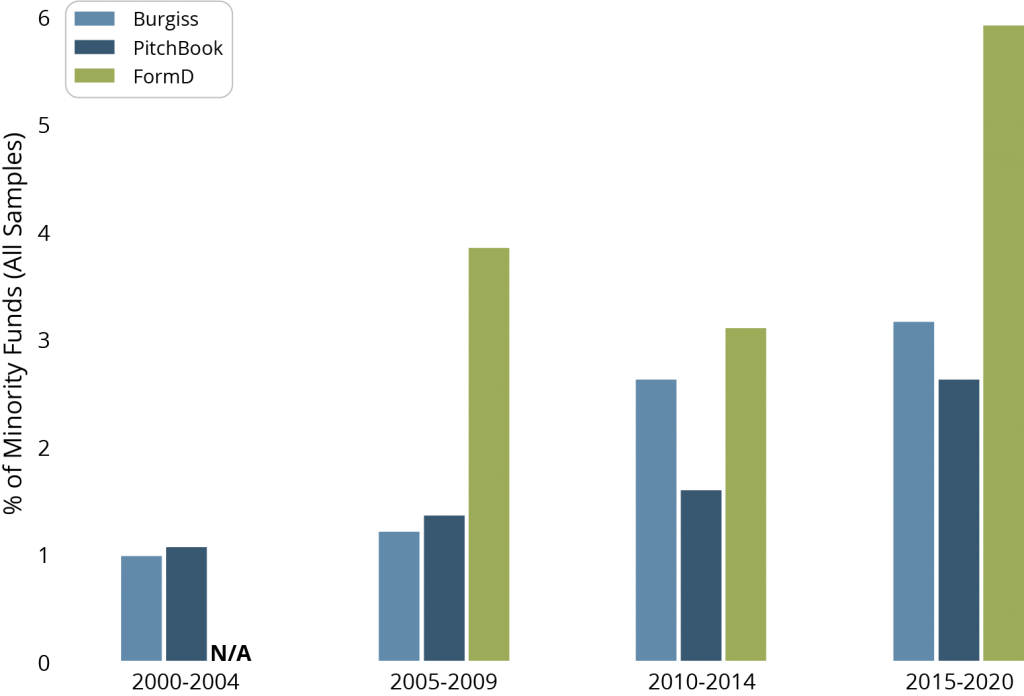

The figure below shows the fraction of all U.S.-based and -focused funds raised between 2000 and 2020 by private capital groups owned by minorities for the three samples we use for our analysis: Burgiss, PitchBook, and Form D. The Form D sample only comprises first-time funds. On a size-weighted basis, minority groups represented 3.34, 3.77, and 2.49 percent of the Burgiss, PitchBook, and Form D samples respectively. % of Minority Funds is the number of minority funds raised over a given period divided by the total number of funds. There are no funds in the Form D sample from 2000-2004 because that sample only begins in 2009, when Form D’s became machine readable.

Given the evidence on the relationship between diversity of the executive team and financial performance, it is puzzling that more startup teams are not diverse and that diverse teams face fundraising difficulties. Several reasons have been proposed for this lack of diversity in early-stage funding.

First, it’s possible that nonminority investors are biased against minority founders.6 As such, low demand for minority founders from investors might explain the paucity of minority startups. Second, some argue there is a pipeline problem: not enough high-quality minority founders available to fund. That is, the supply of talented minority founders might explain the lack of diversity. Third, there might be a potential disconnect between the network of venture capitalists funding startups and executives at companies formed by diverse founders.

Recent research by Cassel, Lerner and Yimfor (2022) provides supporting evidence for the network effect.7 Minorities are underrepresented among venture capital general partners, and the minority GPs in the industry are more likely to exit during periods of low returns. Given that minority GPs are three times more likely to fund minority entrepreneurs, low fundraising prospects by minority GPs could partly explain the low levels of fundraising by minority entrepreneurs.

Other recent research by Cook, Marx and Yimfor (2022) provides evidence against the pipeline argument by showing that Black and female founders that apply for a patent are just as likely to be granted the patent as non-Black founders but are less likely to raise funding from venture capital firms.8 This is the case even through other sources of funding such as SBIR grants, crowdfunding, accelerator funding and angel funding appear to provide equitable access to these Black and female innovators. These findings suggest that minorities “in the pipeline” also have trouble accessing VC funding. One factor that seems to mitigate this funding gap is the presence of minority GPs, who are more likely to fund minority startups.

The evidence leads us to the conclusion that a combination of bias (the funding gap disappears at later stages of funding, consistent with models of biased beliefs) and networks (minority founders are less likely than non-minority founders to have shared work histories with non-minority venture partners) explains, at least in part, the lack of funding for minority startups, leading to the low levels of diversity in startups.

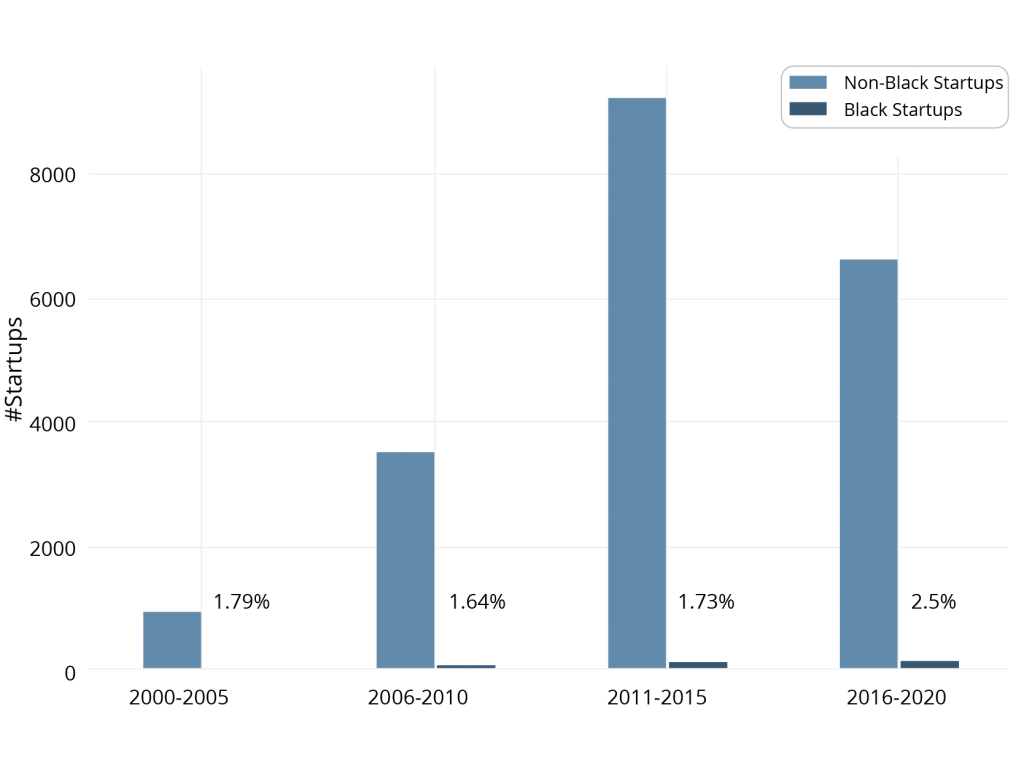

The figure below plots the number of U.S.-based startups in our final sample that were formed between 2000 and 2020 by whether the startup was formed by Black founders. Black Startups is an indicator that equals one when all the startup’s founders are Black. We impute founder race using images, which we classify using a combination of image processing tools and clerical review. The bar between 2000 and 2005 is missing because of the scale of the y-axis. There are 21 Black-owned startups in our sample between 2000 and 2005.

These frictions in access to venture funding have important implications and represent missed opportunities. Several studies have shown that diverse teams that surmount these frictions perform better. There are several mechanisms that might explain better performance by diverse teams.

Diverse teams may generate larger profits because they are better at inventing and innovating relative to nondiverse teams. Startup teams can either exploit existing ideas, for example by devising quick go-to-market strategies, or can develop better solutions to existing problems by inventing and innovating. Exploiting existing ideas is less profitable in the long run because other startups can easily enter the industry, eroding the competitive advantage of the incumbent. However, inventing and innovating can be protected by patents, which can lead the company to enjoy a competitive edge for as long as the patent is valid — 20 years in the United States.

Gompers et. al. (2016) show that when venture capitalists syndicate deals with ethnically similar VCs, they tend to underperform and when academics collaborate with other people of similar ethnicity, the papers they write tend to publish in lower-impact journals and have fewer citations (Freeman & Huang, 2014).9 That is, teams with greater ethnic diversity generate papers that make more of a splash in the scientific literature, and syndicates of diverse investors are more likely to pick better-performing startup teams.

In the wake of the racial justice movement that followed the George Floyd protests, policymakers and practitioners have pondered the best way to increase minority representation in economic opportunity. Our research has overcome the challenge of the lack of disaggregated data by race and taken two important first steps:

Further, our research suggests the following paths to increase funding for diverse-owned high-growth companies:

More generally, our research also suggests that minority entrepreneurs looking for venture capital funding can increase their chances of success by targeting minority partners (especially from their alma maters). Further, venture groups looking to increase their investments in minority-owned companies might also benefit from collaborating with minority groups or expanding their search outside their partners’ work or education networks.

On the research front, understanding frictions affecting diversely owned firms requires disaggregated data. Private capital databases, such as Burgiss, can facilitate this effort by including data on private capital group ownership and portfolio companies that are disaggregated by race and gender.

This insight is part of our yearlong, solutions-based analysis of stakeholder capitalism. Interested in learning more from Kenan Institute Distinguished Fellow Emmanuel Yimfor? Join us tomorrow for a special lunch presentation in Chapel Hill! Learn more and register today.

1 Dolan, K.A.& Peterson-Withorn, C. (2022). Forbes Worlds Billionaires List. Forbes. https://www.forbes.com/billionaires/

2 See Derenoncourt et. al (2020)

3 Cassel, Lerner, and Yimfor (2022) and Cook, Marx, and Yimfor (2022)

4 U.S. Bureau of Labor Statistics. (2019, October). Labor force characteristics by race and ethnicity 2018 (BLS Report 1082). https://www.bls.gov/opub/reports/race-and-ethnicity/2018/home.htm

5 Lorenzo, R., Voigt, N., Tsusaka, M., Krentz, M., & Abouzahr, K. (2018, January 23). How Diverse Leadership Teams Boost Innovation. BCG.https://www.bcg.com/publications/2018/how-diverse-leadership-teams-boost-innovation and McKinsey & Company. (2020) Diversity Wins: How Inclusion Matters. https://www.mckinsey.com/~/media/mckinsey/featured%20insights/diversity%20and%20inclusion/diversity%20wins%20how%20inclusion%20matters/diversity-wins-how-inclusion-matters-vf.pdfm

7 Cassel, Lerner, and Yimfor (2022)

8 Cook, Marx, and Yimfor (2022)

9 See Freeman, R. B., & Huang, W. (2015) and Gompers, P. A., Mukharlyamov, V., & Xuan, Y. (2016)