Increasingly, Wall Street has been advocating for investment strategies based on environmental, social and governance factors, arguing these generate “more stable and higher long-term returns.” Backing the logic was, among other evidence, the relative resilience of ESG-labeled assets at the height of the pandemic.1 The outperformance of ESG has come under scrutiny, however, including recent data showing long-run underperformance of ESG funds over the past five years.2 In this Kenan Insight, we provide some clarifying evidence based on recent research that revisits some fundamental questions: why and how some investors take ESG factors into account in the first place.

Why Is ESG Becoming Such a Controversial Topic?

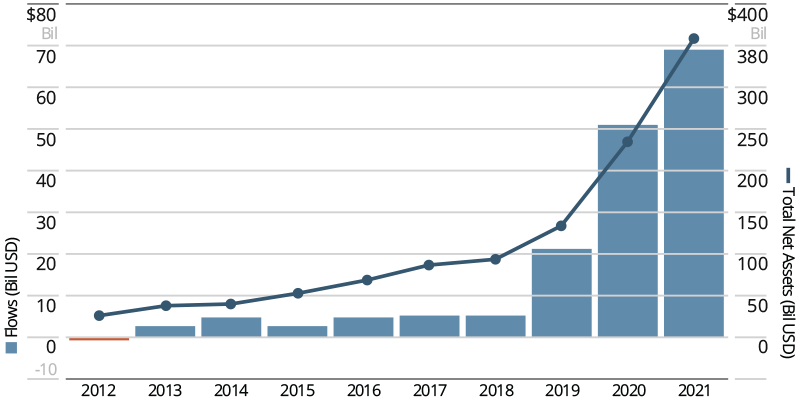

ESG investing in the U.S. has moved from a niche market to the mainstream over the last two years (see Figure 1). With this newfound popularity has come increasing controversy. Proponents of ESG investing tout the potential benefits to the corporate bottom line that also align with their broader societal goals, concocting a “doing well by doing good” rhetoric. However, detractors worry that the benefits of ESG are overstated and that ESG can result in muddled outcomes and unwarranted economic dislocation in certain industries (e.g., oil and gas), including lower employment and competitiveness. One of the biggest challenges in weighing potential costs and benefits is the lack of an agreed-on framework for evaluating the impact of ESG investing. To tackle it, we discuss some recent research that helps us sort through how ESG has affected expected investment returns and thus the cost of capital for companies. In short, the evidence suggests, for better or worse, that nonpecuniary aspects of ESG are increasingly important and thus have the potential to impact operations and real investment by corporations. In other words, ESG-focused investors care about more than just returns and thereby are having an impact on corporate behavior.

Figure 1: Growth of ESG Investment in the US

**Source: Morningstar Direct as of Dec. 31, 2021. Includes Sustainable Funds as defined in Sustainable Funds U.S. Landscape Report, January 2022. Includes funds that have liquidated, but excludes funds of funds.

But first, let’s take a step back. ESG is a large and complex topic with the potential to affect almost every facet of a company, from how it engages its employees and customers to the types of inputs (e.g., energy) used in operations. To further complicate the problem facing investors and managers, there is no single accepted framework (or rating system) for evaluating ESG factors to decide the appropriate plan of action. Most fundamental is the tension between shareholder profit maximization, which has historically been viewed as the primary corporate objective, and benefits going to other stakeholders.3 Academics and practitioners have been grappling more and more with the question of how to prioritize shareholders and other stakeholders. For example, numerous studies have examined associations between ESG and equity returns, yet only a slight majority have documented a positive relation between ESG attributes and stock performance.4 In fact, recent theory suggests that in equilibrium, the willingness for some investors to pay a premium for what they view as desirable ESG characteristics implies lower returns in the future for companies that rate highly on ESG metrics.5

At an intuitive level, ESG investing ties hands of profit-maximizing investors as they commit to underweight or screen out companies that have undesirable ESG characteristics but nonetheless generate profits. This reluctance to invest results in those companies selling at a discount and others with desirable ESG characteristics possessing a relative valuation premium, a so-called greenium. Anytime investors are paying a relative premium, they should expect long-term underperformance. What makes this more complicated, and hard to investigate empirically, is that looking back at historical returns, it is hard to separate the positive performance attributable to a growing greenium (due to persistently growing ESG-integrating capital, as illustrated in Figure 1) from the lower expected performance going forward.

So why is this controversial? If ESG is not all about win-win opportunities, investors, managers and policymakers need a clear picture of exactly what the trade-offs are. For example, when ESG investors care about something other than returns, this will affect decisions made by managers and boards. In essence, the traditional link between profit-maximizing decisions and firm valuation is now broken because investors value nonpecuniary factors.

What New Evidence Says About Investors’ Expectations on ESG Returns

To unpack whether investors place any substantial value on nonpecuniary factors assumed in ESG, it is critical to first explore what they expect their ESG investments’ returns to be. If some market participants expect lower returns, then we know they are willingly choosing ESG over profits. Fortunately, some new financial models provide a mechanism for doing this fairly precisely, at least for the subset of companies with listed options.6

A recent research paper by UNC Kenan-Flagler Business School finance doctoral student Paul Yoo examines expected market returns derived from option prices across companies with different ESG attributes. Specifically, the analysis looks at how expected returns relate to two types of ESG factors, profit-maximizing (pecuniary) risk measures and intangible (nonpecuniary) measures. The pecuniary risk (Risk) measures companies’ exposure to ESG risk factors such as climate, human capital, or regulation that accompany material consequences when realized, providing a good measure of the financial benefits related to hedging against ESG risks. The intangible measure (Intangible) corresponds to investors’ nonpecuniary preference such as nonmonetary benefit from investing in a socially responsible manner.7 Since investors’ ESG considerations are multidimensional, this approach allows us to understand to what extent two inherently distinct preferences affect U.S. public equity prices.8

The results of the analysis show that both the pecuniary (Risk) and nonpecuniary (Intangible) ESG ratings explain variation in the expected-return measures in a way consistent with the ESG greeniums described above. That is, more favorable ESG ratings result in lower expected future returns. Moreover, the size of the effects can be substantial. For example, over the last decade, low-Risk and high-Intangible stocks are generally expected to underperform high-Risk and low-Intangible stocks by roughly 2.1% a year based on the most conservative estimate.

Just as interesting are how the differences in expected returns have evolved over the last decade as ESG has been more widely measured and investors have adopted ESG into their process. As shown in Figure 2, the effect of ESG-related Risk on one-month-ahead expected returns over a rolling window of the past five years was decidedly positive (about 0.4% to 1.5%) between 2012 and 2017, but the effect has decayed in recent years to net zero before bouncing back during the pandemic. This is consistent with the pecuniary risks associated with ESG factors being internalized by companies (or at least for the large companies with listed options represented in the sample). These risks are potentially more apparent to companies or more easily addressed than nonpecuniary factors (which might, for example, be more intrinsic to a company or industry).9

Figure 2: ESG Risk Premia

****The Risk measure is based on RepRisk index. The vertical-axis represents the change in 1-month ahead expected returns (in annual %) associated with one standard deviation increase in RepRisk index. The sample focuses on S&P 500 stocks. Details are provided in Yoo (2022).

In contrast, Figure 3 shows that the nonpecuniary Intangible factor has changed from having a variable effect on one-month-ahead expected returns (between -0.5% and 1.5%) over five-year rolling windows in the early 2010s to being associated with a consistently lower return of around -3% in recent years. This finding is consistent with a growing greenium associated with nonpecuniary ESG factors.10 Moreover, it suggests companies’ costs of capital are likely to be meaningfully and persistently different based on these factors.

Figure 3: ESG Intangible Premia

**The Intangible measure is based on MSCI’s Intangible Value Assessment (IVA) data. The vertical-axis represents the change in 1-month ahead expected returns (in annual %) associated with one standard deviation increase in IVA ratings. The sample focuses on S&P 500 stocks. Details are provided in Yoo (2022).

Takeaways for Managers and Investors

The existence of substantial valuation effects for nonpecuniary ESG preferences has important value implications for businesses and investors. For managers, even though setting out and committing to social objectives has upfront costs, the latest evidence suggests that efforts to develop certain ESG characteristics will have significant impact on the firm’s cost of capital. Yet for investors, this is a double-edged sword in that the lower cost of capital is synonymous with lower future returns. Thus, these results caution against the “doing (financially) well by doing good” rhetoric. Finally, for the ESG skeptics, these results suggest that they are fighting not an extraneous force that seeks to change how businesses operate but instead the preferences of investors, which directly affect shareholder valuation. In this sense, directors must acknowledge the potential impact of ESG factors (and increasingly nonpecuniary factors) on valuations as they exercise their fiduciary responsibilities.

1 For a recent evidence, see Albuquerque et al. (2020), for example.

2 See, for example, this Bloomberg article.

3 For example, see Kenan Insight published last December.

4 See meta-analysis papers like Friede et al. (2015), Coqueret (2021), and Whelan et al. (2021).

5 See Kenan Insight published in April for more details.

6 New models include Martin and Wagner (2019) and Kadan and Tang (2020).

7 By construction, the Risk and Intangible ratings contain information that are more relevant to pecuniary and nonpecuniary ESG considerations, respectively. This is because the former intentionally confines its scope to gauge firms’ exposure to future ESG-related pecuniary risk events, while the latter puts emphasis on evaluating the gravity of firms’ ESG pledges, commitments and strategies in place.

8 For some evidence for each preference, see Riedl and Smeets (2017), Hartzmark and Sussman (2019), and Humphrey et al. (2021) for nonpecuniary preference and Albuquerque et al. (2018), Hoepner et al. (2022), and Seltzer et al. (2021) for risk-mitigating preference.

9 Notice the countercyclical trend of ESG Risk premiums: high (low) in periods with (without) recessions — the Great Financial Crisis and COVID-19 crisis. That the academic literature has long documented higher risk compensations during bad times confirms ESG Risk premiums arise from pecuniary ESG factors.

10 Unlike ESG Risk premiums, ESG Intangible premiums are acyclical, suggesting they arise from nonpecuniary considerations (or factors less relevant to pecuniary risks, at the least).