The explosive growth in ESG investing has created considerable confusion about what investors should actually expect. Academic studies that have examined how ESG factors relate to both corporate operating performance and investment outcomes have found mixed results. Effects on operating performance appear consistently (though not uniformly) positive and suggest companies with high ESG scores are better in a number of ways. The evidence on investment returns is more ambiguous — some studies find the stock prices of companies with high ESG ratings outperform, but others find no measurable effects, and some even document lower monetary returns.1

In this Kenan Insight, we unpack what investors should expect from ESG and try to reconcile this with both financial theory and the empirical evidence. The bottom line is a bit complicated, because investors can expect either higher or lower returns related to ESG factors depending on specific market conditions. For example, in the short run, companies with high ESG ratings can experience higher stock returns as the number of investors who care about ESG factors increases. This derives from ESG investors’ willingness to pay a premium for these companies, thus driving up their stock prices. In the long run, however, after investor preferences have settled, a new equilibrium results in highly rated ESG companies experiencing lower returns. This is because, all else the same, the runup in ESG stock prices means that new investors are paying more (i.e., a premium) for any given asset, which necessarily means lower returns on that investment.

A simple model for ESG investing

To develop a deeper understanding of the forces at work, we can consider a simple, stylized stock market with just two companies.2 The two companies are identical except for a single crucial difference: One company, which we will call Green Inc., uses power generated only from renewable energy sources, whereas the other company, which will call Brown Inc., uses power generated only by burning coal. To keep things simple for now, we assume that both power sources have the same cost, reliability, etc., and this information is common knowledge. Of course, there are other market and ESG considerations, so we will relax this strong assumption later. We also assume that investors make investments consistent with their preferences and that markets are competitive.3

To more easily understand how ESG investing affects returns through time, we also want to assume three distinct eras of investing, which are based solely on the preferences of investors. First is an era before investors care about ESG factors — we will call this the “pre-awakening” era. Second is an era when many investors start to care about ESG factors and are willing to pay a premium for companies that score well on ESG factors — we call this the “ESG awakening” era. This means that ESG investors care about both monetary and ESG returns. The third and final period is the “post-awakening,” when investor preferences have settled into a new equilibrium around ESG — many care about ESG but some don’t, and the sizes of these camps are fairly stable.

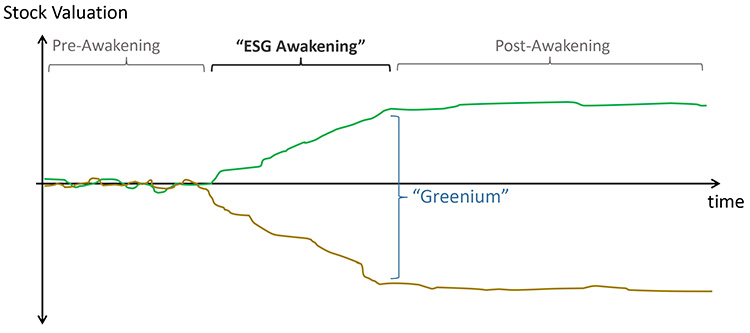

What do the paths of the Green and Brown stock prices look like over these eras? Figure 1 shows that the valuations in the pre-awakening era are basically the same — as they should be since the companies are identical from a purely financial perspective. During the ESG awakening, however, investors start to care more and more about ESG factors and so Green Inc. starts to trade at a premium to Brown Inc. We’ll call this wedge a “greenium” because it is driven solely by investors’ preferences for green energy over brown energy and not the financial performance of the company. In the post-awakening era, investor preferences have stabilized, thus valuations will stabilize and there will be a more stable, but still positive, greenium.

Figure 1: Green Inc. and Brown Inc. Stock Prices

What does Figure 1 mean for relative stock returns for Green Inc. and Brown Inc.? Of course, in the pre-awakening era, prices are about the same and so returns will be about the same as well. It is also clear that during the ESG awakening, the stock of Green Inc. will outperform that of Brown Inc. What may be less obvious is that in the post-awakening era, the stock of Green Inc. will generate lower returns than the stock of Brown Inc. This comes from the fact that we have assumed that the stocks have identical financial performance — i.e., both companies have the same dollar value in earnings and pay the same dollar value in dividends before and after the ESG awakening but the valuation of Green Inc. is higher. Consequently, it must be that the post-awakening returns are expected to be lower. This is simply a mathematical fact deriving from the definition of return being measured as a percent of price paid for an asset. ESG investors are comfortable with this new equilibrium because they are willing to accept lower monetary returns in order to receive higher ESG scores. We see evidence of this with “green bonds,” where, for example, investors can hold nearly identical German government bonds, but with some that are designated as “green” given how the proceeds are invested. These German green bonds have higher prices and lower yields (i.e., lower expected returns).4

ESG and operating performance

The example above is deliberately oversimplified to make the point about higher returns during the ESG awakening and lower returns post-awakening. But there are other factors to consider. Perhaps most important is that corporate attention to ESG factors might change the cash flows of companies. In our example, there are any number of ways that Green Inc. might benefit financially because of its focus on ESG. For example, ESG focus could lead to higher profits from more efficient operations (e.g., energy savings), better brand image and customer loyalty, as well as superior employee satisfaction and retention.5

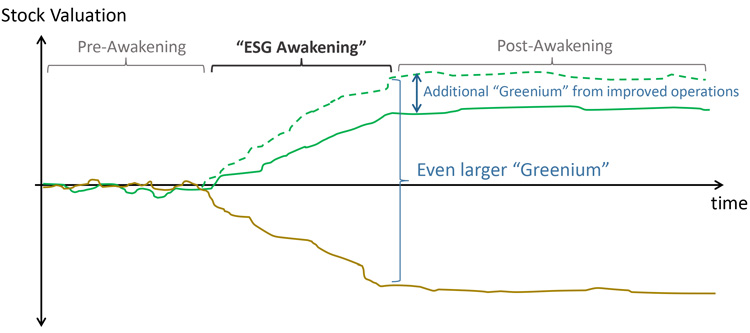

But that’s not all — there are other potential benefits from the ESG greenium. The flip side of the long-run lower expected return from the greenium is a lower cost of capital for Green Inc. Managing ESG factors can also be a risk mitigator if it helps companies assess and manage hazards associated with environment/climate, headline risk associated with corporate actions (e.g., improved social awareness), and weak governance/controls. If risks are lower, Green Inc.’s costs of equity and debt should decline during the ESG awakening and stay lower than that of Brown Inc. Finally, Green Inc.’s lower cost of capital equates to a lower hurdle rate for new investment, which not only increases growth (potentially at the expense of Brown Inc.) but also could allow for investment in more green projects. All of these create a virtuous circle that further benefits the company’s profitability and increases the greenium. Figure 2 shows this graphically (dashed green line) as an even larger greenium developing during the ESG awakening.

Figure 2: Green Inc. and Brown Inc. Stock Prices with Improved Operations from ESG

It’s also important to understand what Figure 2 tells us about stock returns for Green Inc. when there are better profits from ESG. The investment returns to Green Inc. stock will be even higher during the ESG awakening as the greenium grows larger. However, we still expect lower returns from Green Inc. relative to Brown Inc. in the post-awakening period. This seems counterintuitive initially — if Green Inc. is more profitable, then why aren’t returns higher? The answer comes from our assumption about widely available information about ESG and competitive markets during the ESG awakening. If investors can properly evaluate the benefits of ESG, then those benefits get built into the price of Green Inc. and won’t drive future returns.6 Returns for Green Inc. will be higher in the post-awakening period only if there are unexpected changes to ESG factors or beliefs about the financial impacts of ESG factors improve.

Can ESG investors do good and do well?

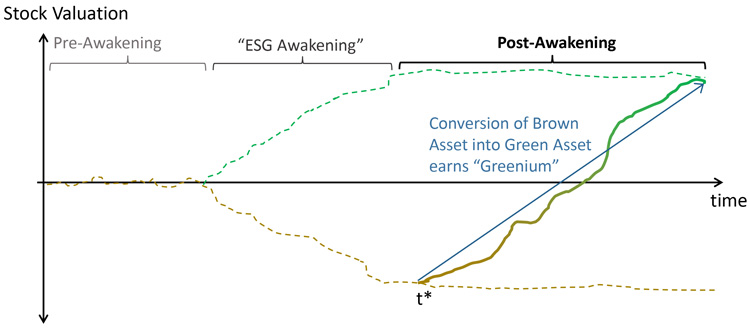

Figure 3: Returns from Converting Brown Inc. into a Highly Rated ESG Company

Is there any way for ESG investors to earn higher returns in the long run? In fact, there is. While the passive investor of Green Inc. during the post-awakening period earns lower returns, an “ESG activist” can potentially beat the market by investing in Brown Inc. and converting it to a highly rated ESG company. Figure 3 shows what this might look like graphically. At time t* the activist investor buys Brown Inc. and over time improves its operations and ESG scores so that it eventually creates an ESG awakening for Brown Inc. and thus the stock starts to command a greenium. In this case, the activist ESG investors will earn a greenium minus whatever costs are incurred in the conversion.7 These might be actual physical investments — for example, costs associated with replacing coal power with solar power — but these could also be costs associated with engaging management, changing corporate culture, etc.8

ESG investing in the real world

The real world is much more complex than the simple model discussed here. In practice, ESG means different things to different investors, and many factors are hard to measure. Furthermore, what’s material to individual companies varies by industry, by country, and over time. For example, a global multinational company likely faces diversity issues that are quite different in the Americas, Europe, and Asia. We have also assumed that there is a clear differentiation between eras and most importantly that we can easily separate the ESG awakening from the post-awakening. In reality, ESG issues are likely to continually evolve as will investor preferences and perceptions about the relative costs and benefits of ESG policies.

The relationship between ESG factors and investment returns can be quite complex, but the model described above allows us to understand the forces at work in a rigorous economic framework. This framework indicates that highly rated ESG companies are likely to earn higher returns when: i) investor preferences for good ESG companies are increasing, ii) the share of ESG investors is increasing, and iii) unexpected new financial benefits from ESG are realized. This is because all of these generate an increasing greenium. On the other hand, highly rated ESG companies will tend to earn lower returns when markets are in a post-awakening equilibrium.

Finally, it is worth noting that this equilibrium is likely to make everyone as happy as they can be in an ESG world. Pro-ESG investors are happy because higher valuations with lower cost of capital provides incentives for adopting and investing more in ESG. These pro-ESG investors are (on average) fine with earning lower returns for companies that operate in ways they like. But, interestingly, even “anti-ESG” investors are happy because they get to invest in higher-returning stocks in the long-run — either because they earn higher equilibrium returns on brown companies or can benefit from conversion to green companies. In this sense, ESG investing really can be a win-win.

In a future Kenan Insight, we will explore how understanding the returns from ESG investing can help us identify where markets will be successful in generating desired social outcomes and where policy interventions will be required.

1 For a meta-analysis of recent studies see Whelan, T., U. Atz, T. Van Holt and C. Clark (2021), ESG and Financial Performance, NYU Stern Center for Sustainable Business white paper.

2 The model discussed here draws largely on Pástor, L., R. Stambaugh, and L. Taylor (2021), Sustainable investing in equilibrium, Journal of Financial Economics 142(2), 550-571.

3 These are fairly standard assumptions and consistent with investors being rational and risk-averse, transaction costs being low, etc.

4 Pástor, L., R. Stambaugh, and L. Taylor (2021b) Dissecting Green Returns, University of Chicago, Becker Friedman Institute for Economics Working Paper No. 2021-70.

5 In fact, there is empirical evidence consistent with each of these. See, for example, Whelan et al. (2021) and cites therein.

6 As noted above, the only determinant of the length of the ESG awakening period is how long it takes for investors to get fully on board the ESG train.

7 The greenium will be larger because you are starting with a lower valuation. However, the total return will be based on the conversion costs.

8 These could be any number of things that economists would describe as incurring (and then minimizing) agency costs.