Event • Jan 26, 2023

There are few topics in business more current, more covered or more controversial than corporate environmental, social and governance (ESG) responsibilities. Proponents claim a business’s adoption of such principles yields outcomes that benefit all parties, driving win-win scenarios for internal and external stakeholders alike. But critics dismiss ESG implementation as a performative PR ploy, and argue that considering such non-pecuniary factors in corporate decision-making is unsustainable. Our (independent, nonpartisan) findings indicate both sides of the debate are missing the mark – and in hopes of advancing more productive conversations, we introduce below a research-based model for examining the trade-offs of ESG adoption for businesses large and small.

Throughout 2022, the Kenan Institute has been exploring environmental, social and governance (ESG) factors as they relate to the decisions of corporate managers and investors. We have framed this analysis within the broader notion of “stakeholder capitalism,” a model in which business decisions explicitly consider the impact on corporate stakeholders such as employees, customers, suppliers, communities and even the planet. A milestone in the stakeholder capitalism movement was the 2019 Business Roundtable New Statement on the Purpose of a Corporation signed by 181 CEOs, which states:

“Each of our stakeholders is essential. We commit to deliver value to all of them, for the future success of our companies, our communities and our country.”

Yet, the Business Roundtable statement also declares that the purpose of a company includes “generating long-term value for shareholders, who provide the capital that allows companies to invest, grow and innovate.”

Unfortunately, the statement provides no direction indicating whether the interests of other stakeholders come at the expense of shareholders, and if so, how such trade-offs should be managed. If caring about the interests of other stakeholders is only about generating long-run value for investors, then this is, in fact, no different than the traditional model of shareholder supremacy championed by Milton Friedman (among others).1 Consequently, the Business Roundtable statement is largely vacuous and could mean almost anything to anyone depending on how it is read – perhaps deliberately.

The Business Roundtable’s vision is not unique in this way. We have been unable to identify any rigorous model of stakeholder capitalism that provides specific direction on how trade-offs between stakeholders should be evaluated. Furthermore, there appears to be little consideration in the discussion around stakeholder capitalism about the fiduciary responsibilities of management and the corporate board of directors. Unless we believe that there will be significant modifications to the legal framework defining fiduciary responsibilities of for-profit companies, any viable model of stakeholder capitalism must be constrained by only considering actions that maximize shareholder wealth.

At first blush, this suggests no room for a stakeholder capitalism model that strays from traditional shareholder supremacy. However, there is an alternative: In this Kenan Insight, we describe a new, rigorous and precise model of stakeholder capitalism that deviates from the traditional model of shareholder supremacy by demonstrating how certain corporate actions that benefit other stakeholders can decrease profitability and yet increase shareholder value. While this may seem counterintuitive, our model is quite straightforward and rests only on an intuitive extension to the traditional model of profit maximization by allowing investors to value more than just financial profits. In particular, if some investors care about a business’s stakeholders, and these preferences are reflected in their valuations of corporate equity, then it is possible for a wedge to open up between corporate profits and shareholder wealth.

Before diving into a more rigorous analysis, we provide a simple, stylized example to illustrate this model at work. Consider a manufacturing company that needs to build a new production facility and has two options: It can build a traditional facility for $100 million, or a more environmentally friendly facility for $115 million. For simplicity, assume there is no difference in the other cash flows (e.g., efficiency) of the environmentally friendly facility – perhaps the only distinction is that it was constructed with more sustainable (and expensive) building materials that are otherwise identical in specifications. In the traditional model of shareholder supremacy, building the environmentally friendly building would cost the company another $15 million with no cash flow benefits and thus would decrease shareholder wealth by $15 million. Depending on one’s interpretation of the law, this could even be considered a violation of fiduciary responsibility by the company’s management and board.

But perhaps the issue is not so simple. What if some of the company’s shareholders have a preference for the company building the environmentally friendly factory instead of the traditional factory? More specifically, suppose that, on average, shareholders would be willing to pay 2% more for the stock of the company if it owns and operates the green factory. This equity price premium is exactly the “greenium” we discussed in a previous Kenan Insight.2 Now, let’s assume that the market cap of the company is $1 billion. If the company built the green factory, the market value of the company’s equity will increase by $5 million (2% of $1 billion is $20 million minus the $15 million in higher construction costs). This happens even though the company’s profits will decline by $15 million. If the company’s management seeks to maximize shareholder value, clearly they should build the green factory despite the lower profits.

Critically, our example demonstrates how a corporate action that lowers profits can still be consistent with fiduciary responsibility. That said, it also shows there is a limit to what the company can spend. This limit depends on the size of the greenium, which in turn depends on the preferences of shareholders for non-pecuniary corporate actions. What if the greenium for a green factory was just 1%? In this case, building the green factory will decrease the market value of the company’s equity by $5 million (1% of $1 billion is $10 million, minus the $15 million in higher construction costs). In sum, the key insight is that investor preferences for non-pecuniary actions that benefit different stakeholders will determine premiums (or greeniums) associated with those actions. The valuation premiums then tell managers the maximum amount they can spend on those actions. Of course, premiums can be zero for some (probably most) non-pecuniary actions – meaning managers should not consider investments associated with those projects or stakeholders. In this way, our model provides exact and prescriptive advice for how managers and boards should consider all corporate stakeholders.

We can now more carefully describe the model we have developed for stakeholder capitalism. Following the model of Pastor, Stambaugh, and Taylor (2021, henceforth PST), we consider an economy in which investors care about the economic profits a company generates as well as the effects the company’s operations have on society. In particular, some companies have what investors consider to be negative impacts while other companies have positive impacts (i.e., positive and negative economic externalities). Investors may observe and measure these non-pecuniary impacts through tools like ESG factor ratings. The PST model considers just one factor, but we extend this to an arbitrarily large number of possible factors that some investors value. As in the PST model, companies with characteristics that investors feel are beneficial to society will have higher valuations as compared to companies with characteristics that investors feel are harmful to society. The magnitude of the valuation premiums will depend on the strength of investors’ preferences for each factor. The more investors care about a particular factor, the larger the valuation premium will be for that factor. This model, like the PST model, holds implications not only for portfolio holdings of investors, but also for corporate actions.

This model of stakeholder capitalism has several important implications:

Finally, we note that this model of stakeholder capitalism should make investors of all types as happy as they can be in a world where some investors have non-pecuniary preferences. For example, the strongest advocates of ESG can buy the highest-rated companies for the factors they care most about – and feel good about their investments while providing a lower cost of capital for the projects that are most important to them. In contrast, investors who do not care about non-pecuniary corporate actions can invest in companies with low commitments to other stakeholders and, in turn, these investors will earn higher financial returns in equilibrium.

The discussion so far begs the question: Is this really happening? Or, more precisely stated, can we actually observe the valuation premiums associated with non-pecuniary investor preferences that will serve as the inputs to corporate decisions? Our ongoing research is digging into this exact question more deeply, but we summarize below recent evidence suggesting the answer is yes.

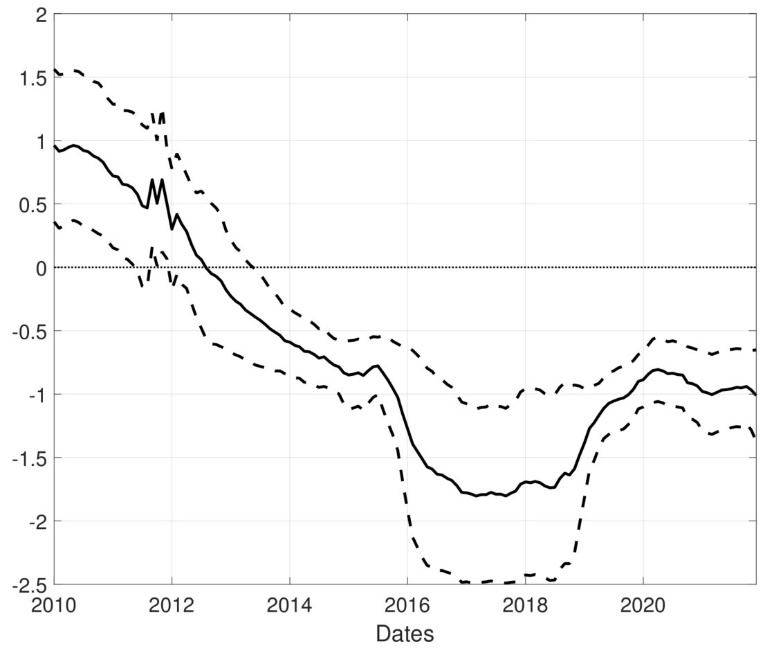

A second paper by Pastor, Stambaugh, and Taylor (2022) finds evidence of a growing and economically significant greenium associated with climate concerns. Likewise, Van Der Beck (2021) finds the recent outperformance of an aggregate ESG portfolio in the U.S. was driven primarily by investment flows, which suggests investors are paying an increasing premium for non-pecuniary factors. In a previous Kenan Insight, we discussed results of new research by Yoo (2022) that uses option-implied expected returns to uncover valuation effects. The findings suggest a non-pecuniary ESG greenium exists in the U.S. public equity market, on top of any other ESG-related premia stemming from pecuniary concerns (e.g., regulatory ESG risks). This option-implied measure (plotted in Figure 1) has been evolving during the last decade in a way that suggests a significant move from 2010 to 2015 toward about a 1-2% lower cost of capital for large U.S. companies that rate highly on MSCI’s Intangible Value Assessment.

However, existing results do not provide the granular view of how investors value different stakeholder groups or specific projects that provide non-pecuniary benefits. The method for generating these measures is straightforward, though – at least in theory. Specifically, with data on corporate valuations and ESG ratings, valuation effects can be estimated for individual factors. (Stay tuned for a future Kenan Insight in which we will report values for exactly this type of analysis.)

In sum, we describe a model for stakeholder capitalism that generates a precise framework for corporate decision-makers to use in evaluating non-pecuniary projects. The model – which is consistent with widely accepted fiduciary standards for corporate managers and boards – derives from a very simple and intuitive extension of the traditional model of shareholder supremacy. Simply put, we assume that some shareholders care about more than money when making investments. This assumption is easily validated by observing the significant recent inflows to funds that have explicit ESG mandates. Yet that is the only non-standard assumption needed to generate a model in which managers will undertake projects that benefit corporate stakeholders at the expense of lower profits, but to the benefit of shareholder value.

This Kenan Insight is part of the Kenan Institute’s yearlong examination of stakeholder capitalism and ESG investing; learn more and join the conversation here.

1 See, for example, Milton Friedman, “The Social Responsibility Of Business Is to Increase Its Profits.” The New York Times, September 13, 1970.

2 Does ESG Investing Generate Higher Returns?

3 See, Baker, Bergstresser, Serafeim, and Wurgler (2018) and Zerbib (2019).