- Do I think we are in a recession now? No.

- Job growth is very strong and consumer spending is holding up and showing signs of a beneficial rebalancing.

- Am I worried about a recession? Yes.

- The challenge is that inflation is eating away at incomes and the Fed is going to do everything it can to tamp down on inflation — and that may very well result in a recession.

GDP, the broadest measure of economic output, contracted for the second straight quarter, stoking fears that the economy is already in a recession — and has been since the beginning of the year. But the guts of the GDP report coupled with continued strong job growth and decent consumer spending suggest that the expansion remains on track. While the official arbiters of recessions are likely to agree with me — they don’t look at GDP but rather measures like job creation — what really matters to households and businesses is whether their spending power or foot traffic is drying up.

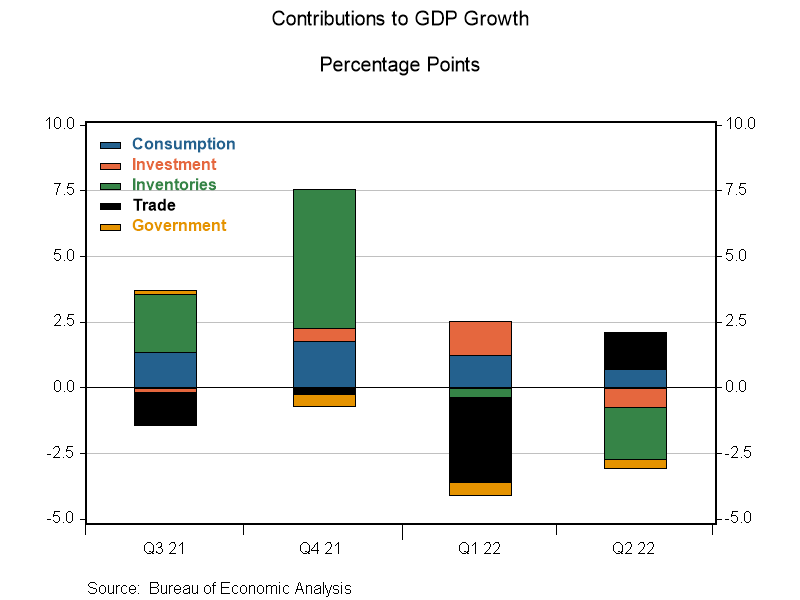

This is why we have to geek out a bit and discuss the details of the GDP report. As the figure below illustrates, consumer spending (blue bars), the largest component of economic activity, continued to grow and added to GDP in the first and second quarters. Yes, it slowed in the second quarter, but it slowed partly because of a rebalancing of spending away from goods and toward services — i.e., fewer people buying cars that are in short supply and more people going out to dinner. This rebalancing is exactly what we have been looking for to help soften the blow of some of the supply chain challenges. At the same time, after a strong Q1, business investment (orange bars) declined in Q2 because of a drop in building of both homes and business structures. It’s not clear that demand for these is weak. Rather, it could be that supply constraints are limiting building activity.

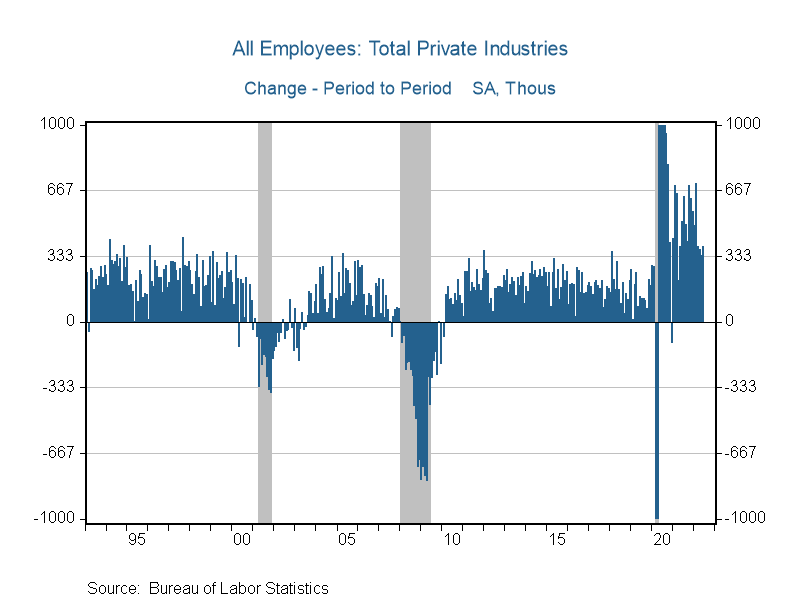

If businesses were so cautious, why did they hire 381,000 people in June? As the chart below indicates, this is an exceptional pace of hiring. In fact, it is faster than any month during the previous two economic expansions! Granted, we are still making up for jobs lost as a result of COVID-19, but this hiring reflects an optimism by businesses that they need those workers to meet current and forthcoming demand. That job creation also suggests that the economy should remain healthy as the income generated by workers drives consumer spending and business investment.

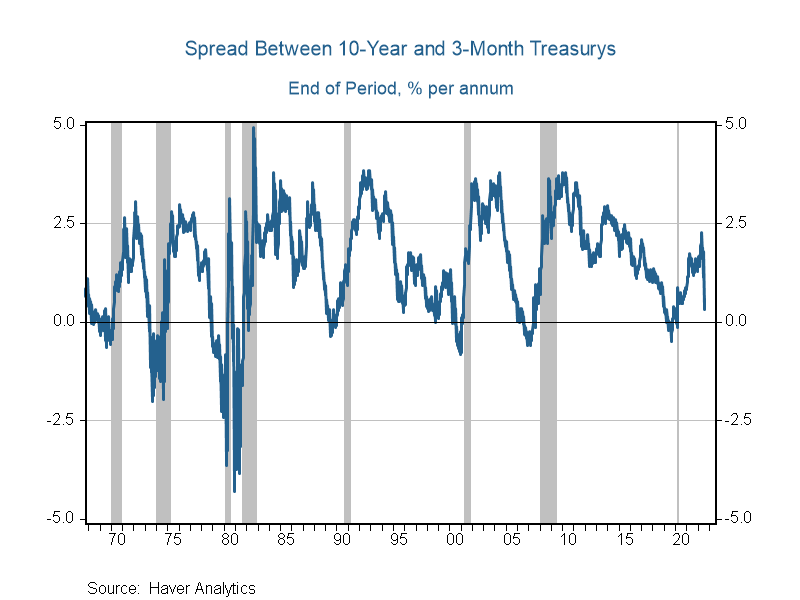

Unfortunately, inflation, the Fed, confidence, and the Treasury yield curve point to significant risks of a recession. Inflation is lowering the purchasing power of people’s incomes, which puts downward pressure on spending. That loss of purchasing power and perhaps even Thursday’s negative GDP report are lowering consumer and business confidence. As my colleague Camelia Kuhnen wrote, confidence affects spending, and people tend to overreact to bad news. Meanwhile, my favorite economic indicator — the difference between the yield on the 10-year and three-month Treasurys — has narrowed substantially over the last month (when it falls below zero, it indicates a recession a year from now, though the timing is inexact).

Normally, indicators such as confidence and the yield curve would give the Fed pause. However, for the first time in 30 years, creating a “soft landing” for the economy may not be enough to put inflation back on a path toward the Fed’s 2% inflation target. That means the Fed may have to create a recession. Fed Chair Jerome Powell acknowledged this challenge when he said, “We’re not trying to have a recession. And we don’t think we have to. We think there’s a path for us to be able to bring inflation down while sustaining a strong labor market. … We know that the path has clearly narrowed, really based on events that are outside of our control. And it may narrow further.”

The next big step in that path is next Friday’s jobs report. That’s why I would recommend tuning in that day to our 9 a.m. economic briefing, where we will break down the numbers to see whether there are any warning signs. Those could include a softening in temporary help employment, which, because those jobs can be easily cut, is a good leading indicator. We look forward to seeing you!