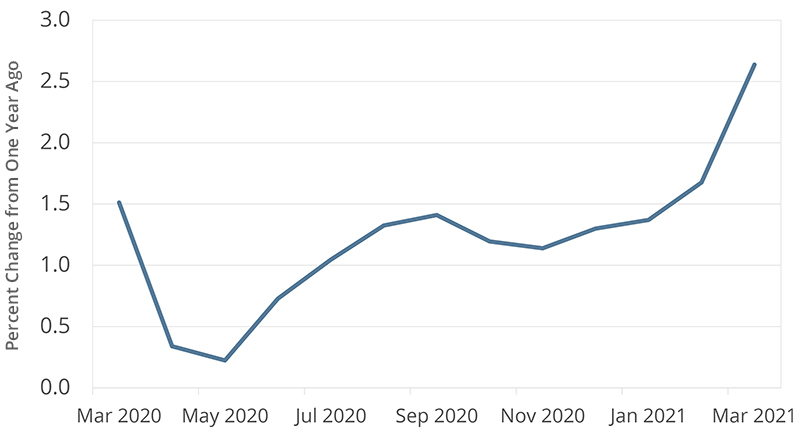

The chatter around inflation is increasing. In March, the Consumer Price Index (CPI) was up 2.6% compared with a year ago, when demand for many goods and services evaporated and the pandemic pushed the economy into a tailspin. This jump from February’s 1.7% rate was partly expected because the pandemic’s depression of prices began in the spring of 2020.

Consumer Price Index for All Urban Consumers (All Items in U.S. City Average)

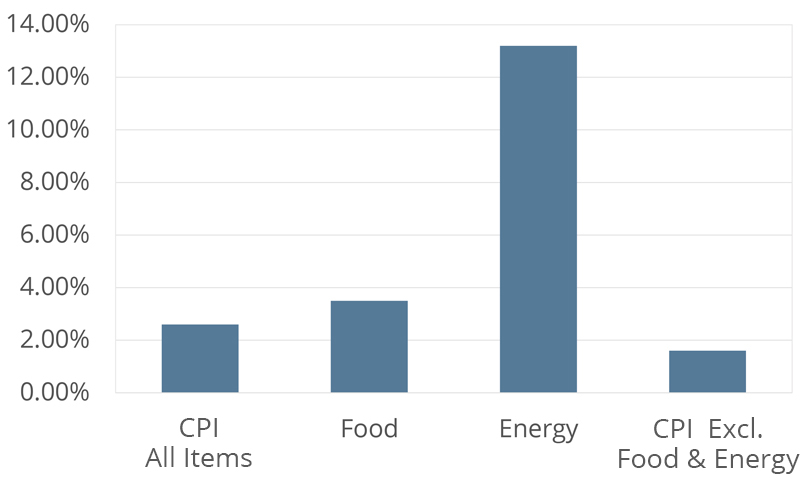

But there may be more to the rising speculation about inflation. Prices jumped by 0.6% in March alone, and the core Consumer Price Index, which excludes more volatile energy and food prices, was up by 0.3%. Commodities such as aluminum, copper and lumber are trading near all-time highs. Businesses from homebuilders to manufacturers to household goods providers are sounding alarms over supply-chain bottlenecks and mounting raw material costs. Major consumer brands are announcing plans to raise prices. Hotel, car rental and air travel rates are all up, adding significantly to a 0.4% rise in the price of services in March. Increasing vaccination rates and decreasing restrictions on businesses across the country, in addition to the latest round of $1,400 stimulus checks received by most Americans, are fueling demand as consumers emerge from lockdowns. Add in massive fiscal stimulus, a proposed infrastructure program and a highly accommodative monetary policy and it’s reasonable to question whether a perfect storm is brewing. Of most concern is what a pronounced spike in inflation would do to the rapidly improving U.S. economy.

Indeed, many economists expect inflation to keep rising in the short term, as stimulus and a year of pent-up demand pump up the economy and supply chain disruptions potentially make it hard for supply to meet growing demand — a recipe for higher prices. At its March meeting, the Federal Reserve revised its growth forecast for 2021 upwards from 4.2% to 6.5% and bumped its inflation forecasts for this year to above their 2.0% target.1

Consumer Price Index, 12-Month Percentage Change, March 2021 (Not Seasonally Adjusted)

But is a little inflation such a bad thing? A modest near-term uptick shouldn’t worry us, especially given that strong economic growth, needed and desired, usually goes hand in hand with faster growth in consumer prices. However, the headline inflation rate often masks the uneven burden of price changes. Food and gas prices, which make up a much larger share of expenses for low-income groups, have climbed much faster than the CPI indicates. Inflation — even at a subdued level — is experienced quite differently across various constituencies with diverse spending habits. Once again, low-income households which experienced the most job losses during the pandemic also are hit hardest by increasing consumer prices. The wealthier, who mostly continued to work remotely through the pandemic, experience the lowest level of inflation.

Still, the key question is whether the current rise in consumer prices is transitory or whether it might turn into a genuine long-term threat of higher and sustained inflation. The Federal Reserve believes the former. Despite higher projected inflation in 2021, the Fed expects inflation in 2022 and beyond to come back to its 2% target. In August 2020, Fed Chair Jay Powell announced a revision to his agency’s long-run monetary policy by reframing its target as an average inflation target of 2% over the long run — effectively communicating that it will tolerate inflation above that target for a limited time (like 2021) to offset periods when inflation is below the target. Essentially, this was the Fed’s attempt to counter the tendency for persistently low inflation rates to steer expectations downward. Low inflation expectations ultimately become self-fulfilling, in turn leading to lower interest rates and less monetary ammunition for the Fed to counteract recessions. Fed Chair Jay Powell appears unfazed by the recent increase in consumer prices, and the Fed has not faltered from its position that it would likely not start raising interest rates above zero until 2023.

It appears that, for the moment, most economists and professional forecasters are going along with the Fed’s view. According to the First Quarter Survey of Professional Forecasters, inflation projections are holding steady at 2%.2 There are good reasons to support this analysis. Years of unconventionally loose monetary policies followed by central banks in response to the Great Recession did not push inflation above target rates, giving the impression that central banks have successfully “anchored” long-term expectations. Furthermore, the unemployment rate has yet to recover to its pre-pandemic level and millions of workers have left the workforce, yet most are likely to return as health risks drop and children return to school. Moreover, structural trends like globalization and automation have lessened long-term inflationary pressures by weakening workers’ and companies’ ability to raise wages and prices, arguably making high inflationary periods like those experienced in the 1970s and early 1980s far less likely.

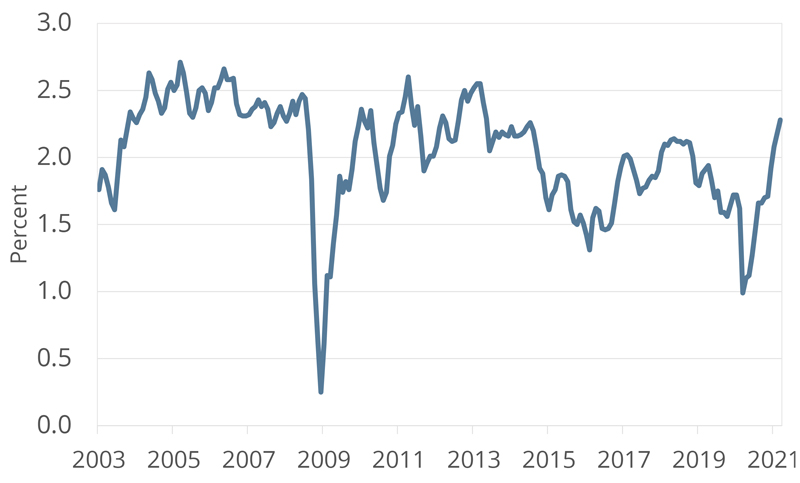

TIPS Expected 10-Year Inflation Rate

Markets appear to have been somewhat spooked by the Fed’s promise to continue its loose monetary stance even as inflation rises. Already pricing in the possibility of the central bank being compelled to raise interest rates sooner, the yield on 10-year treasuries jumped to almost 1.8% in March (from less than 1% at the beginning of the year), the highest level since January 2020. Some economists are worried about the growing risk of a prolonged period of inflation above the Fed’s target. According to a recent Bank of America survey of investors, higher-than-expected inflation has already displaced coronavirus-related tail risks at the top of investors’ fear table.3 Investors are piling into funds that buy Treasury Inflation-protected Securities (TIPS), with returns indexed to the CPI. In fact, TIPS yields are quite informative about the market’s long-term inflation expectations. For example, the difference in the yield on a typical 10-year treasury security and a 10-year TIPS is closely watched by market participants as a measure of long-term expected inflation. After dipping significantly during the early pandemic months, expected 10-year inflation today stands at 2.3%, its highest level since 2013. Clearly the bond market is less sanguine than the Fed.

Are inflation fears justified? The Fed’s new monetary policy framework certainly adds to the source of uncertainty, as no one knows by how much or for how long it will allow inflation to overshoot. For years now, the Fed has been reaping the benefits of having anchored low long-term inflation expectations; it has successfully kept short-term nominal interest rates close to zero over long periods by substantially expanding its balance sheet without jeopardizing its long-term credibility. The worry is that the Fed may be too slow and reluctant to beat back higher inflation, particularly if it takes on addressing inequality as an added mission over that of maximum employment. In addition, if politicians’ preference for lower interest rates at a time of ballooning budget deficits constrains the Fed’s ability to lean against inflation in a timely fashion, these hard-earned, long-standing low inflation expectations could quickly unravel.

So, is the Fed exhibiting overconfidence that nothing it does affects long-term inflation expectations? At a minimum, Chairman Powell does not appear to feel any urgency to address the question. The problem is that raising short-term rates might have little impact on inflation if, in the meantime, enough people doubt the Fed’s commitment to low inflation, and high long-term inflation expectations take hold.

In addition, there may be other global structural threats that further increase inflationary pressures. Some economists argue that the trend of globalization that marked the past few decades is receding, giving way to rising protectionism. Further supply shocks could exacerbate price pressures. Likewise, a more rapid-than-expected pace of vaccinations worldwide could intensify global demand growth. And what will governments do when faced with a choice of inflation versus fiscal tightening?

The doomsday scenario

Inflation hawks are sounding alarms, and memories of the 1970s are being presented as cautionary reminders. Surely we are far from the double-digit inflation rates of that era. Still, significantly higher inflation with a Fed behind the curve is an extremely dangerous, if low probability, risk. In this scenario, interest rates would rise both because of higher required compensation for inflation by investors and from the Fed playing catch-up monetary policy with much higher “real” interest rates. Imagine that inflation expectations rise to 4% and the Fed is effectively forced to respond with a sharp increase in the real short-term interest rate to 3%. The resulting 7% interest rate (expected inflation plus the real rate) may still seem modest by historical standards, but consider the ramifications on highly levered households, businesses and governments. The U.S. would experience a significant decline in the prices of financial assets, as well as residential real estate. Many lower-income households, which typically have greater debt burdens, would face severe financial pressures (e.g., a jump in personal bankruptcies). Corporations would be challenged by much higher interest expense and more constrained access to external capital. Likewise, federal, state and local governments would all experience much higher debt service costs, which would in turn drive fiscal austerity. In short, the economy would shift rapidly from boom to bust as the Fed tries to put the inflation genie back in the bottle. Of course, we all hope that our current taste of inflation is just what the policy doctor ordered – we just need to hope that the doctor is not out to lunch.